May 2015, Vol 242, No. 5

Features

The Shale Gas Revolution and Effects on the Northeast Gas Market

Without a doubt, the biggest factor impacting the U.S. gas market is the development of shale gas in the Marcellus Shale play, located in northern Appalachia and the Alleghenies. The shale gas revolution in the U.S. – specifically in Pennsylvania and West Virginia – is nothing short of a revolution for the entire country.

To illustrate the scale of this change, let me take you back to the 2008-09 period. At that time, production in Appalachia was about 2 Bcf/d out of about 50 Bcf/d nationally. At about 4% of U.S. production, the Marcellus Shale production came from a bunch of small producers, and it was a total sideshow: It didn’t matter for U.S. production or energy security.

What mattered was production in the Gulf Coast region, where production offshore and onshore accounted for about half of U.S. production. Another 10 Bcf/d came from the Rockies, and about 5 Bcf/d from Canada. In the Northeast, gas companies focused on sourcing gas from the Gulf Coast and Canada. We didn’t have our own production.

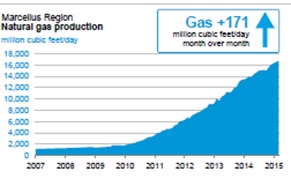

Now things are completely different. We found so much gas in Pennsylvania and West Virginia that we are producing 15-18 Bcf/d in the East (Graph 1). This is nothing short of amazing. Now, thanks to Marcellus and other shale and tight gas production (see graph #2), U.S. production is up 30 Bcf/d to roughly 80 Bcf/d and almost a third is from the East. Production is so extensive that we’re now exporting out of the region.

Shale gas production – particularly in the Marcellus Shale play in Pennsylvania and West Virginia – has skyrocketed in the last five years (Graph 3). What this means for the gas business is that we have to rework the pipeline network to get this new gas moved out to demand centers in the region as well as into the Midwest and Southeast.

The flow of every major pipeline in the Northeast has changed because of this production. Now gas is flowing from the Marcellus Shale to the Tri-State Area and New England, and also from the Marcellus region to other parts of the country that used to ship to us. Also, the gas from the Gulf Coast that used to be shipped north is staying there.

A company not understanding the network wouldn’t find supply in the cheapest area. If you based your decisions on status quo five years ago, you’d be making a mistake.

If you buy gas in Louisiana or Texas and ship it to New York, you’d be marking to the Henry Hub price – the market price on the Gulf Coast. Historically, most gas at the national level was priced close to the Henry Hub contract, or with a small differential.

But the market has changed. Because there is so much gas being produced in the Marcellus, regional hubs in Pennsylvania now can have dramatically different prices from Henry Hub – up to 50% less (Chart 1). In October, prices in Pennsylvania fell below $2 per million Btu, less than half the Henry Hub price.

When demand in the Northeast is low, there is a backlog of gas in the region. In summer, when natural gas isn’t needed for heat, the New York delivery price is 50-70 cents below Gulf Coast price. Under these market conditions, you shouldn’t use any long-haul transport. You should just be using delivered gas. This means you are buying cheaper gas locally, at the “city gate,” and also saving by not paying unnecessary long-distance transport fees.

So how does this affect you if you’re a small commercial customer on Long Island (or elsewhere in the Tri-State area), such as a bakery or apartment building owner?

The answer is, you need a gas company that understands how the market works and can minimize transport and purchase costs. A smart company that understands the market can optimize storage and delivery contracts to keep the price of gas as low as possible for the consumer. That way, when prices go down in the region during periods of low consumption, they can take advantage and pass these savings on to the customer.

Author: Scott LaShelle graduated in 1985 from Georgetown University with a bachelor’s degree in foreign service. He was recruited by JP Morgan into its training program and worked for six years in various capital markets positions until moving to JP Morgan’s energy derivatives desk in 1992. He was responsible for origination of oil and gas deals. In 1998, LaShelle joined Sempra Energy Trading’s derivatives desk, eventually moving to Sempra’s East Gas desk in 2000, where he managed the desk from 2005-08. manage East Gas business. The newest member of Great Eastern Energy’s executive board, Scott joined the company in 2013.

[inline:SHALE2.jpg]

Graph 2 – Source: Geology.com

[inline:SHALE3.jpg]

Graph 3 – Source: National & Regional Production of Natural Gas, 2008-2013.

Based on data from U.S. EIA, Natural Gas Gross Withdrawals & Production.

[inline:scott_lashelle-264×264.jpg]

LaShelle

Comments