January 2024, Vol. 251, No. 1

Features

Global Pipeline Construction Outlook 2024: New LNG Terminals Sound Beckon Call for More Pipelines

By Michael Reed, Editor-in-Chief

(P&GJ) — It comes as little surprise to those in midstream that during the past year we have continued to see LNG initiatives garner more attention than pipeline projects. However, terminal construction drives new pipeline construction.

While this is increasingly true in Europe, where new pipelines are being developed to support new entry-points for gas, it’s also true in the United States, where new pipelines are needed to supply the liquefaction plants on the other side of the LNG supply chain. As LNG infrastructure continues to develop, pipeline construction will grow with it.

Similarly, thousands of miles of hydrogen pipelines are in development already, particularly in Europe, as the drive toward net-zero energy matures, and hydrogen finds a bigger role in the energy mix. This, too, will bring additional opportunities for pipeline construction and related work.

In fact, traditional pipeline construction remains strong, particularly in new gas markets. India in particular has remained strong among global pipeline construction as it expands gas access to hundreds of millions of people. Argentina is also transforming its relationship to energy as it develops its shale resources. There is still plenty of space to develop fossil fuel pipelines.

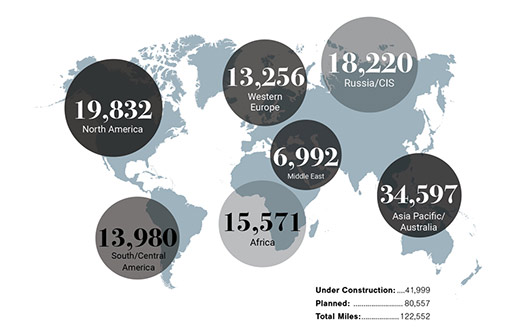

In our latest count, Pipeline & Gas Journal found a total of 41,999 miles of pipeline under construction as we enter 2024. Another 80,557 miles of pipeline are in the planning stages, reaching a combined total of 122,556 miles worldwide. Overall that figure represented a 9.3% increase worldwide over the previous year.

Globally, Indian and Chinese pipeline development continues to drive growth, with those countries containing around a quarter of planned and under-construction pipelines.

As in recent years, activity in global pipeline construction markets will continue to be bolstered by natural gas, with Europe still looking for additional sources to replace Russian supplies, and the Asia-Pacific region continuing to expand its import, transmission and distribution infrastructure, led by India and China.

NORTH AMERICA

Pipeline Miles Under Construction: 8,689

Pipeline Miles Planned: 11,143

Total: 19,832

North America is still developing as a major global supplier of LNG, through growing shipments from the Gulf Coast to Europe. Unfortunately, from the midstream perspective, pipeline construction to support future LNG expansions has been limited by a variety of factors.

Natural gas production growth in the Marcellus and Utica shale remains restricted due to pipeline bottlenecks from the region. And pipelines delivering Permian Basin and Haynesville gas to the Gulf Coast are catching up with near-term demand. Still, our forecasts for North America indicate a total figure of 19,832 miles of pipeline either planned or under construction in the region.

Of that total, almost 8,689 miles are currently under construction – which is more than was the case a year ago. Planned project mileage also rose to 11,043. Overall, that represents a 9.5% increase from last year.

In the United States, more than 8 Bcf/d of pipeline capacity is either planned or under construction from the Permian and Haynesville basins as pipeline operators jockey for position around LNG growth markets on the Texas and Louisiana Gulf coasts.

Complementing these efforts, an ongoing wave of acquisitions is making some of the biggest midstream players even bigger while embedding them more deeply in both production and demand markets.

Some of those acquisitions are expansions of gathering and processing footprints to support existing long-haul business. Others are aimed at positioning companies to capitalize on LNG demand growth, however, which requires that operators move ahead of the demand.

While much of the new capacity is a couple of years from becoming reality, the demand is there and will need to be supported by new natural gas pipeline projects. These projects range from new and expanded gathering systems, long-haul pipe construction, compression expansions and so-called “last mile” pipe connecting large transmission systems to specific areas and facilities.

And, while the timelines for LNG expansion can be fickle, with underutilization of new pipelines being common, the effect of those gaps will vary.

Energy Transfer, for example, has already finished construction of the 1.65 Bcf/d Gulf Run pipeline to move gas from north Louisiana to the coast. That project, gained through acquisition of Enable Midstream in December 2021, is backed by a 20-year agreement with the $10 billion Golden Pass LNG export plant now under construction in Texas by QatarEnergy (70%) and Exxon Mobil (30%).

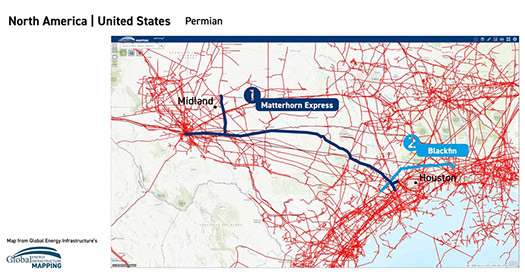

Permian

While most of the Permian Basin natural gas pipelines built-out in recent years has targeted LNG export markets to the south of the Houston area, two proposed intrastate projects have emerged within the couple of years that will deliver Permian Basin gas to the Texas-Louisiana border region.

The larger of the two, Targa’s 562-mile Apex pipeline, was approved by the Railroad Commission of Texas in late March. It would originate in Midland County in West Texas to Jefferson County, along the Louisiana border near Sabine Pass.

WhiteWater Midstream’s proposed 190-mile Blackfin Pipeline, which filed for state regulatory approval in February, takes a different approach. Although Blackfin would originate at the eastern edge of the Eagle Ford shale, it would primarily serve as an extension of the 580-mile Matterhorn Express Pipeline that was sanctioned in May 2022 by a joint venture of WhiteWater, EnLink Midstream, Devon Energy and MPLX.

Additionally, the Matterhorn Express itself is scheduled to be in service in the third quarter of 2024 and will provide 2-2.5 Bcf/d of Permian takeaway capacity to the Katy area west of Houston. Blackfin would link with Matterhorn to help debottleneck the Katy area and, like Apex, deliver volumes east to the Texas-Louisiana border area.

These Permian “connectivity” projects will be getting pipe closer to the LNG liquefaction projects than some past projects, such as Gulf Coast Express, Permian Highway and Whistler.

Haynesville

Several natural gas pipeline projects are in-development to connect Haynesville gas producers to Gulf Coast LNG exporters.

One major project is DT Midstream’s three stage Louisiana Energy Access Pipeline (LEAP) expansion. The existing LEAP Gathering Lateral Pipeline is a 155-mile, 1 Bcf/d line stretching from the Haynesville to the Gulf Coast region. DT midstream plans to increase LEAP capacity by 90% through compression and construction expansions to 1.9 Bcf/d.

The first stage of the expansion would add 300 MMcf/d of capacity, expected in-service by the end of this year. Stage two would add a 400 MMcf/d expansion due online in the first quarter of 2024 and the final stage would add 200 MMcf/d due in the third quarter of next year.

Momentum Midstream is currently developing the New Generation Gas Gathering project, dubbed NG3 from the Haynesville to coastal Louisiana LNG markets, with 275 miles of additional natural gas gathering pipelines with 2.2 Bcf/d of capacity. The system will be complemented with a Carbon Capture and Sequestration (CCS) solution to offer producers a net negative CO2 emission solution. NG3 is expected to be completed in 2024.

Additionally, Williams announced in May 2022 that it was committing about $1.5 billion to expand natural gas capacity and grow market access and followed up a month later by sanctioning its Louisiana Energy Gateway (LEG) project, which is designed to move 1.8 Bcf/d of Haynesville natural gas to several Gulf Coast markets. Tulsa-based Williams expects start-up of the LEG system by 2024.

Further to the south, Mexico is developing 31 mtpa of LNG export capacity on its west coast. Unusually for an LNG exporter, these projects are looking to import most of their feed gas.

That’s welcome news for U.S. natural gas producers, who stand to gain easier access to Asian markets, as well as pipeline operators who deliver their gas to the border and planned export terminals.

Most of the terminals will make use of spare capacity on existing pipelines including the Sonora pipeline, the Topolobampo pipeline and the Samalayuca – Sasabe pipeline, with gas originating at the Waha gas hub via either the El Paso Pipeline System or the Comanche Trail and Roadrunner Gas Transmission Pipelines.

The biggest potential new project is the Saguaro Connector Pipeline. The pipeline will deliver natural gas to the Mexico Pacific’s, in-development, 14.1 mtpa Saguaro LNG export facility on the Gulf of California coast. In December 2022, a division of Tulsa-based ONEOK filed an application with the U.S. Federal Energy Regulatory Commission (FERC) to construct the 155-mile pipeline which would run from the Permian Basin to Mexico.

The 48-inch, 2.8 Bcf/d pipeline would run to the border and interconnect with a planned Mexican pipeline which would carry on to Mexico Pacific’s LNG terminal, although no details of the Mexican route are available.

FID on the Connector Line had been expected by mid-2023 but has been pushed back to the end of 2023. The first 9.4 mtpa phase of Saguaro LNG is expected in 2025.

In Canada, one of the biggest positive developments for energy infrastructure developers in recent years has been that the nation’s First Nations are beginning to embrace the economic opportunities that pipeline and export projects can offer.

The growing technical and financial participation by First Nations represent a sea change in the relationship between Canada’s Indigenous leadership and midstream projects that has been years in the making.

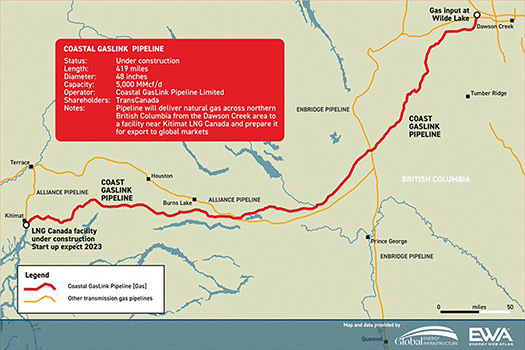

One of the clearest indications of that evolving perspective was the creation of the First Nations Major Projects Coalition (FNMPC) in 2016, a coalition of more than 130 of Canada’s First nation communities that have committed to work toward economic advancement through such projects as TC Energy’s Coastal GasLink pipeline.

In an early success, the coalition was instrumental in helping First Nations members reach an agreement to take a 10% ownership stake in its Coastal GasLink pipeline project, which TC Energy said completed construction on Oct. 30.

Coastal GasLink project involves the construction and operation of a 48-inch, 416-mile (670-km) pipeline from near the community of Groundbirch, in northeastern British Columbia, to the Shell-led LNG Canada Export Terminal, which also is scheduled for completion this year, near Kitimat, B.C. From there, the LNG will be exported to Asian markets, helping to reduce emissions by replacing high-carbon coal.

TC Energy is building the project in partnership with LNG Canada, Kogas, Mitsubishi, PetroChina and Petronas. The pipeline will be built to move 2.1 Bcf/d (59 MMcm/d) of natural gas with the potential for delivery of up to 5 Bcf/d (142 MMcm/d), dependent on the number of compressor and meter facilities constructed. The First Nations will assume its stake in the project upon completion.

Coastal GasLink will provide natural gas feedstock to the Shell-led LNG Canada liquefaction and export facilities currently under construction in Kitimat.

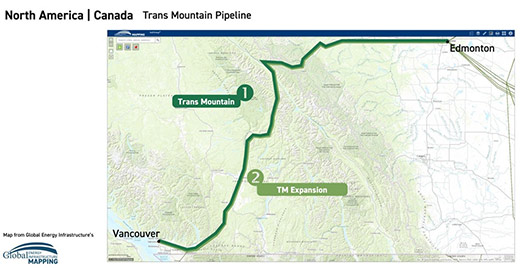

In another sign of growing First Nations involvement, Indigenous groups including Project Reconciliation, Nesika Services and Chinook Pathways are contenders for an ownership stake in Canada’s other major pipeline project slated for mechanical completion by the end of the year – the expansion Trans Mountain (TMX) pipeline and related export facilities.

Trans Mountain was acquired from Kinder Morgan Canada in 2018 by the Canadian government plans to sell Trans Mountain after completion. The project involves the twinning of an existing 715-mile (1,150-km) pipeline originating near Edmonton, Alberta, and extending to Burnaby, British Columbia.

The 590,000 bpd expansion will nearly triple the flow from Alberta’s oil sands to Canada’s Pacific coast, opening access to Asian markets. It includes more than 600 miles (980 km) of new 36-inch pipe and 120 miles (193 km) of reactivated pipeline, along with 12 new pump stations and 19 new storage tanks at existing terminals.

At this point, while the First Nations have continued to express interest in acquiring a stake in the project, potentially with Pembina, mounting costs for the project have raised concerns about a suitable return on the investment. Trans Mountain had been expected to start filling the pipeline, months ago, but has once again run into a construction-related hurdle that could delay its completion by 10 months.

Also in Canada, Keyera Corp. completed the Key Access Pipeline System (KAPS), a 357-mile (575-km) NGLs and condensate pipeline. It will transport 350,000 bpd of NGL and condensate from the Montney and Duvernay basins to Keyera’s processing hub in Alberta's Industrial Heartland, Fort Saskatchewan.

The pipeline will consist of a 16-inch pipeline for condensate and a 12-inch pipeline for NGL mix and handle 350,000 bpd.

SOUTH AND CENTRAL AMERICA/CARIBBEAN

Pipeline Miles Under Construction: 4,507

Pipeline Miles Planned: 9,473

Total: 13,980

South America is an active region for pipeline development with more than 13,980 miles of pipeline planned or under construction. The biggest milestone for South American pipelines this year was the completion of the first stage of the Nestor Kirchner Pipeline in Argentina.

The pipeline will bring to market Argentina’s Vaca Muerta shale gas. Located in the west of Argentina the Vaca Muerta reservoir is estimated to hold 300 Tcf of recoverable gas reserves. Argentina is currently a net importer of gas, but development of the reservoir promises to satisfy the country’s domestic demand and leave a large surplus available for export.

The Nestor Kirchner pipeline began development in 2018 and the first phase of the project, a 290-mile section of 36-inch pipe, was opened this summer. While the pipeline will eventually operate at a capacity 6.6 Bcf/d, until October of this year capacity will be limited to 3.5 Bcf/d.

This first section links Vaca Muerta production to Buenos Aires province where most of Argentina’s domestic gas demand is located. The second section of the project will carry gas further north to Santa Fe province where it can supply customers in northern Argentina.

As part of the project, Argentina is also reversing the flow of the Northern Pipeline, currently set up to receive gas from Bolivia. Bolivian gas production is falling, and Bolivia and Brazil are both potential markets for Argentina’s gas.

Combined with the flow reversal, a 93-mile interconnector between the Northern Pipeline and the Central East Pipeline will ensure additional Vaca Muerta gas has a route north to Argentina’s neighbors.

Construction on the second phase of the pipeline has yet to begin. State-owned Energia Argentina is expected to launch tenders for its construction this month, and it is hoped the second phase will be completed before the end of 2024.

EUROPE

Pipeline Miles Under Construction: 4,398

Pipeline Miles Planned: 8,858

Total: 13,256

Pipelines have not been the main midstream story in Europe this year. Instead, the continent is continuing its massive LNG build-out as it looks to replace Russian pipeline gas.

Over the period from the start of 2022 to the start of 2023, Europe added about 77 mtpa of new LNG regasification capacity, representing a 44% increase over 2021. Nearly 37 mtpa of this capacity has started or will begin operations between now and the end of the year.

Additionally, Europe is expanding its gas pipeline networks to support gas flows from these new LNG terminals. Germany, for instance, is planning to add 355 miles of pipeline over the next few years to accommodate new LNG imports, almost all of which will be high-capacity pipe with a diameter of 39-inch or greater.

Hydrogen Pipelines

The other big pipeline story in Europe centers on the ongoing development of the European Hydrogen Backbone, which could see many existing natural gas pipelines across Europe converted to carry hydrogen as well as some new pipeline construction.

The majority of Phase 1 of the Hydrogen Backbone, with significant portions located in France, Germany, Belgium and Austria, is expected to begin operations between 2026 and 2030, with future expansions planned. Many hydrogen pipelines are also being built as part of hydrogen clusters across the continent.

AFRICA

Pipeline Miles Under Construction: 2,829

Pipeline Miles Planned: 12,742

Total: 15,571

Both Africa and the Middle East have been quiet regions for pipelines this year. In Africa, major projects continue to languish in the early stages of planning with relatively few projects entering the construction stage and no major projects having begun operations this year. Planned pipelines in Africa total 15,571 miles of pipeline are planned in Africa, but only 2,829 miles of pipeline are under construction.

In Uganda Tilenga and Kingfisher petroleum projects, as well as a pipeline to carry oil to Tanzania for export, are on track for first production by 2025, Uganda National Oil Co.’s chief executive is on record as saying.

The 898-mile (1,445-km) East African Crude Oil Pipeline (EACOP) that will transport crude from Tilenga and Kingfisher is scheduled to come online in 2025.

EACOP is co-owned by the government of Uganda, France’s TotalEnergies, China’s CNOOC and Tanzania’s Tanzania Petroleum Development Corp (TPDC).

Uganda is in advanced talks with Chinese export credit agency SINOSURE to provide credit for the project, which will cost $5 billion, including the cost of credit, and 40% of the money will be raised through debt while the rest will come from equity, a top Ugandan official said.

MIDDLE EAST

Pipeline Miles Under Construction: 1,164

Pipeline Miles Planned: 5,828

Total: 6,992

In the Middle East, there are 6,992 miles of pipeline planned or under construction. Most new pipelines are shorter and will connect new fields across the region to existing pipeline networks with little in the way of major transmission pipelines in-development for either oil, refined products or gas.

QatarEnergy signed a deal with Exxon Mobil for the Gulf state’s North Field East expansion, the world’s largest LNG project, following agreements with TotalEnergies, Eni and ConocoPhillips. Qatar is partnering with international companies in the first and largest phase of the nearly $30 billion expansion.

The companies will form a joint venture, with Exxon holding a 25% stake in that, according to QatarEnergy CEO Saad alKaabi. Oil majors have been bidding for four trains that comprise the North Field East project. In all, the North Field Expansion plan includes six LNG trains that will ramp up Qatar’s liquefaction capacity from 77 mtpa to 126 mtpa by 2027.

In 2022, the Iraqi cabinet approved the framework agreement for the long-studied Basra-Aqaba Oil Pipeline, roughly three months after talks between Iraq and Jordan were reported by Iraq’s oil ministry to have reached an “advanced stage.”

The latest step pushed forward a project that the two countries agreed to way back in 2012. Last year, the ministry noted that the cost should be brought under $9 billion for the project to go ahead. However, there have been reports since last April that the project is taking longer than expected and has stalled as Iran tries to block its construction on the pretext that it aims to supply oil to Israel and other nations.

The pipeline would carry crude oil to the Jordan Petroleum Refinery Company’s plant in Zarqa to meet Jordan’s needs and to the Aqaba Port for export purposes. The first phase of the project would be constructed in Iraq, across a 435-mile (700-km) stretch between Rumaila and Haditha.

ASIA PACIFIC/AUSTRALIA

Pipeline Miles Under Construction: 13,331

Pipeline Miles Planned: 21,266

Total: 34,597

Asia Pacific remains the region with most new pipeline activity. This is in large part due to the fast-growing infrastructure of the world’s two largest countries, China, and India.

In particular, India is seeing an enormous pipeline infrastructure build-out as economic growth takes off. GDP growth for the country is forecast to be between 6 and 7% over the next 12 months, and the nation is hopeful that gas will have a 15% share in the total energy mix by 2030, up from about 6% in 2022.

13,331 miles of pipelines are currently planned or under construction. Major gasification efforts are taking place in the country’s northeast and northwest. Pipelines are also increasingly reaching out from the coasts to central India.

However, some projects continue to be plagued by delays. GAIL’s Mumbai- Nagpur-Jharsuguda Pipeline is a case in point. The pipeline planners had hoped to avoid delays by choosing a route adjacent to a government highway, removing the need to obtain permission to build from private landowners. Despite that commissioning has been pushed back from May of 2023 to October 2024.

In February, GAIL claimed the 451-mile Mumbai-to-Nagpur section was about 80% complete with GAIL citing technical issues for the delay. The 874-mile, 32-inch pipeline would run from Mumbai to Jharsuguda, delivering 580 MMcf/d of gas to new markets in central India.

Other delayed projects include the final phase of GSPL’s Mehsana-Bhatinda pipeline in the northwest, delayed due to difficulties obtaining building permission from local farmers, and IMC’s Kakinada-Vijayawada-Nellore pipeline. Originally expected in 2021, that pipeline’s start-up has been pushed to 2024.

Nevertheless, India’s pipeline expansion remains exceptional. Construction on IGGL’s North East Gas Grid continues and the pipeline system is expected to be fully commissioned in March 2024.

Hundreds of millions of people stand to benefit from access to new energy sources. India has about 10% of global under construction pipeline mileage and that number is likely to grow as time goes one.

RUSSIA/CIS

Pipeline Miles Under Construction: 6,981

Pipeline Miles Planned: 11,239

Total: 18,220

Mega-projects make up most of new pipeline activity in Russia, much of that in the planning stages. Of the 18,220 miles of pipeline planned and under construction in Russia, nearly 25% are associated with a few mega-projects.

The most watched pipeline projects in the region are the three Power of Siberia projects, which aim to increase Russia’s gas exports to China. Power of Siberia 1, which opened in 2019, continues to ramp up this year.

Flows through the pipeline rose 47% year-over-year and are expected to reach 776 Bcf (22 Bcm) by the end of 2023, according to Global Energy Information, closing in on the pipeline’s maximum capacity of 3.8 Bcf/d. The Power of Siberia 3 project has also progressed this year. The pipeline would connect Dalnerchensk in the Russian far east to the Chinese city of Harbin, allowing gas from fields on and around the island of Sakhalin to reach China.

In January 2023, a key agreement allowing construction on the cross-border section of the pipeline was signed, although the deal has not been ratified yet. December 2022 also saw the completion of an expansion project for the Vladivostok Gas Transmission System, which would supply Power of Siberia 3.

Though the expansion provided no immediate increase in capacity, it has prepared the pipeline to supply up to 3 Bcf/d of gas, up from about 2.4 Bcf/d once additional compressor stations are added.

The most important Russian project remains Power of Siberia 2. Unlike the other Power of Siberia projects, which link to recently developed gas fields in Russia’s far east, Power of Siberia 2 would draw from Russia’s gas fields in West Siberia, the heart of Russian gas production, where most Russian upstream gas infrastructure is located.

Without European markets, this gas is stranded now. Power of Siberia 2 would provide an alternative export route, connecting the West Siberian Basin to China with a 55-inch, 5 Bcf/d pipeline. The pipeline would cost tens of billions of US dollars and would likely take at least a decade to build.

High-level talks were held in Moscow in the spring of 2023 which were expected to result in a gas deal regarding the pipeline. But no formal deal materialized. For now, the project remains in limbo.

Additionally, Novatek, the Russian energy giant, has officially announced its project to construct an extensive 808-mile (1,300-km) gas pipeline reaching Murmansk, Russia, according to The Barents Observer.

This project, approved by the Kremlin, is set to provide a vital source of natural gas to the households in Murmansk and Karelia while also catering to the requirements of a new LNG facility in the Kola Bay.

CEO Leonid Mikhelson unveiled this milestone during Russian Energy Week, emphasizing that Novatek will take the reins in building this pipeline project capable of transporting 1.4 Tcf (40 Bcf) of gas annually.

The decision to embark on this infrastructure project was made at the highest echelons of government after extensive deliberations.

Approximately 75% of the pipeline’s gas capacity will be allocated to the forthcoming Murmansk LNG plant, with the remaining 25% earmarked for the gasification of towns and communities in the Karelia and Murmansk regions.

Editor’s note: This report has been compiled by the Pipeline and Gas Journal editorial team and by researchers at Global Energy Infrastructure (GEI). GEI is a real-time database that provides data on over 7,000 global oil and gas pipeline projects, as well as on other energy infrastructure, including Hydrogen production facilities, carbon capture storage sites and LNG terminals.

In addition, resources for this report include owner/operator editorial contacts, FERC filings, the National Energy Board in Canada and other government energy regulators arounds the world. Researchers also make extensive use of company websites, annual reports, press releases and official social media.

Comments