April 2015, Vol. 242, No. 4

Features

Nimble by Nature: Pipeline Market in Transition

In an environment that is exhibiting disruption and change, being nimble is a necessity. The concept of being flexible rather than rigid in the face of change is one that for many industry participants is counterintuitive.

Bruce Lee might have said it best when he suggested, “Empty your mind, be formless. Shapeless, like water. If you put water into a cup, it becomes the cup. You put water into a bottle and it becomes the bottle. You put it in a teapot, it becomes the teapot. Now, water can flow or it can crash. Be water, my friend.”

Those leaders who adapt to change and are nimble in the coming decade will thrive while those that remain rigid will be ground down the way water cuts a canyon.

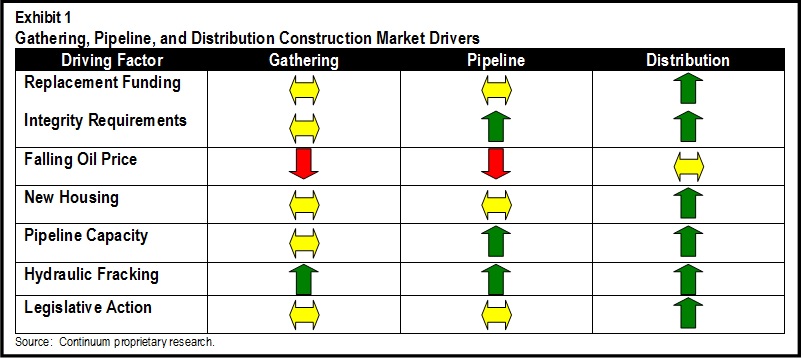

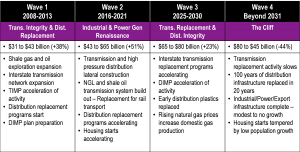

To thrive, leaders must understand the drivers of the gathering, pipeline and distribution market, including the seven factors described in Exhibit 1. The majority of these are increasing both the actual and potential spending for pipeline infrastructure, and they each affect the construction put in place (Exhibit 2). While spending ebbs and flows, the overall trajectory of this market space has resulted in spending rising from $6.9 billion in 2003 to $43.8 billion in 2014 with a forecast of $65.5 billion in 2020.

Over this timeline, this segment is the best performing from the power market, which includes power generation, electric transmission and distribution (T&D), and gas/liquid T&D. While our forecast anticipates a short and shallow slowdown in spending in early 2017, we see a continued upward trajectory over the long term for this market through 2030, after which spending will decelerate and then fall.

Spending Drivers

Traditionally, construction markets produce five- to seven-year cycles that coincide with the economy. The pipeline market has resisted these cycles because growth is not solely derived from economic factors, but from a combination of economic and “derived demand” incentive. Note the brief slowdown in spending in 2010 and 2011. While other types of construction were continuing to suffer, the pipeline market lost little activity. Derived demand restricted the fall in spending in this market due to government regulation, safety and environmental or other actions that resulted in capital construction and maintenance activity.

Replacement Funding: Asset replacement is most strongly affecting the distribution market. More than 38 states have some type of accelerated cost recovery that goes beyond the traditional rate case mechanism. Many of these states are using cost-tracking techniques that allow for the recovery of spending starting as short as three to six months after the initial expenditures.

This dramatic change in approach to address the safety and performance of distribution infrastructure began in earnest in 2009 and is the largest single contributor to the increase in spending. The vast majority of local distribution companies are just now addressing the faster replacement of existing infrastructure. One example can be found in Pennsylvania. Columbia Gas of Pennsylvania (CPA) has a mature main and service replacement program in existence that will likely continue for another five to ten years.

Columbia is one of six large utilities that have roughly the same size system; the other five are only beginning replacement programs. Using CPA as a guide, it is possible that in three to five years, Pennsylvania will exhibit five to ten times the current amount of distribution pipeline-related capital construction and maintenance activity (Exhibit 3).

Who will perform this work and at what cost is unclear. (Research Opportunity: Continuum is researching the answer to this question and will present results at the AGA/DCA Contractor Management Conference on April 28-29 and AGA Operations Conference on May 22. If you would like to participate in this research as a pipeline company, utility or contractor, contact Mark Bridgers at MBridgers@ContinuumAG.com or (919) 345-0403).

Integrity Requirements: Transmission integrity management plans (TIMP) and distribution integrity management plans (DIMP) are making a significant impact on both construction and maintenance activity. High-profile leaks, spills and explosions that are direct threats to public health and safety only push this market toward higher spending. Gathering lines, while similar to either transmission or distribution lines, receive less scrutiny from an integrity and regulation standpoint.

Transmission integrity programs are well established and, given the federally required assessment cycle, every mile of the about 475,000 gas or liquid lines have been inspected at least once using inline inspection (ILI) tools or external corrosion direct assessment (ECDA) techniques. Distribution integrity programs are just beginning but much of this asset base is not piggable with ILI tools.

Given the age, performance, regulatory perception and public perception, the only possible course going forward is a more consistently applied standard to gathering, transmission and distribution lines that will result in more inline inspections and integrity assessments. All of these actions will result in additional construction and maintenance expenditures.

Falling Oil Price: Oil has dropped from $100/b to $50/b since late 2014 (Exhibit 4). This relatively rapid reduction in price is not well explained and is hurting the U.S. gathering and transmission pipeline market. We see five drivers of the change in oil price:

- Low global demand: The economic slowdown in Asia and Europe has reduced demand.

- High supply: Five years of $90-plus oil led to massive investment in exploration and production.

- OPEC weakness: OPEC’s share of world supply is declining; members have grown fat domestic budgets fueled by high-priced oil, and these countries want to protect their market share.

- Geopolitical action: Saudi Arabian opportunity to economically punish Russia, Iran and Syria without directly harming the United States and inflicting moderate and manageable damage to their domestic budget.

- Speculation: It is not clear what role speculators play in the current crude oil price swing, yet there is general agreement that speculative activity continues and is moving prices.

The impact on the distribution market is muted and unless prices fall farther, we anticipate no significant changes in spending patterns for distribution pipeline construction.

New Housing: Since the collapse of the housing market in 2007, home construction has performed poorly. In 2014, the market finally reached 1 million starts and is finally on the path to a more real, robust recovery. The housing sector is a driver for nearly every other type of construction but it has been absent. As housing starts accelerate there will be greater demand for transmission infrastructure to strengthen and reinforce system performance, yet we anticipate seeing this impact in five to seven years.

Distribution activity impact is almost immediate. In Exhibit 5, we note that homebuilders have been slow to rebuild their construction workforce. In the trades of framing, drywall and masonry, there is a severe shortage that is creating longer build cycles, poor quality and fewer closings. On the flip side, customer fear of rising interest rates and home prices is driving activity. The net effect is continued accelerating progress and a faster housing recovery.

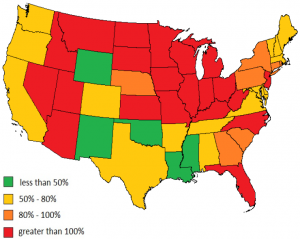

Pipeline Capacity: Pipeline capacity and availability at the gathering, transmission and distribution level is affecting decision-making and the development of the pipeline market. As an example, the lack of adequate gathering systems in North Dakota are resulting in the flaring of natural gas associated with shale oil drilling. The lack of adequate transmission and distribution capacity prevents greater use of natural gas in the Northeast.

Although dated, the chart (Exhibit 6) from 2010 offers insight into the states and regions where capacity is most constrained. A related opportunity has to do with the use of rail to move oil from western Canada, western United States and to a lesser extent from the Ohio and Pennsylvania shale basins. Rail transportation has risen dramatically since 2010, which in our view, is due to a combination of capacity issues and a desire for flexibility that rail offers producers.

Now that the price of oil has fallen, producers will search for a low-cost, longer-term, and safer solution that will result in additional transmission pipeline construction. As these critical capacity issues are addressed, we anticipate faster spending on pipeline and distribution infrastructure throughout the United States, in particular targeting the Northeast, Midwest and Southeast.

Hydraulic Fracking: This is the initiating source for much activity in the gathering, pipeline and distribution markets. The connection to gathering and pipeline is perhaps obvious in that once exploration is complete and production begins, gas or oil must be moved from the rig to either a processing point or the transmission system.

As U.S. production of natural gas and oil has increased, the building of these assets is a requirement. On the distribution front, the increases in supply have driven the price of natural gas to about $3 from as high as $10 (Exhibit 4). This 70% reduction in cost has allowed distribution utilities to expand their capital programs and receive rapid recovery of the expenditures within the rate base while customers most likely saw their combined asset and commodity bills remain the same or fall. The next effect is a largely pain-free improvement in the distribution system since 2008 in the eyes of the ratepayer.

?

Legislative Action: The use of legislative action to accelerate pipeline construction activity is becoming an increasingly important driver of natural gas infrastructure spending. Legislation in the Northeast, Midwest, Mid-Atlantic and California has created specific requirements and funding mechanisms that are driving increased spending on infrastructure.

Illinois, Indiana, and Massachusetts each have similar legislation with Massachusetts house bill H4164 providing a good example. The bill establishes a mechanism for recovery of infrastructure replacement cost in return for utilities establishing programs that will replace all leak-prone infrastructure within 20 years.

Most of the legislation targeting infrastructure replacement is driven by safety and environmental concerns, allowing it to gain bipartisan support. In addition to legislation targeting leak reduction, bills in many states have been passed that support the growth of infrastructure to support natural gas vehicles, expansion of gas service into rural areas, investment in upstream reserves and streamlining of rate-case processes. The trend of legislative action to promote spending on natural gas infrastructure will continue.

Conclusions

The long-term prospects for gathering, pipeline and distribution markets are extremely good. They are, however, unbalanced in sector, geography and timing. Energy firms, pipeline operators, utilities and contractors that are rigid, short-sighted, backward-looking and traditional will be cut the way rock is cut by running water.

Success in these markets requires that energy firms, pipeline operators and utilities recognize the changing market dynamics and position their firms with the highest quality and safest contractors available to them. For contracting organizations, they must learn how to adapt, understand the drivers of activity in these markets and position their firms and capabilities appropriately.

Both owners and service providers face variability, change, challenge and opportunity and as water flowing over, under, around or even through an obstacle. Firms that thrive in these markets must be nimble by nature.

Authors: Mark Bridgers, Nate Scott and David Shipley are consultants with Continuum Advisory Group, which provides management consulting, training and investment banking services to the worldwide utility and infrastructure construction industry. They can be reached at (919) 345-0403 or MBridgers@ContinuumAG.com, who can be followed on twitter at @MarkBridgers.

Exhibit 2a

Exhibit 2b

Exhibit 3

Exhibit 4

Exhibit 5

Exhibit 6

Comments