May 2013, Vol. 240, No. 5

Features

North America: An Energy Rocket Ship If Mexico Gets Aboard

A panel discussion was recently waged by a Canadian, an American and a Mexican talking about North America’s energy future as the new Middle East for the rest of the world. Hyperbole was cheap, but chances of the provocative scenario becoming a reality ride squarely on the shoulders of Mexico. And everyone was OK with this.

The amount and timing of a whole host of infrastructure investments south of the U.S. border – the continent that is suddenly awash in oil and gas – provided a backdrop for a host of energy perspectives of the panelists.

A former private equity investment sector executive and now senior fellow at the Manhattan Institute for Policy Research, Mark Mills, in mid-2012 released a white paper that his colleagues tout as a treatise for a North American “colossus,” touting macro-economic numbers in the hundreds of billions to the trillions of dollars.

“The total North American hydrocarbon resource base is more than four times greater than all the resources extant in the Middle East, and the United States alone is now the fastest-growing producer of oil and natural gas in the world,” wrote Mills in his “Unleashing the North American Energy Colossus: Hydrocarbons Can Fuel Growth and Prosperity.”

Out of the think tanks and on the ground, this bullish prognostication is still being sorted out, but the depth and breadth of the discussion on one dreary Monday in New York City was on right target concerning what many in the energy industry are grappling with: How does the American energy sector leverage this energy bonanza in North America more effectively on a global basis?

It will start with the newly installed Mexican government freeing up oil and gas development and production to the private sector and beginning to create some semblance of a free market for energy, according to Luis De la Calle, a Mexico City-based international economic consultant and a former official in Mexico’s Ministry of Economics.

“We have to ask ourselves: are we willing to have a common North American market for energy goods?” De la Calle told the Manhattan Institute audience in December. “I think now is the right time to ask whether we want to have energy be the sparkplug for true development in Mexico.”

At that conference and elsewhere in the oil/gas patch in the United States and Canada, the answer appears to be in the affirmative, and markets north of the Mexican border are all trending southward toward the Gulf of Mexico and farther to the Southwest. The goal is the re-industrialization of the United States and the emergence of a fully developed economy in Mexico.

“It is very likely we will continue to see more investment to bring in more U.S. gas to Mexico,” said Jose Coballasi, director of the Mexico City office of Standard & Poor’s Ratings Services.

One of his analysts, Fabiola Ortiz, added this will bring with it larger investments in exploration and production of gas.

“Mexico will continue to invest in natural gas [in Mexico], but, I think, they still clearly need to bring in more gas from the United States,” said Coballasi, who several times repeated the fact that the cheap U.S. supplies, with their closeness to Mexico, are enticing to officials in Mexico City.

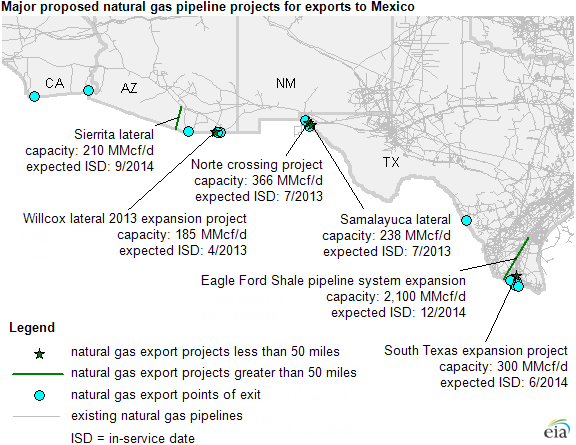

The building boom for gas infrastructure is already under way with both TransCanada and Sempra Energy subsidiaries selected to build several billion dollars’ worth of new transmission pipelines, and El Paso Natural Gas Co. providing an added link that will connect its Southern System, running through Arizona, with part of the Sempra work.

In the last quarter of 2012, TransCanada won the bidding to build a $1 billion, 329-mile, 30-inch transmission pipeline and a $400 million, 257-mile, 24-inch pipeline. At the same time, San Diego-based Sempra Energy was awarded the contract on a 500-mile, two-phase pipeline project in northwest Mexico that will be linked to Kinder Morgan’s El Paso Southwest interstate system. Sempra affiliates already have several gas infrastructure projects valued at more than $2.4 billion operating in Mexico.

Sempra and TransCanada have come away with 25-year contracts with Comsion Federal de Electricidad (CFE), the national Mexican electric company, which is basing a massive shift to gas-fired electric generation on having access to more low-priced U.S supplies.

Kinder Morgan’s El Paso Natural unit late last year launched a binding open season for its proposed new pipeline that would extend from its south mainline system near Tucson, AZ to the U.S.-Mexico border near Sasabe, AZ. Earlier, the Federal Energy Regulatory Commission (FERC) approved two companion applications to allow El Paso to modify its border-crossing facilities in Arizona.

The blueprint for some stepped-up gas infrastructure work in Mexico is now much clearer, and it bolsters the arguments for industry players who are pushing for a North American pipeline grid in the next decade. Mills’ whiter paper calls for a NAFTA-like energy agreement.

One of the drivers for more U.S. gas imports and infrastructure is the CFE strategy to go through another round of having private sector developers build independent, gas-fired electric generation plants in Mexico, using relatively cheap U.S. gas supplies.

“What CFE is interested in doing is extending the network of pipelines coming in from the U.S. to backstop its gas use for its power plants,” said Dino Barajas, a partner with Houston-based Akin Gump Strauss Hauer & Feld LLP, who has his office in Los Angeles, but serves as the law firm’s Latin American expert, operating out of multiple offices.

“The Ministry of Energy has backed that plan strategically for Mexico, and it is designed to be a great way to maintain low electricity prices in Mexico and continue the build-out of more industrial hubs in northern Mexico,” said Barajas, adding that there is some push for renewables in the form of wind and solar, but “it is going to be difficult for a lot of those projects to compete with gas-fired projects.”

With a track record in Mexico, Irving, TX-based Fluor Corp., the international engineering and construction firm, has a joint venture project in place to build a major ethylene complex in Veracruz. It is a $3.2 billion undertaking that is scheduled to begin operations in 2015. This is one of two current projects that Fluor participates in through a partnership designated as ICA Fluor.

ICA Fluor holds a 20% interest in a joint venture with Brazilian conglomerate Odebrecht (40%) and French-based Technip (40%) to build the ethylene complex for a joint venture between the Brazil petrochemical giant Braskem SA with Mexico’s Grupo Idesa SA de CV. Braskem is the largest petrochemical producer in the Americas. The Ethylene XXI project will include an ethane cracker and three polymerization plants. The project is expected to have an annual polyethylene production capacity of 1 million tons.

After getting base foundations in place and the site cleared, Fluor indicated that the electromechanical assembly phase of the project will kick off shortly.

The master plan for Mexico is that to the extent that the national oil company, Petroleos Mexicanos (Pemex), is able to increase its production of natural gas, there is a market for Mexican natural gas in Central America, because the base fuel for power generation throughout that region is bunker fuel and diesel, according to Barajas.

“So if Mexico can use any increased production of natural gas, Pemex wants to export it into Central America and capture the differential in terms of pricing, and then bring in cheaper natural gas from the United States for power generation in Mexico.”

For all of its size and historic success, Pemex is seen as a bit of a stumbling block for the proponents of a North American gas grid and greatly increased private sector investment in Mexico’s energy infrastructure. At the end of 2012, Moody’s Investor Services hinted at this in affirming Pemex’s “A” credit rating and stable outlook in issuing nearly $2 billion worth of new bonds.

Touted for its 13.5 billion boe of proved hydrocarbon reserves (year-end 2011) and 3.7 MMboe/d oil and natural gas production, Pemex still faces what Moody’s called “numerous operational and financial challenges,” including heavy tax burdens, high amounts of debt and the challenge of growing its oil production – more than half for exports – most of which go to the United States.

“Pemex remains capital-constrained, and its ability to attract capital and technology to the upstream is stymied by Mexico’s prohibition on foreign investment and equity ownership of [Mexican] reserves,” Moody’s said, in its analysis from its Mexico City office.

Sempra officials who are working out the logistics for their two-phase pipeline project and developing what could become a 1,250-MW wind-power development in North Baja California, call Mexico’s natural gas infrastructure “severely constrained,” and predict it will be “a priority for the [new presidential] administration as gas will continue to be the most efficient fuel to generate electricity and a vital supply for industry.”

They cited estimates from the Mexican Energy Ministry that place average annual growth in natural gas and electricity demand at 2.35% and 3.92%, respectively. This provides Sempra with what it acknowledged is an excellent opportunity to expand its already extensive footprint south of the border.

Sempra’s first segment, a 36-inch, 310-mile (500-km) pipeline will run from Sasabe, south of Tucson, to Guaymas, Sonora and will have the capacity of 770 MMcf/d. The new pipeline is expected to begin operations in late 2014.

The second segment from Guaymas to El Oro, Sinaloa, is a 30-inch, 200-mile (320-km) pipeline with a capacity of 510 MMcf/d. The pipeline is planned to begin operations in the third quarter of 2016.

“This new pipeline network will provide reliable access to clean natural gas to CFE’s plants in Sonora and Sinaloa,” said Carlos Ruiz, president and CEO of Sempra Mexico. “We have a long and successful history of safe, efficient and reliable operations in Mexico, and we appreciate the confidence that CFE has placed in us. We look forward to creating new jobs in these communities and improving the local economy for years to come.”

Neither Sempra nor TransCanada are concerned about the logistics of their billion dollar projects. They have the know-how, the materials and the labor force. Gaining the Mexican government’s green light and 25-year contracts with CFE proved to be the key.

“Most of (existing) pipelines, as with the new projects, are underpinned by long-term CFE contracts,” said Dean Ferguson, TransCanada’s vice president for U.S. and Mexico operations. Ferguson emphasized that in the early stages of construction, the sole customer for TransCanada’s two projects is CFE.

As they build projects such as the 330-mile, 30-inch Topolobampo Pipeline, industrial operations along the pipeline route may choose to connect with the new line.

While Ferguson agreed with much of the scenario described by Barajas as Mexico’s long-term energy strategy, he hesitated to embrace the concept of a North American pipe grid. He said there are “combinations of views” on Mexico, some including shale gas development, although he agreed that is an area where the Mexican government has not outwardly focused a lot of attention.

“Certainly, I think there is the recognition in Mexico that they have their own resource [in natural gas], and they should think about how they develop it,” said Ferguson, choosing his words carefully.

“That is one of the reasons that energy reform is one of the key elements that the new president [Enrique Pena Nieto] has highlighted as one of the things he believes is important to the country. What shape that takes obviously has a lot of politics wrapped around it,” he said.

Serving as an important backdrop to the burgeoning energy infrastructure boom is the widely held belief that Mexico’s economy is stable and set to expand rapidly. Aside from the potential future policy reforms in Mexico, from a financing point of view there is a lot of interest from the project finance community, given the infrastructure build-out, according to Barajas.

“There is a huge appetite from the commercial lenders to finance these [new gas and chemical] projects, because in the past they have become very comfortable with financing the power projects in Mexico. They see the country as having a low risk.”

The advent of the pipelines allows the financial people to go into another sector in a country seen as having what Barajas characterized as “very low risk and pretty good returns.”

The Japanese banks are “very interested,” along with Spanish banks, Canada-based Scotia Bank, BNP and others. Depending on the size of the deal and credit quality, you can have other, smaller banks, too, Barajas said.

“There is a lot of capacity available in the market.” Ultimately the added energy infrastructure promises to bring more stability to Mexico’s economy, and that in turn will fuel ore economic growth, Barajas and others surmised.

Richard Nemec is the Los Angeles-based West Coast Correspondent for P&GJ. He can be reached at rnemec@ca.rr.com.

Comments