March 2016, Vol. 243, No. 3

Web Exclusive

Ethane Production Expected to Increase as Petrochemical Consumption and Exports Expand

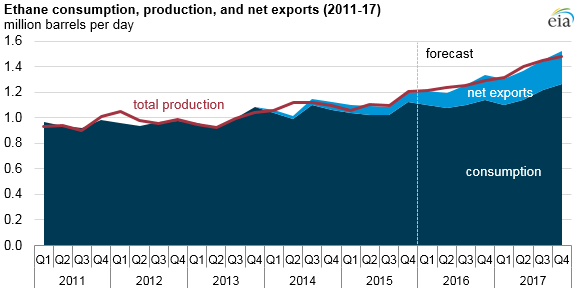

Ethane production is expected to increase from 1.1 million barrels per day (b/d) in 2015 to 1.4 million b/d in 2017, accounting for two-thirds of total U.S. hydrocarbon gas liquid (HGL) production growth. Ethane, a key feedstock for petrochemical manufacturing, is recovered from raw natural gas at natural gas processing plants.

Over the past five or six years, the amount of ethane contained in domestically produced raw natural gas has exceeded the capacity to consume and export it. This oversupply kept ethane prices relatively low, hovering at or below the price of natural gas, leading producers to reject the ethane stream by leaving it mixed with the stream that is marketed as pipeline natural gas, which is mostly methane.

Beginning in 2012, the availability of relatively inexpensive ethane encouraged a wave of investments in ethane-consuming petrochemical plants and export facilities. The recognition that these investments would provide an outlet for U.S. ethane also encouraged investment in facilities to recover ethane from raw natural gas and to transport it to market. Many of these projects, including de-ethanization facilities, ethane pipelines, petrochemical plants, and ethane export facilities, have either recently been completed or are currently under construction and will come online in the next few years. These projects increase take-away capacity for ethane, especially in the Marcellus and Utica shale regions, mainly in Pennsylvania, Ohio, and West Virginia, where market outlets for rapidly growing natural gas supply were previously limited to pipeline natural gas.

As new ethane-consuming petrochemical and export capacity reduces the ethane oversupply in 2016 and 2017, ethane prices are expected to generally remain above natural gas prices, leading to a rise in ethane recovery to meet demand and export growth. EIA’s recent report on the Short-Term Outlook for Hydrocarbon Gas Liquids examines ethane production, consumption, exports, and infrastructure projects.

U.S. ethane consumption, which was 1.05 million b/d in 2015, is forecast to increase 50,000 b/d in 2016 as expansion projects at ethylene-producing petrochemical plants increase feedstock demand for ethane. In 2017, ethane consumption is projected to increase another 80,000 b/d as capacity begins to ramp up at five new petrochemical plants and at a previously deactivated plant.

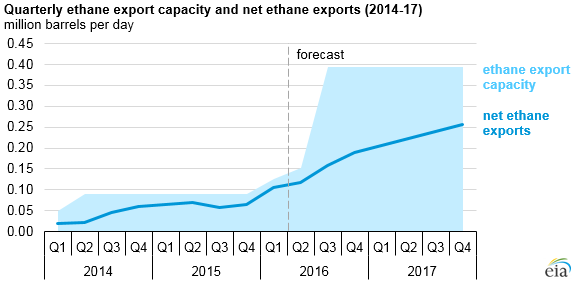

In 2014, the United States switched from being a net importer of ethane to a net exporter after the opening of two new ethane pipelines that began transporting ethane from North Dakota and southwestern Pennsylvania to Canada. EIA’s Short-Term Energy Outlook (STEO) expects annual average ethane net exports to increase from 60,000 b/d in 2015 to 230,000 b/d in 2017, as new export facilities and ethane-carrying ships enable ethane to reach overseas markets. On March 9, the United States shipped the first waterborne exports of ethane from the Marcus Hook, Pennsylvania terminal to Europe. A second ethane terminal is expected to open at Morgan’s Point, Texas in the third quarter of 2016. The two terminals are expected to export ethane mainly to European and Asian countries.

Comments