August 2010 Vol. 237 No. 8

Features

P&GJs Mid-Year International Pipeline Report

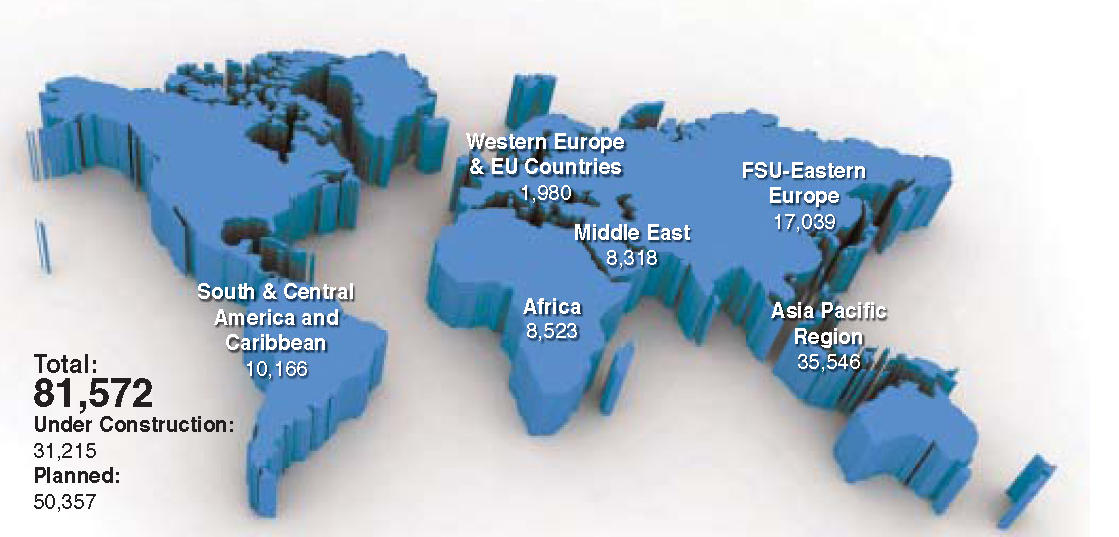

P&GJ’s mid-year international/offshore report shows planned pipeline miles remain higher than actual pipeline construction mileage. Figures show the international sector accounts for 81,752 miles of crude oil, natural gas and refined products pipelines under construction and planned. Of these, 50,355 miles represent pipelines in the feasibility and front end engineering design phase while 31,215 miles account for pipelines in various phases of construction.

The new figures show an 8,872-mile decrease in pipeline miles under construction and planned since P&GJ’s February 2010 report when the international sector accounted for 90,624 miles of new and planned pipelines. Much of the decrease is accounted for in the removal of planned projects which have been delayed or removed after failing to come to fruition. Conversely, pipeline miles under construction rose since February from 24,260 to 31,217.

In identifying areas with high levels of activity, the following reflect new and planned pipeline miles in the six basic geopolitical groupings used in this report (see accompanying map). South and Central America and the Caribbean – 10,166; Western Europe and European Union countries – 1,980; Africa – 8,523; Middle East – 8,318; Former Soviet Union and Eastern European countries – 17,039; and the Asia Pacific region, 35,546. For more information on these and other projects, see P&GJ’s sister publication, Pipeline News.

Energy Demand

Much of the interest in new pipeline construction is driven by rapid growth in energy demand in nations outside the Organization of Economic Cooperation and Development (Non-OECD) nations. With robust economic recovery expected to continue in China, India, and other non-OECD nations, continued rapid growth in energy demand is expected.

In support is the U.S. Energy Information Administration’s International Energy Outlook 2010. World-marketed energy consumption is shown growing 49% between 2007-2035, driven by economic growth in the developing nations of the world, according to the reference case projection from the recently released report. The most rapid growth in energy demand from 2007-2035 occurs in non-OECD nations. Total non-OECD energy consumption increases by 84% vs. a 14% increase among OECD nations.

Asia Pacific

With the Asia Pacific region fast becoming the world’s most significant oil and gas consumer, it is not surprising that the region accounts for the highest number of new and planned pipeline miles. Of 35,546 miles, 18,594 represent pipelines in the engineering and design phase, while 16,952 miles reflect projects in various stages of construction.

As to activity, China, India and Australia continue to be the most active nations in the Asia Pacific region in terms of construction.

Much of the activity in China is driven by state-owned China National Petroleum Corp. (CNPC), the country’s largest natural gas company in upstream and downstream sectors. Earlier this year, CNPC began pre-build activity in preparation for Phase II of the 920- mile Central Asia-China Natural Gas pipeline from Kazakhstan’s Beyneu to Shymmkent. Construction is slated to begin before year-end.

Shortly after placing the second West-East Pipeline in commercial operation, CNPC announced plans to build a third West-East Pipeline to run parallel to the second West-East line terminating in Shandong. CNPC estimates that it will invest $14.6 billion in the project that will have an annual transmission capacity of 30 Bcm/a. There have been proposals for fourth and fifth West-East pipelines which are in pre-feasibility stages.

Analysts also expect India’s natural gas import demand will increase. Several import schemes, including LNG and pipeline projects, have either been implemented or considered.

In northern India, Tractebel Engineering is constructing the $168 million Jagdishpur-Haldia gas pipeline for GAIL (India) Ltd. The 1,274-mile pipeline will carry gas from the Mahanadi and KG basin to the four Indian states of Uttar Pradesh, West Bengal, Jharkhand and Bihar. Completion of the entire project is slated in 2013.

Much of the activity in Australia is closely tied to the eight new LNG terminals that are expected to begin operation by 2015. One project is by Australia Pacific LNG (APLNG), a 50-50 joint venture between Origin Energy and ConocoPhillips, to deliver coal seam gas (CSG) to an LNG plant in Gladstone with processing capacity of up to 18 MMt/a.

Plans call for construction of a 280-mile pipeline from the CSG field to the LNG plant. Construction will start in 2011 with completion in 2013.

Attention is also focused on Queensland as it emerges as one of the most abundant regions for CSG in the Pacific basin. Exploration and development is concentrated in the Surat and Bowen basins where the BG Group subsidiary Queensland Gas Company (QGC) is moving ahead with development of its Queensland Curtis (QCLNG) project to supply CSG from QGC’s Surat basin tenements via a 340-km, 42-inch pipeline to the processing facilities on Curtis Island, near Gladstone. Pending approvals, construction on a liquefaction plant is scheduled to begin in 2010 with first delivery of LNG in 2014.

Arrow Energy has won a license from the Queensland government to develop a pipeline beween the company’s Arrow’s CSG operations in the Surat basin and the proposed Gladstone Fisherman’s Landing LNG project. The 470- km pipeline will extend from Dalby to Chinchilla before moving north to Gladstone. Construction will start in 2011 with first gas supplied to the plant in late 2012.

Overview of the Gorgon Project. (Chevron Graphic)

In western Australia, Chevron Australia and its joint venture partners ExxonMobil, Shell, Osaka Gas, Tokyo Gas and Chubu Electric Power are working on the multibillion-dollar Gorgon Project to develop the Greater Gorgon area gas fields, located 130 km off the northwest coast. It includes construction of a 15 MMt/a LNG plant on Barrow Island and a domestic gas plant with capacity to provide 300 Tj/d to supply gas to western Australia. First gas is planned for 2014.

Gladstone Liquefied Natural Gas (GLNG®) is a pioneering project by Australia’s largest domestic gas producer Santos and Malaysia’s national oil and gas company, Petronas, to convert CSG to LNG.

GLNG involves exploration and production of CSG in the Surat and Bowen basins, a 435-km gas pipeline from the gas fields to Gladstone, and construction of up to three processing trains at an LNG plant and export facility on Curtis Island, off Gladstone. LNG shipments are scheduled in 2014.

FSU-Eastern Europe

Nations in the FSU and Eastern Europe are constructing and planning extensive pipeline networks to reach Europe and the Asia Pacific region. Azerbaijan, Georgia, and Romania want to develop a new transport corridor running via the Caucasus and the Black Sea.

The Azerbaijan-Georgia-Romania Interconnection (AGRI) project envisages construction of two LNG terminals, one in Georgia and one on the Romanian Black Sea coast. The terminals would allow gas from Azerbaijan to flow via pipeline across the Caucasus to Georgia and liquefied at a planned terminal at Kulevi (where Azerbaijan’s state-run oil and gas firm SOCAR has an oil export terminal), then shipped across the Black Sea to the Romania. There, the LNG would be regasified, pumped into the Romanian gas grid, and delivered into the wider European market.

Preliminary estimates for the two LNG terminals are US$5.4–8.1 billion. The AGRI project could transport up to 7 Bcm/y of gas and be finalized in three years.

One of the region’s most notable projects is construction of the Nord Stream Pipeline to deliver natural gas to Europe. It consists of two parallel lines which will be laid across the Baltic Sea from Vyborg, Russia to Greifswald, Germany. The first, with a transmission capacity of 27.5 Bcm/a, is due for completion in 2011. A second parallel line is due for completion in 2012, doubling annual capacity to around 55 Bcm/a.

Total investment in Nord Stream is EUR 7.4 billion. Nord Stream AG is an international consortium whose partners are Gazprom, Germany’s E.ON and BASF/Wintershall and the Dutch company Gasunie.

Western Europe & European Union

While pipeline construction continues to lag in many EU nations, this is expected to change with a decision by the European Commission (EU) to provide US$1.9 billion in grants to ensure that some 30 gas projects are not delayed. Some of the projects to receive the commission grants include the 804-km Interconnector Turkey-Greece-Italy (ITGI) project, 210-km Posiedon Pipeline, 453-km Skanled Pipeline, 3,300-km Nabucco Pipeline and the 210-km Slovakia-Hungary Interconnector, plus upgrades to Slovenia’s transmission system.

One major project recently under way is the 470-km OPAL (Ostsee-Pipeline-Anbindungs-Leitung – Baltic Sea Pipeline Link) in Germany. The starting point is near Greifswald and its termination point is on the German-Czech border near Olbernhau. Once completed, it will connect Germany and Europe to the major natural gas reserves in Siberia via the Nord Stream pipeline. As many as 2,500 workers will work on the pipeline before commissioning in October 2011.

OPAL is owned by Wingas GmbH & Co. KG, 80% and E.ON Ruhrgas AG 20%. OPAL Nel Transport GmbH and E.ON Ruhrgas Nord Stream Anbindungsleitungsgesellschaft GmbH are the network operators.

Work is scheduled to begin in 2011 on the Nabucco Pipeline with first gas expected by 2014. Designed to reduce Euorpe’s dependence on Russian gas, Nabucco will transport gas from Central Asia via Turkey and Austria, bypassing Russia.

Africa

Despite instability continuing to hamper activities in several nations, the region remains important to world energy markets. For this reason, companies continue to work to bring new projects on stream. Among these is a project awarded to China Petroleum Pipeline Engineering to construct the 200-mile Nairobi-Eldoret pipeline for the Kenya Pipeline Company. When completed in September 2011, the line will have capacity of 12.7 MMbpd.

Off Angola, Subsea 7 is working under contract to BP to carry out pipeline engineering, construction and installation for the greater Plutonio development. Subsea 7’s work scope includes installation of a 46-mile, 12-inch gas pipeline, pipeline tie-ins, installing three client-supplied subsea manifold systems and a 3,300-foot umbilical before carrying out the final commissioning in 2011.

A 932-mile pipeline is planned by the Democratic Republic of Congo to carry oil from discoveries in the central basin to the western port of Matadi on the Congo River. To finance the $3.5 billion project, officials plan to seek help from international oil companies, the World Bank and the African Development Bank. Development in the region has been limited by its remoteness, conflict and the global financial crisis.

In Cameroon, Foster Wheeler AG won a contract to carry out pre-front-end engineering design for an onshore LNG plant and offshore gas gathering pipelines and infrastructure on the southern coastline. The Cameroon LNG Project, jointly owned by GDF Suez and Cameroon’s SNH, involves a single-train onshore LNG plant with production capacity of up to 3.5 Mt/a. Foster Wheeler is scheduled to complete the work next year.

Middle East

Although new and planned pipeline projects in the Middle East total only 8,318 miles, several involve sizeable pipeline construction projects. Nacap-Suedrohrbau, the Saudi Arabian subsidiary of Dutch pipeline contractor Nacap, is working to complete a 315-mile, 30-inch multi-products pipeline for Saudi Aramco later this year.

Work is scheduled by China Petroleum Engineering and Construction Corp. on a 487-mile crude oil export line that will link the UAE’s emirates of Abu Dhabi and Fujairah. The International Petroleum Investment Co., which manages global energy investments in excess of $10 billion for the Abu Dhabi government, appointed WorleyParsons Ltd. to carry out the front-end engineering design on the Abu Dhabi Crude Oil Pipeline, or ADCOP project. Completion is scheduled in August 2011.

South & Central America And The Caribbean

This region is starting to see an upturn in construction. Several significant projects are in various stages of construction and South America recently saw its first LNG facility inaugurated. At US$3.8 billion in investment, PERU LNG’s plant is located in the remote Pampa Melchorita area, 170 km south of Lima, and has a capacity of 4.5 Mt/a. Gas will be transported to the plant via a 408-km branch pipeline connecting to the existing Transportadora de Gas del Peru SA, (TgP) pipeline stretching from Camisea to Lima.

Four companies form the PERU LNG consortium set up to develop, build and operate Peru LNG: Hunt Oil Company with a 50% participating interest; SK Energy of South Korea with a 20% participating interest; Repsol of Spain, also with a 20% participating interest; and Marubeni Corporation of Japan, with a 10% participating interest.

Work is slated to start soon on the 674-mile South Andean Pipeline. Peru gave Kuntur Transportadora de Gas, an affiliate of U.S.-based Conduit Capital Partners, the concession to build the gas pipeline and to transport gas in the southern region. Brazil’s construction company, Odebrecht, has joined Kuntur in building the line. Commercial operations are scheduled in 2012.

The proposed Gasoducto Andino del Sur gas pipeline in southern Peru is moving closer to construction. The 1,085-km pipeline would transport gas from central to southern Peru for use in copper mines. The route runs from the Camisea gas fields, located in Cusco, to Juliaca, an Andean city near the Bolivian border.

In Bolivia, pipeline construction is expected to increase with news that YPFB Transport S.A. is planning to invest at least US$141 million in new projects to meet internal demand and exports. YPFB inaugurated the first stretch of the US$172 million, Carrasco-Cochabamba gas pipeline that boosts supply to the west of the country to 130 MMcf/d. The first stretch runs 108 km, and the third stretch – completed last year – runs 65 km. The second and final 78-km stretch is due for completion next year. The company envisions additional expansions with compression stations.

In Venezuela, construction on a $US600 million pipeline project may begin by 2012 following the signing of a Memorandum of Understanding between PdVSA and Russian oil transport company Transneft. Under the agreement, Transneft will construct the infrastructure to develop the Orinoco oil belt, including a 807-mile pipeline. Transneft plans to build a second 435-mile pipeline from the Juni-6 field in the Orinoco belt, which is set to be developed by a Russian consortium under another agreement with PdVSA.

Several projects are slated in Brazil where plans by Petrobras call for five oil products expansion projects involving 1,432 km of new construction. The project include the: 341-km, 14-inch Curtiba to Londrina pipeline; 10-km, 12-inch Londrina to P Eptácio pipeline; 286-km, 12-inch P Eptácio to Campo Grande pipeline; 44 km, 10-inch Campo Grande to Rondonopólis pipeline; and 171-km, 10-inch Rondonópolis to Cuiaba pipeline. No timeline for construction has been announced.

Comments