January 2013, Vol. 240 No. 1

Features

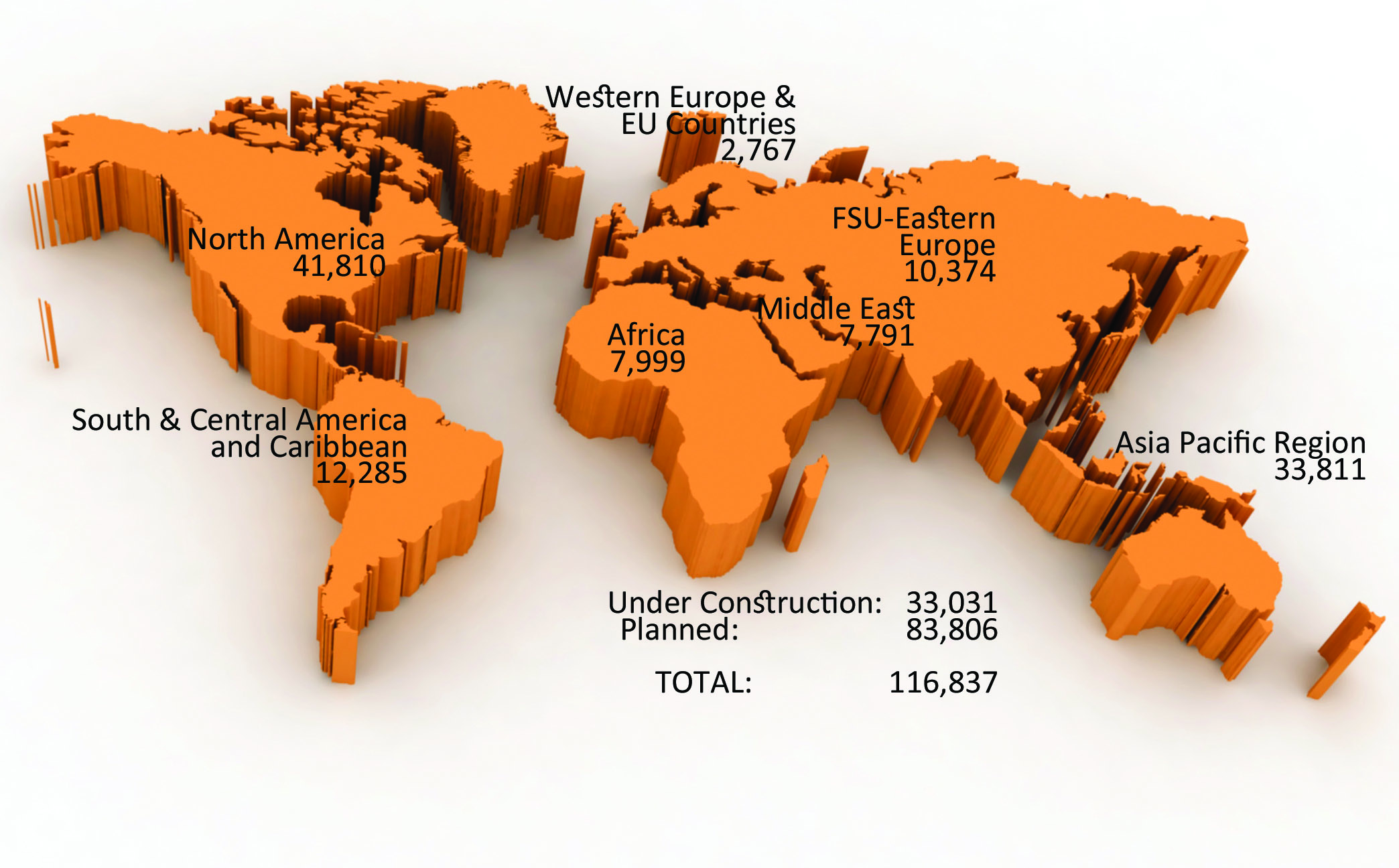

Pipeline & Gas Journals 2013 Worldwide Construction Report

P&GJ’s 2013 survey figures indicate 116,837 miles of pipelines are planned and under construction worldwide. Of these, 83,806 represent projects in the planning worldwide design phase while 33,031 reflect various stages of construction.

Following is a look at new and planned pipeline miles in the seven basic regional groups (see area map). North America – 41,810; South/Central America and Caribbean – 12,285; Africa – 7,999; Asia Pacific – 33,811; Former Soviet Union and Eastern Europe – 10,374 ; Middle East – 7,791; and Western Europe and European Union – 2,767. For information on these and other pipeline projects, see P&GJ’s sister publication, Pipeline News.

North America

The U.S.s’ rising shale gas production is credited with increasing mileage of new and planned pipelines. DTE Energy, Enbridge Inc. and Spectra Energy Corp., plan to jointly develop the NEXUS Gas Transmission (NGT) system to move growing supplies of Ohio Utica shale gas to markets in the Midwest, including Ohio and Michigan, and Ontario, Canada. The proposed NGT project will originate in northeastern Ohio, include 250 miles of large-diameter pipe, and be capable of transporting 1 Bcf/d of natural gas. Targeted in-service date is November 2015.

The Front Range NGL Pipeline that will originate in the Denver-Julesburg Basin (DJ Basin) in Weld County, CO and extend about 435 miles to Skellytown, TX is planned by Enterprise Products Partners, Anadarko Petroleum and DCP Midstream It will provide takeaway capacity and market access to the Gulf Coast. Initial capacity is expected at 150,000 bpd which can be expanded to 230,000 bpd. Enterprise will construct and operate the pipeline which is expected to begin service later this year.

Enterprise continues to expand its natural gas and NGL infrastructure in South Texas and Mont Belvieu, TX to accommodate the Eagle Ford Shale play. Construction is progressing on a 350-mile pipeline, a processing facility and an NGL fractionator at the Mont Belvieu complex. Included in the expansion are two additional pipeline segments totaling 168 miles, of which 26 miles of 24-inch pipeline will extend the mainline to the far western reaches of the Eagle Ford. The remaining 142 miles, to be built in two segments, will comprise 30-and 36-inch line in the eastern portion of the Eagle Ford. A new 64-mile, 30-inch line from the cryogenic facility to its Wilson natural gas storage facility in Wharton County will provide takeaway capacity for residue gas.

Enterprise plans to loop 62 miles of gas pipeline with 24-inch and 30-inch loops. Construction on the expansion is should be ready for operation shortly.

The company has a 173-mile extension of the partnership’s NGL pipeline system under construction from Yoakum, TX to the western reaches of the Eagle Ford in LaSalle County. The pipeline will link to the company’s NGL pipeline system that delivers Eagle Ford production to Mont Belvieu where Enterprise is constructing three NGL fractionators. The extension is set to begin service in the second quarter.

Williams Partners gained approval to expand its Transco natural gas pipeline to provide an additional 250,000 Dth/d of incremental firm transportation capacity to the Northeast. The expansion will primarily consist of 12 miles of pipe at locations in Pennsylvania and New Jersey in addition to a 25,000-hp compressor facility in Essex County, NJ along with other facility modifications. The cost of the project is estimated to be $341 million. It is to be placed into service in November.

Just as the shale boon has increased gas pipeline construction, shale plays are also increasing the nation’s crude oil pipeline construction.

Data from the U.S. Energy Information Administration indicates oil production (including lease condensate) averaged almost 6.5 MMbpd in September 2012, the highest volume in nearly 15 years. The states with the largest increases are Texas and North Dakota.

From September 2011 to September 2012, the EIA reported Texas production rose more than 500,000 bpd as North Dakota production increased by more than 250,000 bpd. Increased production from smaller-volume producing states, such as Oklahoma, New Mexico, Wyoming, Colorado, and Utah, is also contributing to the rise in domestic crude oil production and pipeline construction.

One example is TransCanada’s Gulf Coast project involving a 485-mile, 36-inch crude oil pipeline beginning in Cushing, OK and extending south to Nederland, TX to serve the Gulf Coast marketplace. The 47-mile Houston Lateral project is an additional project under development to transport oil to refineries around Houston.

Construction on the Gulf Coast pipeline commenced August 2012 with an anticipated in service date of mid-to-late 2013. The line will have initial capacity to transport 700,000 bopd and can expand to transport 830,000 bopd to refineries.

In the Gulf of Mexico, Enbridge Inc. will build, own and operate a crude oil pipeline to connect the proposed Heidelberg development, operated by Anadarko Petroleum, to an existing third-party pipeline system. The lateral is expected to be operational by 2016. The Heidelberg lateral will originate in Green Canyon Block 860, 200 miles southwest of New Orleans in 5,300 feet of water. The 20-inch pipeline will be extend 34 miles and is expected to be in service in 2016.

Canada remains fully committed to construction of its1,179-mile Keystone XL Pipeline from Hardisty, Alberta to Steele City, NB. TransCanada indicated it still anticipates approval of the Presidential Permit application – which is required as the pipeline will cross the Canada/U.S. border – in the first quarter of 2013, after which time construction will quickly begin.

TransCanada is active in Mexico where its subsidiary, Transportadora de Gas Natural del Noroeste, will build, own and operate the El Oro-to-Mazatlan pipeline for the Comisión Federal de Electricidad (CFE). The $400 million pipeline project will begin at El Oro and end in Mazatlan, in the state of Sinaloa. The 24-inch pipeline will be 257-miles and have contracted capacity of 202 MMcf/d. The pipeline is expected to be in service in late 2016. It will interconnect with the El Encino-to-Topolobampo pipeline that TransCanada was awarded the contract to build, own and operate. Construction of the two pipelines is supported by 25-year natural gas transportation service contracts with the CFE.

Sempra Mexico’s parent, Sempra International, was awarded two contracts by the CFE to construct, own and operate a 509-mile, US$1 billion pipeline network connecting the northwestern states of Sonora and Sinaloa. The network will be built in two segments that will connect with the U.S. interstate system in Arizona and provide natural gas to power plants. The first segment, a 36-inch, 310-mile line will extend from Sasabe, south of Tucson to Guaymas, Sonora. Its capacity will be 770 MMcf/d. Commissioning is expected by late 2014.

The second segment will extend from Guaymas to El Oro, Sinaloa. It will be a 30-inch, 190-mile pipeline with capacity of 510 MMcf/d. Commissioning is expected in mid 2016.

Caribbean, South & Central America

Planned pipelines continue to outnumber actual mileage under construction throughout this region with Brazil continuing to lead in activity.

As noted by energy experts GBI Research, competition is forcing the global offshore oil and gas industry to undergo a technological revolution in order to access a broader range of reserves, and Brazil is no exception.

The report* states that Floating Production Storage and Offloading (FPSO) technology is playing an increasingly important role in meeting the surging demand for fresh fossil fuel sources in more remote offshore locations. Brazil’s national oil company Petrobras is taking the lead, investing enormous amounts of money to benefit from the FPSO trend.

According to the report, the number of FPSO vessels in Brazil was 32 at the end of 2011, but could expand by 30 by 2017.

FPSO systems are seen as needed to achieve daily production exceeding 1 MMbbls of oil by 2017. Petrobras and partners announced contracts had been approved for $4.5 billion of construction work, for eight FPSOs planned for the Santos basin pre-salt blocks, with the first vessel expected to start production in 2015.

Petrobras is involved in constructing pipelines in support of FPSOs. One project is the contract to Saipem for the Guara and Lula-Northeast gas export pipelines in the Santos Basin, 162 miles off the coasts of Rio de Janeiro and São Paulo, in water depths of 2,100-2,200 meters. The contract encompasses installation and pre-commissioning of a 34-mile, 18-inch line that will connect the Guara FPSO to a subsea gathering manifold in the Lula field and a second 14-mile, 18-inch line to connect the Lula-Northeast FPSO to the same manifold in the Lula field. Offshore activities for both will be performed mainly by the Saipem FDS 2 through 2013.

In Argentina, Rigzone reports national oil company YPF SA wants help from Norway’s Statoil to develop its potentially huge shale gas resources. YPF CEO Miguel Galuccio unveiled an ambitious five-year growth plan that he hopes will lead foreign oil companies to help YPF develop shale gas reserves believed to be the world’s third-largest. Much of this will depend on YPF’s ability to properly exploit the 774 Tcf of gas and 23 Bboe that the U.S. EIA estimates lies trapped in the Neuquen basin.

In other regions, Saipem has contracted with Venezuela’s PDVSA Petroleo S.A. for the Dragon- CIGMA Gas Export Pipeline which is part of the Delta Caribe Oriental project. Saipem will install as 68-mile, 36-inch subsea line to connect the Dragon Platform to the CIGMA complex close to Guiria and in the Gulf of Paria, state of Sucre. Offshore activities will be handled by the Castoro 7 pipelay vessel and should be completed shortly.

Work is under way in southern Peru on the 675-mile South Andean Gas Pipeline, also known as the Gasoducto Andino del Sur. The route starts at the Camisea gas fields in Cusco and then run south through the cities of Puno, Arequipa, Matarani, and Ilo, and may be extended to Tacna. Cost estimates range up to US$3 billion. Constructor Kuntur Transportadora de Gas indicates construction could take three years.

Off Trinidad, Technip was awarded an EPCI contract by BG International for development of the Starfish Field. The field lies at a water depth of 130 meters and will be tied back to BG’s existing Dolphin ‘A’ Platform. The contract includes project management, detailed design and procurement of: a 14-inch, 6-mile concrete-coated production flowline; 7-mile control umbilical; riser and spoolpiece tie-ins; and four flexible jumpers. Offshore installation is expected in mid-2014 with Technip’s G1200 for all pipelay, umbilical lay and heavy lift operations.

Asia Pacific

The Asia Pacific region accounts for 33,811 miles of new and planned pipeline miles, slightly lower than last year when P&GJ reported 34,295 miles.

Several projects involve pipelines of significant length, including China National Petroleum Corporation’s third West-East Gas Pipeline that is nearing construction. With a length of 4,584 miles, the project consists of one trunk, eight branches, three gas storages and one LNG station. The 3,243-mile trunkline will start at Horgos in Xinjiang and end at Fuzhou of Fujian Province, traveling through 10 provinces and regions including Xinjiang. With design pressure of 10-12 Mpa and annual deliverability of 30 Bcm, completion is expected in 2015, joining Line C of the Central Asia-China Gas Pipeline which also is under construction.

Line C covers 329 miles in Uzbekistan. It is estimated that gas supply will commence in January 2014 and reach the designed throughput in late 2015, enhancing transmission capacity of the Central Asia-China Gas Pipeline to 55 Bcm/a.

In India, negotiations are under way for the Indian Oil Corporation (IOC) to acquire a 30% stake in state-owned gas utility Gail (India) Ltd.’s 963-mile natural gas pipeline from Surat in Gujarat to Paradip in Odisha. Gail gained approval to construct the pipeline to connect the west and east coasts in April 2012. The pipeline would have a capacity to transport up to 60 MMcf/d. GAIL will have 36 months to lay the pipeline and commission it.

IOC reportedly plans 1,243 miles of new pipeline projects to expand infrastructure for transportation of crude oil and petroleum products. These include the 435-mile Paradip-Haldia-Budge Budge-Kalyani-Durgapur LPG Pipeline, 183-mile Sanganer-Bijwasan Naphtha Pipeline, 168-mile branch pipeline from Patna to Motihari and Baitalpur, 750-mile Cauvery Basin Refinery to Trichy Pipeline and 250-mile Ennore-Trichy-Puducherry LPG Pipeline.

Gail is developing the Kochi-Koottanad-Bangalore-Mangalore Pipeline that will pass through the states of Kerala, Karnataka and Tamil Nadu. The first phase of 31 miles was completed in 2012. The second 447-mile phase is scheduled to be completed this year.

In Vietnam, the consortium of Chevron, PetroVietnam Gas, Mitsui Oil Exploration, and PTT Exploration & Production Public Co. Ltd. plans to build the 249-mile O Mon Gas pipeline to transport natural gas to fuel the 2,760-MW O Mon power complex. If constructed, it will be one of the longest gas pipelines in Vietnam. PetroVietnam has a controlling stake of 51% in the US$7 billion project. No timeline for has been announced.

Australia

The focus here is on LNG where seven facilities are under construction and six more are planned.

The Queensland Curtis LNG (QCLNG) project being developed by QGC, wholly owned by the BG Group, will be the world’s first project to turn coal seam gas into LNG. The project, under construction since 2010, will provide hydrocarbons for export markets in 2014.

This major, integrated project involves: expanding QGC’s existing coal seam gas production in the Surat Basin of southern Queensland; building a 335-mile natural gas pipeline network linking the gas fields to Gladstone; and constructing a liquefaction plant on Curtis Island, near Gladstone, where the gas will be converted to LNG for export. This is one of Australia’s largest capital infrastructure projects, involving US$20.4 billion of investment.

Australia Pacific LNG is a coal seam gas to LNG joint venture partnership between Origin, ConocoPhillips and Sinopec. In October the first of more than 330 miles of pipe for the project had been laid. The main transmission pipeline will enable coal seam gas to be transported from gas fields in the Surat and Bowen basins to an LNG plant on Curtis Island, off the coast of Gladstone for processing and export. There, the first two gas production trains can process up to 9 Mtpa.

Construction of the Australia Pacific LNG pipeline is expected to be complete in mid-2014.

Also in the region, Shell celebrate the cutting of first steel for the Prelude Floating Liquefied Natural Gas (FLNG) facility’s substructure with joint venture participants, Inpex and KOGAS, and lead contractor, the Technip Samsung Consortium, at Samsung Heavy Industries’ Geoje shipyard in South Korea.

More than 260,000 tons of steel will be fabricated and assembled for the facility. When completed, the Prelude FLNG facility will be 488 meters long and 74 meters wide, making it the largest offshore floating facility ever built. When fully equipped and with its cargo tanks full, it will weigh more than 600,000 tons.

Once completed, the Prelude FLNG facility will be deployed in Australian waters more than 125 miles from shore.This is the first of what Shell expects to be multiple Shell FLNG projects.

Africa

According to GlobalData, production of oil and natural gas from offshore West Africa is expected to increase from 1,564.2 MMboe in 2011 to 2,201.6 MMboe in 2020 at an AAGR of 3.8%. The offshore production of oil and gas is expected to reach 2,011.4 MMboe by 2015 due to production from projects in important producing countries such as Nigeria and Angola. Beyond 2015, production is expected to increase marginally due to the maturing of production fields in Equatorial Guinea, the Republic of the Congo and Nigeria.

Moreover, the new pipelines under construction and planned will ultimately increase natural gas exports from Africa to European markets.

Tanzania announced construction start of the Mnazi Bay to Dar es Salaam Gas Pipeline project in November. The 330-mile pipeline will transport Mnazi Bay gas through a 36-inch line to Dar es Salaam and other major population and industrial centers. Construction is expected to take 18 months.

FSU & Eastern Europe

The most significant report on construction starts in this region came late last year with the announced construction of the long-awaited South Stream Pipeline at Russia’s Russkaya compressor station site near the Anapa, Krasnodar Territory.

The 1,490-mile pipeline will traverse the Black Sea and carry Russian gas via Serbia, Hungary and Slovenia to Italy. The length of the Black Sea section will exceed 560 miles. Its design capacity will be 3 Bcm. First gas supplies via South Stream are scheduled for December.

To feed the required gas to South Stream, Russia’s transmission system throughput will be increased through construction of an additional 1,520 miles of line pipe and 10 compressor stations with total capacity of 1,473 MW. This project id named South Corridor and will be implemented in two phases before December 2019.

In addition to working on diversifying the routes of Russian gas supplies to the EU, Gazprom is anxious to develop its Asian markets. Gazprom announced a $38 billion program to develop an East Siberian gas field and building a pipeline to the Pacific port of Vladivostok to lessen its reliance on exports to Europe. Plans call for an investment of $24.5 billion to build the 2,000-mile pipeline from the East Siberian Chayanda deposit to Vladivostok. The remaining $13.7 billion would be invested in field development.

In the Ukraine, a comprehensive upgrading of a section of the Urengoi-Pomary-Uzhgorod gas trunk pipeline (also known as the West-Siberian Pipeline or Trans-Siberian Pipeline) which carries Russian gas to Europe is under way by Naftogaz Ukrainy. This includes replacing insulation and pipes, modernization and reconstruction of pumping stations. Investments in the first stage, which will require three years, will cost US$539 million. The total cost to upgrade the country’s pipelines is estimated at US$6.5 billion and completion is expected in 2020.

Middle East

The United Arab Emirates recently completed a 248-mile pipeline from the Habshan fields in Abu Dhabi to Fujairah terminal on the Gulf of Oman, which has the capacity of exporting 2 MMbop/d to Asian markets in case of any disruption in shipment through the Strait of Hormuz.

The UAE began operating the pipeline – which was constructed by China – in July. It can export 75% of the country’s oil production which is about 2 MMbpd. The UAE is also increasing Fujairah’s storage and off-loading capacities.

Threats to close the Strait of Hormuz are credited with a move by Saudi Arabia to bypass Gulf shipping lanes. In June Saudi Arabia reopened the Iraqi Pipeline in Saudi Arabia (IPSA), originally built by Iraq.

Saudi Arabia reconditioned the IPSA Pipeline to secure alternative routes to export oil. Tests through the 1.65-MMbpd line delivered crude into storage facilities at Mu’ajjiz near Yanbu on the Red Sea for at least four months, according to published reports.

The IPSA Pipeline is seen as an essential link as more than a third of the world’s seaborne oil exports pass through the narrow Strait of Hormuz from Saudi Arabia, Iran, Kuwait, Iraq, the UAE and Qatar. Qatar’s LNG exports are shipped through Hormuz.

Iraq has awarded South Korea’s KOGAS a $127.5 million contract to construct two 68-mile pipelines linking the cities of Kirkuk and Beiji. The lines will be used to transport liquid and dry natural gas. The lines are slated for completion in late 2014.

Western Europe & EU Countries

While pipeline construction in Western Europe and European Union countries has shown an some increase, the EU seems ready to take a major step to speed up construction by improving its approval process of strategic energy pipelines and grids. Although still requiring final approval of the European Parliament and member states, it could come by spring. The fast-track permitting rules will only apply to the most strategic infrastructure, labeled “projects of common interest” because they benefit more than one member state.

This could include the proposed southern corridor route to bring gas supplies from Azerbaijan and reduce dependency on Russian gas.

As to area activity, Poland’s Gas Transmission Operator Gaz-System has a host of gas pipelines planning, including the cross-border Poland-Slovakia pipeline which will connect the natural gas transmission systems of the two countries, and expansion of the Poland-Czech Republic pipeline. The European Commission is co-financing business and feasibility studies for the two projects.

The parties to the Poland-Slovakia project are Gaz-System S.A. and Eustream – the Slovakian transmission system operator.

Gaz-System accounts for several gas pipeline projects awaiting decisions, including the: 81-mile Zdzieszowice-Wroc?aw pipeline; 32-mile Skoczów-O?wi?cim pipeline; 117-mile Szczecin-Lwówek pipeline; 110-mile Rembelszczyzna- Gustorzyn pipeline; 165-mile Szczecin-Gda?sk pipeline; 105-mile Gustorzyn- Odolanów pipeline; 41-mile Polkowice-?ary pipeline ; and 61-mile Strachocina-Pogórska Wola pipeline.

A significant project awaiting a development decision is the Norwegian Sea Gas Infrastructure project. A spokesperson with Statoil indicated to P&GJ that a decision would be made shortly. The project calls for 312 miles of pipeline to gather gas from the Aasta Hansteen, Linnorm and other discoveries in the Norwegian Sea and piping it to western Norway.

Eleven oil and gas companies are reportedly financing the project of which Statoil is development operator. Start-up is planned in 2016.

*To purchase the GBI Research FPSO Report, phone +44 (0)1204 543 528 or email pr@gbiresearch.com

Comments