May 2014, Vol. 241, No. 5

Features

Challenges Of Converging U.S. Gas, Power Markets

Many utilities are expanding portfolios of power generation assets, and as older coal-fired plants retire, utilities are deciding what must replace them. While some older plants are candidates for retrofitting to natural gas, others will be forced to shut down.

The Energy Information Administration (EIA) reports that the federal government’s most recent forecasts project about 49 gigawatts of coal-fired generation capacity could be retired within the next eight years – facilities driven from the market by a combination of increased Environmental Protection Agency (EPA) rulemaking and cheaper natural gas.

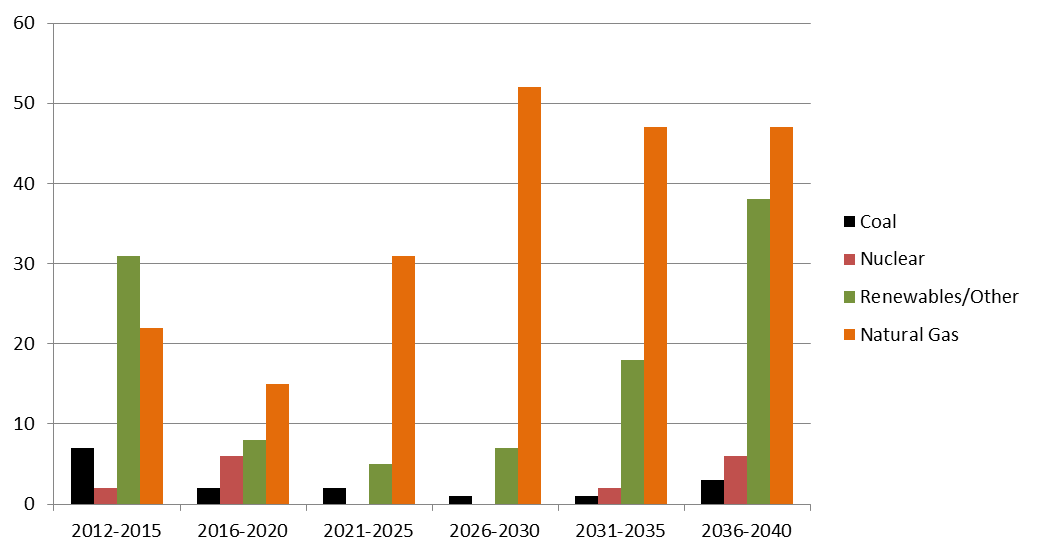

Since 2010, and with the recent dramatic drop in natural gas prices in North America, natural gas displacement of coal as a primary fuel for power generation has been accelerating. Last spring, the EIA reported for the first time, natural gas and coal provided an equivalent share of the power produced in the United States, each providing about 96 million megawatt hours in that month. In fact, the EIA also projects that natural gas-fired plants will account for 63% of capacity additions from 2012-2040, compared with 31% for renewables, 3% for coal and 3% for nuclear.

With utilities retiring large as well as centrally located coal facilities while transitioning to smaller, more numerous and geographically dispersed gas-fired plants, power generation companies are increasingly exposed to new, potentially more complex, markets in which to purchase, manage and deliver their fuels.

Whereas coal is generally purchased under long-term agreement and can be stockpiled onsite, natural gas is an on-demand delivered fuel, meaning in order to ensure adequate supplies to meet obligations, utilities must invest in additional assets (including firm pipeline capacity and gas storage) and enter into a portfolio of supply agreements that balance operational and delivery risks against price exposures.

Integrating these new operations and new markets can be challenging, as fuels management systems that were adequate for coal plants operating as base-load facilities will not meet the needs of a utility operating a fleet of gas-fired generators.

With the incorporation of new gas-fired assets, new energy trading and risk management solutions are required to address the complexities of the natural gas markets and infrastructure, including the ability to capture and manage complex natural gas purchase and sales agreements, create and manage nominations across multiple pipelines, manage natural gas storage agreements and perform risk management.

Even for companies that had previously operated a handful of gas generators, the increased adoption across a wider geographical area will increase operational complexities, taxing current systems and increasing both operational and financial risks.

One area of particular operational concern is the forecasting and nominating of fuel supplies well in advance of power delivery. This includes managing optionality in fuel supply agreements that provide surety of delivery to meet reliability requirements, yet also allow for alternate delivery, turn back or resale should the fuel not be required for power generation.

As new gas-fired assets are brought onboard, the importance of capturing and maintaining a complete portfolio view increases in importance, as natural gas systems for fuels management cannot live in isolation. These systems must be closely incorporated into the larger utility IT infrastructure, one that will include systems for managing power sales and purchases, plant operating systems, production cost models, and regional transmission organization (RTO) or independent system operator (ISO) bidding, settlement and market communications systems.

Beyond the operational concerns, this integration is also important to ensure adequate risk management visibility, capturing the complete value and exposures associated with the generation portfolio. Given the dynamic nature of the natural gas and power markets, with each evolving toward convergence with the other, price correlations are in flux, and market events, such as power peak days or natural gas pipeline upsets, can inflict rapid and potentially extreme damage to near-term portfolio values.

The Federal Energy Regulatory Commission (FERC) has also highlighted the need to ensure adequate pipeline capacity to support the increased use of natural gas to generate electricity.

Specifically, FERC noted that, “Because natural gas is generally delivered on a pipeline network rather than stored onsite, it is important that we have an adequate pipeline network and operating practices that support the reliability of both electric and gas networks. In certain regions, there may be inadequate local pipeline capacity to support generation during the winter heating season due to geography, fuel mix and market structure. This is already an issue in New England and may be an emerging issue in other regions as more gas is utilized for generation.”

The development and operation of infrastructure has been one of the more challenging aspects of operators in the natural gas markets in terms of coordination with power generators. The increased use of natural gas to generate electricity poses certain integration, coordination, and reliability issues.

Recently, the Subcommittee on Energy and Power continued its American Energy Security and Innovation hearing series with a focus on natural gas and electric coordination challenges. The series builds on the subcommittee’s recent hearing on the importance of fuel diversity and examined the challenges facing electricity markets as a result of the growing share of natural gas in the nation’s electric generation portfolio.

The committee emphasized that generating power from natural gas has many benefits, especially given that domestic supplies are increasing and prices are relatively low. But it also cautioned there are some very real challenges in integrating more natural gas into the power sector.

FERC expressed the urgent need for regulators and industry stakeholders to work together to address these challenges, stating, “Ultimately, the challenges we face with gas and electric coordination is a good problem to deal with as it’s partially the result of abundant domestic gas resources. But the challenges are serious, very real, and somewhat urgent, especially in New England and the Midwest.”

FERC also warned of concerns that some in the industry believe nothing short of a major blackout will provide sufficient motivation to the various stakeholders to solve the problems facing the industry, and that there is a critical need for the energy industry, regulators, and legislators to be focused on the range of solutions necessary.

Editor’s Note: On April 8 the EIA reported that natural gas-fired power plants accounted for just over 50% of new utility-scale generating capacity added in the United States in 2013. Solar provided nearly 22% of new generating capacity; coal at 11% and wind nearly 8%, according to the EIA. Almost half of all generating capacity added in 2013 was located in California. In total, a little over 13,500 megawatts of new capacity was added nationwide in 2013, less than half the capacity added in 2012, the EIA reported. Nearly 60% of the natural gas capacity added in 2013 was located in California. Just two coal plants, both delayed projects that were originally scheduled to be completed in 2011-2012, accounted for all of the coal capacity added in 2013. One was in Texas, the other in Indiana.

Comments