March 2016, Vol. 243, No. 3

Web Exclusive

High Production, Low Prices Mean Little Change in Natural Gas Storage Capacity

High levels of natural gas production and relatively low natural gas prices are affecting markets for seasonal natural gas storage, including the value of additional storage capacity. For the second year in a row, no new natural gas storage facilities were added, and the slight changes, both positive and negative, at existing storage fields resulted in national storage capacity remaining essentially flat for the year. EIA measures natural gas storage capacity inNovember each year, which is typically when net storage withdrawals begin.

With elevated natural gas production, prices have been low and stable in recent years. Natural gas storage facilities have traditionally served as a physical hedge against high wintertime prices. Storage allows natural gas distributors or large natural gas consumers to buy and store less-expensive natural gas in the summer, and then to withdraw natural gas in the winter, when prices are typically higher. In recent years, however, natural gas prices have been exhibiting decreased seasonality, making some kinds of underground storage less financially attractive.

EIA uses two distinct measures of natural gas storage capacity:

Design capacity is the sum of the working gas design capacity at 385 active storage fields, as of November 2015, as reported in EIA’s Monthly Underground Natural Gas Storage Report. Design capacity is based on the physical characteristics of the reservoir, installed equipment, and operating procedures particular to the site, and is often certified by federal or state regulators. Because of slight changes at existing fields and the deactivation of 10 facilities, design capacity declined slightly, falling 0.2%, from 4,665 billion cubic feet (Bcf) in November 2014 to 4,658 Bcf in November 2015.

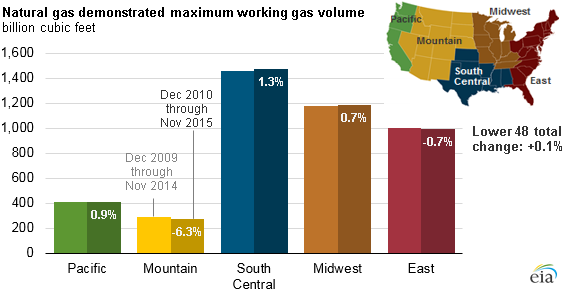

Demonstrated maximum working gas volume is the sum of peak volumes reported by the 385 active storage facilities in the Lower 48 states, regardless of when the individual peaks occurred over the five-year reporting period ending in November 2015. In the graphic below, this measure is compared to the five-year period ending November 2014. At the national level, the difference is small, increasing by just 0.1% from 4,336 Bcf to 4,343 Bcf.

In addition to geographical regions, EIA categorizes storage types based on geology. Traditional storage, such as depleted fields, provides the bulk of storage by volume, and it typically is filled during the spring, summer, and fall, and then is withdrawn during the winter. Traditional storage is slow to fill and deplete, and holders of this natural gas generally prefer to not withdraw too early in the season because it cannot quickly be refilled for later use. However, an increasingly popular type of storage is salt cavern storage, which consists of leached caverns in salt deposits, mostly along the Gulf Coast. While far smaller in volume, salt storage can be cycled in and out many times a year, allowing the stored natural gas to be withdrawn quickly to meet market needs, such as to provide heating during cold snaps or to take advantage of arbitrage when prices spike for other reasons.

Because of this seasonal usefulness, salt facilities in the South Central region saw a significant increase in demonstrated working gas volumes between November 2014 and November 2015, rising by 5.8%, as many salt facilities hit new peak levels in November 2015. By contrast, traditional storage in the adjacent Mountain region saw a significant decrease, falling by 6.3%, because a few facilities that reached peak levels in 2010 are no longer included in the five-year period ending in November 2015.

Principal contributor: Mike Kopalek

Comments