August 2009 Vol. 236 No. 8

Features

Pipeline & Gas Journals 2009 International Pipeline Construction Report

Once again, international pipeline projects indicate a much higher number of planned pipelines versus actual construction. This is reflected in P&GJ’s latest international survey figures that indicate 85,076 miles of pipelines are under construction and planned at this time. Of these, 17,941 miles account for pipelines in various stages of construction, while 67,135 miles are planned projects.

This year’s figures show pipelines in the engineering and design phase rose 15,979 mile over the past year going from 51,156 miles a year ago to 67,135 miles today. Conversely, the number of actual pipeline miles under construction decreased from 19,015 to 17,941 miles during this same time period.

Despite the fall in new pipeline construction miles, the international sector could see a record number of new pipeline miles constructed in the coming years. Construction of many long-planned projects is expected to be driven by higher energy prices and growing energy consumption.

Supporting this is the Energy Information Administration’s recently released International Energy Outlook 2009 (IEO 2009). The EIA report notes that the current global economic downturn will dampen world energy demand in the near term, as manufacturing and consumer demand for goods and services slows. However, with economic recovery anticipated to begin within the next 12 to 24 months, most nations are expected to see energy consumption growth at rates anticipated prior to the recession.

According to the reference case projections in the report, world marketed energy consumption is projected to grow by 44% between 2006 and 2030, driven by strong long-term economic growth in the developing nations of the world.

The report projects strong economic growth to continue in both China and India over the projection period, with their combined energy use increasing nearly twofold and making up 28% of the world’s energy consumption in 2030.

The report also notes that non-OECD Asia shows the most robust growth of all the non-OECD regions, with energy use rising by 104% from 2006 to 2030. Energy consumption in other non-OECD regions also grows strongly over the projection period, with increases of around 60% forecast for the Middle East and Central and South American and 50% for Africa. A smaller increase, about 25%, is expected for non-OECD Europe and Eurasia (including Russia and the other former Soviet Republics), as declining populations and substantial gains in energy efficiency result from the replacement of inefficient Soviet-era capital equipment.

Construction Overview

P &GJ’s construction report provides details on some, but not all, of the major pipeline projects under construction and planned at this time. In defining areas with high levels of activity, the following reflects new and planned pipeline miles in the six basic geopolitical grouping used in this article (see accompanying map): South/Central America and Caribbean 13,526; Africa 6,253; Asia Pacific 36,133; Former Soviet Union and Eastern Europe 18,797; Middle East 6,232; Western Europe and European Union 4,135. More information is provided in P&GJ’s sister publication Pipeline News.

Asia Pacific

With the demand for energy growing faster in the Asia Pacific sector than anywhere else in the world, it is not surprising that the region also accounts for the highest number of new and planned pipeline projects, which currently total 36,133 miles. Of these, 26,848 miles represent projects in the engineering and design phase, while 9,285 miles account for pipelines in various stages of construction.

As to area pipeline activity, after placing the first West-East gas pipeline into service to deliver 12 Bcm/a from the Tarim Basin, China National Petroleum Corporation (CNPC) launched a second West-East pipeline in February 2008 to carry natural gas from Turkmenistan and China’s Xinjiang Uygur Autonomous Region to the Yangtze and Pearl River Deltas, the country’s two most developed regions. The $20 billion 4,785-mile gas pipeline, with an annual gas transmission capacity of 30 Bcm/a, is scheduled to come online in 2011.

Now, a third West-East pipeline is in the planning phase and a fourth is being considered. According to CNPC, the third project will require an investment of more than $14.6 billion. As proposed, it will have an annual transmission capacity of 20-30 Bcm of gas sourced from Central Asia. The route is expected to start in the northwest region of Xinjiang and run parallel with the second West-East pipeline as far a Jiangxi province in eastern China, from here it will take a different route to its final destination, most likely to the coastal province of Shandong.

Also in the region, China National Petroleum Corp. will start construction in September on the $2 billion oil and natural gas pipelines linking Myanmar and China. Once completed, the pipelines will transport oil from the Middle East and Africa to China and gas from the Southeast Asia to Chinese users.

Plans call for the oil and gas pipelines to run parallel. Both will start on the west coast of Myanmar and enter China at the border city of Ruili in the Yunnan province. The 685-mile oil line will end in Kunming, capital of Yunnan Province. It is expected to transfer 20 million tons of crude to China from the Middle East and Africa annually. The natural gas pipeline will extend from Kunming to Guizhou province and the Guangxi Zhuang Autonomous Region, running a total of 1,744 miles. It is expected to transport 12 Bcm of gas to China every year.

PetroChina is expected to be the holding company for the pipelines being constructed jointly by China, Burma, India, and Korea.

Work is also under way on the China section of the China-Russia oil pipeline that is expected to be put into service by the end of 2010. The 640-mile-long pipeline is designed to transport 15 MMt/a of crude from Russia to China between 2011 and 2030.

In addition to cross-border pipelines, China is building a string of LNG receiving terminals along its coastline to receive cargoes from Australia, Qatar and Malaysia as well as spot supplies.

Elsewhere in the region, the Russian contractor Stroytransgaz is building the Dadri – Bawana – Nangal gas pipeline for Gail (India) Ltd. The 380-mile pipeline will supply gas to the Bawana Power project in Delhi, National Fertilizer Ltd.’s plants in Nangal, Bhatinda and Panipat, and a power plant in Doraha among others. It will connect into the Hazira – Vijaipur – Jagdishpur pipeline.

Also in the region a consortium led by Punj Lloyd has been awarded Malaysia’s largest pipeline project valued at $500 million. The contract for the Sabah Sarawak gas pipeline was awarded by Petronas Carigali Sdn Bdh, a subsidiary company of Petronas, the state oil and gas major in Malaysia.

Work under the contract includes the engineering, procurement, construction and commissioning of the 318-mile, 36-inch diameter onshore pipeline and associated facilities from the proposed Sabah oil and gas terminal in Kimanis, Sabah to the Petronas LNG complex in Bintulu, Sarawak. The project is expected to take 36 months to complete and is scheduled to begin service in March 2011.

The Asia Pacific region also accounts for Reliance Gas Transportation Infrastucture Ltd.’s recently completed 850-mile Kakinada (East-West) pipeline linking West Begal with India’s east coast. In May 2009, BJ Services completed pipeline pre-commissioning and commissioning operations on the pipeline, which is designed for a capacity of 80 MMscm/d.

Australia

In an effort to lead Australia out of its first recession since 1991, oil and gas producers propose projects valued in excess of A$161 billion. While developing the projects is expected to create 50,000 jobs and yield A$10 billion in government revenue, actual construction at this time remains low.

As to projects which are likely to go ahead, Nacap Australia expects to commence installation by mid-2010 on Epic Energy’s QSN3 project. The scope of the project incorporates the looping construction of approximately 584-mile of 18-inch gas pipeline from Wallumbilla in South East Queensland to Moomba in South Australia.

Hunter Gas Pipeline Pty Ltd., a private company, also plans to build the 516-mile Queensland Hunter gas pipeline that will run between the Wallumbilla Gas Hub in Queensland and Newcastle in New South Wales. Construction of the $850 million pipeline is planned to commence in 2010, with first gas deliveries in 2011.

Middle East

Countries in the Middle East are building and planning just over 6,200 miles of pipelines. One of the region’s most notable construction projects is in the UAE where China Petroleum Engineering and Construction Corp. is charged with building the 487-mile Abu Dhabi Crude Oil Pipeline (ADCOP) for the International Petroleum Investment Company (IPIC). The importance of the ADCOP project cannot be under estimated since it will connect Abu Dhabi’s largest onshore oilfields at Habshan to storage and export facilities on Fujairah’s coast and allow up to 1.5 MMbop/d of UAE exports to bypass a chokepoint for international shipping at the Strait of Hormuz. The pipeline is due to become fully operational in August 2011.

In Saudi Arabia, Dutch contractor Nacap-Suedrohrbau is working with Saudi Aramco to help develop a multi-products pipeline from the Ras Tanura Refinery on the east coast of Saudi Arabia via Dhahran to Riyadh in the central region of the Kingdom. The project consists of 315-miles of 30-inch diameter pipelines, three pump stations, metering systems and substations. The pipelines will transport diesel and kerosene from the refineries in RasTanura to Riyadh and also to Dhahran and Al-Hasa along the way. Project completion is slated in December 2011.

Still on the drawing boards is the long-planned Iran-Pakistan-India gas pipeline project. After India refrained from signing an agreement to move the 1,298-mile project forward because of security concerns, Iran is looking at alternative plans for the pipeline, including possibly exporting gas to the UAE, Kuwait, Bahrain and Syria.

In recent weeks, Pakistani Prime Minister Yousuf Raza Gilani has requested the preparation of a feasibility report on the viability of constructing the Iran – Pakistan gas pipeline project along a sea route.

According to local news sources, the potential sea route could save $US2 billion and reduce the pipeline’s length by approximately 93 miles. He has reportedly asked for the feasibility report from Pakistan’s petroleum ministry as he is seeking parliamentary approval for the project.

Africa

Instability in the Niger Delta has caused significant amounts of shut-in production and several companies declaring force majeure on oil shipments. EIA estimates Nigeria’s effective oil production capacity to be around 2.7 MMbop/d but as a result of attacks on oil infrastructure, 2008 monthly oil production ranged between 1.8 MMbop/d and 2.1 MMbop/d. Additional supply disruptions for the year were the result of worker strikes carried out by the Petroleum and Natural Gas Senior Staff Association of Nigeria that shut-in 800,000 bpd of ExxonMobil’s production for about 10 days in late April and early May.

Despite the challenges, Dubai Natural Resources World is teaming up with the state-run Nigerian energy company to bankroll $16 billion worth of oil and gas projects and build at least 1,000 MW of gas-fired power generation. The deal also envisages building new pipelines to distribute gas and possible investments in LNG facilities.

As to area activity, Algeria accounts for several significant projects at this time, including the 120-mile Medgaz project that will link Beni Saf, Algeria to Almeria, Spain, with an eventual extension to France. The $1.2 billion project, expected to be operating by September 2009, will have an initial capacity of 390 MMcf/d, increasing to 1.55 Bcf/d.

Also, Italy’s Snam Rete Gas and the Galsi Consortium have committed to build the 560-mile Galsi pipeline to transport Algerian gas to Italy. The pipeline will have an initial capacity of 770-990 MMcf/d and is expected to be completed by 2012.

Saipem is working under an EPC contract from Sonatrach to build the $580 million GK3-Lot 3 gas pipeline from Mechtatine to Tamlouka in the northeast of Algeria, then connecting the latter to Skikda and El-Kala, located on the northeastern coast of the country, for a total length of approximately 220 miles. The project will allow Sonatrach to expand its gas transport capacity to 9 Bcm/y in order to provide the gas necessary to feed the future Galsi export gas line, as well as the new LNG train in Skikda and two power plants.

Work is also under way off Ghana where Kosmos Energy, Anadarko and Tullow Oil and Gas expect to begin first production from the deepwater Jubilee oil field by the second half of 2010.

In southwestern Chad, China’s largest energy producer, China National Petroleum Corp., began work in July on a major oil pipeline that is due for completion in 2011. Once completed, the pipeline will transport crude from the Koudalwa field some 185 miles south of N’Djamena to the Djarmaya refinery north of the capital. The planned cost of the project hasn’t been disclosed.

Recently approved is the 2,800-mile Trans-Saharan natural gas pipeline to connect Nigeria, Niger and Algeria. Also in recent weeks, energy ministers from the governments of Nigeria, Niger and Algeria approved the construction of the 2,800-mile Trans-Saharan natural gas pipeline that will connect all three countries and come on line in 2015.

While the immense length of the pipeline and the possibility for sabotage are considered major deterrents to the project moving forward in the near-term, both Russia’s Gazprom and French oil company Total have expressed interest in participating in the project that would send up to 30 Bcm/y of gas to Europe from Nigeria via Niger and Algeria.

The European Union says the pipeline could help ease Europe’s dependence on supplies from Russia. Officials estimate the Trans-Saharan pipeline will cost at least $13 billion.

Western Europe/EU Countries

Although this region accounts for just over 4,100 miles of new and planned pipelines at this time,

this could soon change. In January 2009, Russia’s gas monopoly Gazprom turned off gas flowing into Ukraine for transit into Europe for three weeks. Almost one fifth of the EU’s total gas supplies were cut off and half the EU was directly or indirectly affected.

As a result, European Commission President Jose Manuel Barroso is promoting projects to diversify sources and routes of gas supply. In a recent statement he specifically singled out strategic projects in the Southern corridor, such as the 2,051-mile Nabucco pipeline to bring gas from the Caspian region; and projects such as Nordstream to link Germany and its neighbors to new gas sources in northern Russia.

A number of those interconnections and supply routes will be able to get financial support from the EU budget, he said.

One project that could be approved this year is the Trans-Adriatic Pipeline (TAP) to import gas directly into Europe from the Caspian and Middle East, which so far has never reached Europe through pipelines. As proposed, the 325-mile pipeline will have a gas transport capacity of around 10 Bcm/a, with the option to expand to 20 Bcm/a. The EGL Group, which started the project, is expected to make a development decision on the $2.2 billion project later this year.

FSU/Eastern Europe

As the world’s largest exporter of natural gas and the second largest oil exporter, it is not surprising that Russia accounts for an increasing number of projects to increase oil and gas exports to Europe, Africa and the Asia Pacific region. Once again, however, the FSU and Eastern Europe accounts for more planned pipeline miles than actual miles under construction. Of the 18,797 miles of new and planned pipelines, just over 4,000 miles represent work in progress.

Certainly a significant event this year was first oil through the completed portion of the 2,500-mile Eastern Siberia Pacific Ocean (ESPO) pipeline that will connect reserves from Western Siberia to Asian-Pacific markets for the first time. Construction of the ESPO pipeline began in 2006. The project’s first-phase completed earlier this year, extends from Taishet in Irkutsk province to Skovorodino in Amur province. The second, as yet unfinanced phase, will extend the line to the Pacific coast port of Nakhodka.

Even with the first segment complete, crude transported via ESPO will still need to be loaded onto rail and then shipped to market. That limits throughput to only 600,000 bopd — all the rail network in the region can handle. It also limits the customer base to only China, as Russia has not yet built a supertanker port at Nakhodka. This means that the real benefits of ESPO will not likely be realized until another $10 billion investment is made in the ambitious project.

Another project aimed at increasing Russia’s export capacities is the 550-mile South Stream pipeline planned by Russia’s Gazprom and Italy’s Eni. As proposed, the pipeline would connect Russia and Italy via a pipeline under the Black Sea and pass through Central European states, including Bulgaria, Greece, Hungary and Serbia. Cost estimates to construct the project that will have a peak capacity of 31 Bcm/a are approaching $20 billion and climbing.

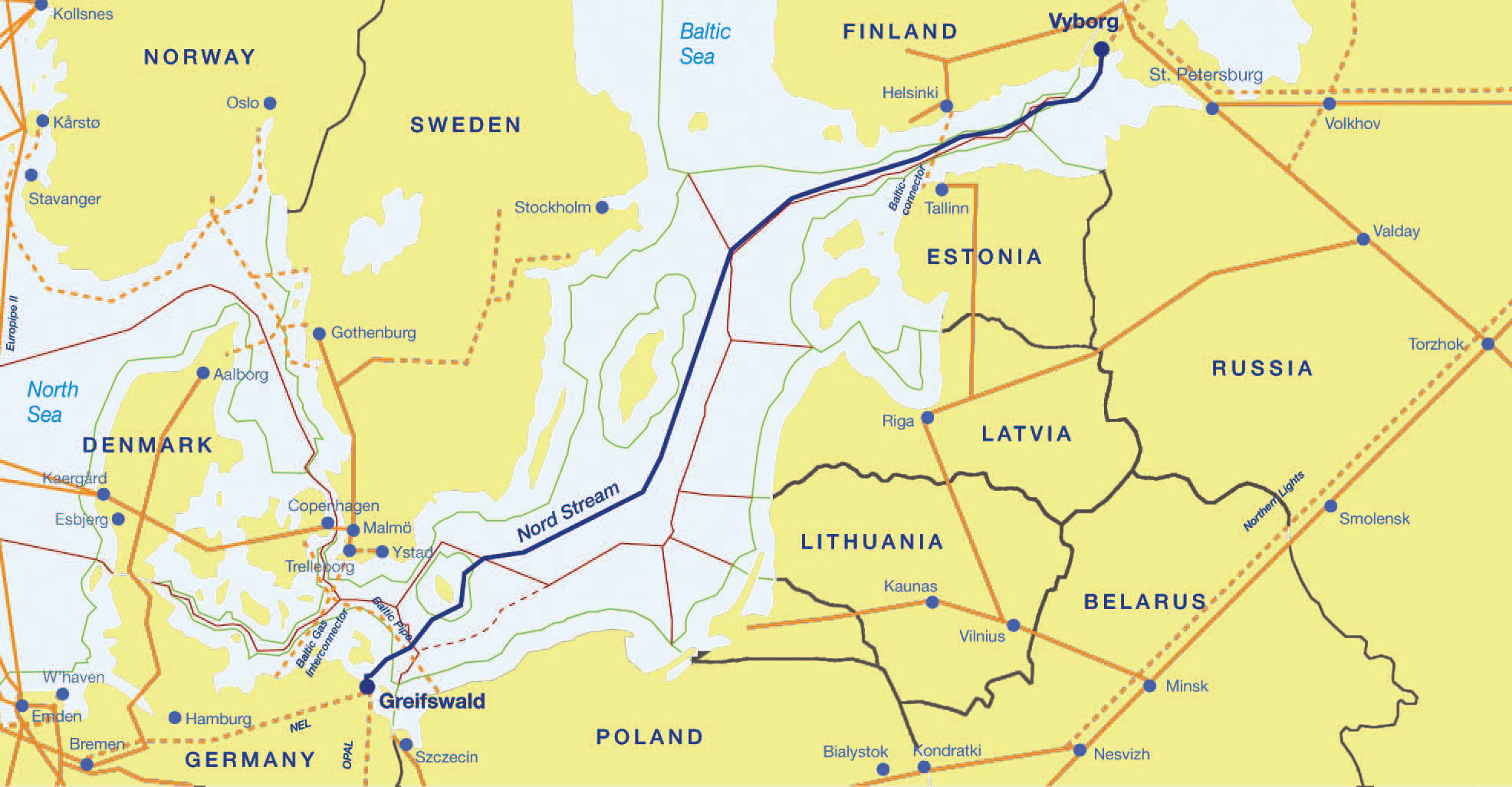

A second major project for gas transmission is the 745-mile Nord Stream pipeline which will run along the bottom of the Baltic Sea, mostly in Finnish waters, from Wyborg, Russia to Greifswald, Germany. Nord Stream is majority owned by Gazprom, which is building it with Germany’s BASF, E.ON, and Dutch Gasunie and has plans to build two parallel gas-pipeline legs of 745 miles each. Once completed, it will have a 27.5 Bcm gas capacity. Work on the second leg of the project is expected to start in 2013.

The third project under planning, the EU-supported Nabucco pipeline run by a consortium led by the Austrian OMV, will carry gas from Caspian Sea fields to the EU. Construction is planned to begin in 2011 and would reach full capacity of 31 Bcm in 2020. The project may, however, be delayed as EU ministers have refused to grant financing.

As to area construction, work on sections of the China-Russia oil pipeline began earlier this year in both China and Russia. The 640-mile-long pipeline is expected to transport 15 MMt/a of crude from Russia to China between 2011 and 2030.

By year’s end, Turkmenistan is scheduled to complete construction of its 120-mile segment of the Turkmenistan-China natural gas pipeline that will transport gas from eastern Turkmen fields and traverse Uzbek and Kazakh territory before reaching Xinjiang in eastern China. More than 745 miles of the 4,350-mile pipeline has already been laid in Kazakhstan and Uzbekistan. The pipeline is expected to be fully operational by 2011. The $9.5 billion pipeline may also be extended to Japan.

Also in recent weeks, oil flowed for the first time through a pipeline that gives China access to Caspian Sea oil fields in Kazakhstan, as part of the expansion of the 1,865-mile Kazakhstan – China oil pipeline. With a designed transportation capacity of 10 MMt/a, the new section runs approximately 475 miles from the Kenkiyak oil field – operated by CNPC – to Kumkol, very close the Chinese border.

Work is also winding down on the 280-mile Atyrau – Kenkiyak section, which would extend the pipeline further west and has a planned transmission capacity of 6 MMt/a.

South/Central America And The Caribbean

The global crisis and stringent nationalistic reforms being imposed by leaders in Venezuela, Colombia, Bolivia and Ecuador are likely to continue to depress pipeline construction in much of this region. For this reason, the number of pipeline projects waiting to be implemented in South/Central American and the Caribbean account for a far greater number of miles than actual construction.

Despite the challenges, Canada-based Pacific Rubiales plans to build an oil pipeline in Colombia with an initial capacity of 60,000 bpd. The 145-mile pipeline will carry crude from fields the company jointly operates with Colombian state oil company Ecopetrol in Rubiales, in the central province of Meta, to a pumping station in Monterrey, a municipality in the eastern province of Casnare.

The pipeline will form part of the country’s current 4,300-mile pipeline network.

Pacific Rubiales’ goal is to transport 100,000 bpd of crude by the end of 2009 and 150,000 bpd by the end of 2010, an amount equivalent to 25% of Colombia’s total crude production. The $530 million pipeline is part of Pacific Rubiales’ planned $1.6 billion investment in Colombia from 2008-2012.

In Trinidad, Technip has been awarded contracts by the National Gas Company of Trinidad to install two pipelines off the islands of Trinidad & Tobago in the Caribbean. The contract covers subsea and land surveying services, environmental, project management and construction management for a large diameter pipeline that will connect the BHP Billiton facility in Block 2C off Trinidad to NGC’s existing pipeline network. The second pipeline will connect BHP Billiton’s facility to the south coast of Tobago to supply gas for a power generation plant under construction by NGC. The pipelines are scheduled to be completed by the end of 2009.

Trinidad energy officials says a proposal for the development of a natural gas pipeline between Port of Spain and Barbados remains on the table, even as it presses ahead with plans to spend $155 million dollars to construct a gas link with its sister island Tobago. The Tobago pipeline is expected to be up and running by the first quarter of 2011. However, Trinidad is currently awaiting word from Barbados on the proposal to extend the pipeline to service the needs of Bridgetown.

This region is also seeing a significant upturn in LNG projects. For example, Peru LNG is a natural gas export project that will support economic growth in some of Peru’s poorest regions and represents the largest foreign direct investment in the country’s history. Totaling $3.8 billion in costs, Peru LNG will be Latin America’s first LNG export project. It includes a liquefaction plant and a marine loading terminal at Pampa Melchorita on Peru’s central coast, as well as a new 255-mile pipeline that will connect to an existing pipeline network east of the Andes. The project is expected to make Peru a net gas exporter after operations begin in 2010.

Moreover, new pipeline projects are under consideration. Kuntur Transportadora de Gas President Samuel Gomez, said development of the Gasoducto Andino del Sur (South Andean Pipeline) is under way and construction is expected to begin next year. The expected route of the $1.billion pipeline will start at the Camisea gas fields in Cusco, and then proceed south through the cities of Puno, Arequipa, Matarani, and Ilo, and possibly further on to Tacna.

The company projects that first gas will be available to customers in 2012 or 2013.

Brazil’s Petrobras has also outlined a number of pipeline projects in its recently released Petrobras Strategic & Business Plan 2009-2013. In the projects in progress portfolio, the 2009-2013 plan includes the completion of 10 gas pipeline construction jobs (1,580 miles in length), the installation of new compression stations and points of delivery, and the enhancement of the capacity of the Bolivia-Brazil gas pipeline (Gasbol) between São Paulo and Paraná by means of new compression stations. The company is expected to invest $4.52 billion in these projects.

Among the main projects in progress at this time is the third and last section of the Southeast-Northeast Gas Pipeline (Gasene), the Cacimbas (ES) – Catu (BA), measuring 588 miles in length. In total, 53% of the project’s construction and assembly have already been completed, and the project is hoped to be wrapped-up in the first half of 2010.

Comments