January 2016, Vol. 243, No. 1

Features

State Severance Tax Revenues Decline as Fossil Fuel Prices Drop

Several states that collect significant revenue from fossil fuel extraction are re-evaluating current and upcoming operating budgets and taxation structures to address revenue shortfalls. Severance taxes are often imposed on the extraction of nonrenewable resources such as crude oil, natural gas, and coal. Lower fossil fuel prices, and in some cases, lower production, have led to lower severance tax receipts than were expected when revenue estimates were developed.

Six states strongly affected by this budget squeeze are Alaska, Texas, North Dakota, Wyoming, Oklahoma, and West Virginia.

Alaska. Alaska’s severance tax revenue has fallen further and faster than other states because its tax is based on the operators’ net income rather than on the value or volume of oil extracted. In 2015, when average net incomes after operating and capital expenses were near zero, the state derived practically no revenue from this tax, versus more than $5 billion in 2012. Based on 2014 data, severance taxes accounted for about 72% of the state’s tax revenue. Given the sharp decline in severance tax revenues, the governor recently proposed a 6% state income tax as well as scaling back the payout of dividends to residents from Alaska’s Permanent Fund.

Texas. The comptroller of Texas reports that as of November 2015, revenues from natural gas production and oil production and regulation were down 48% and 51%, respectively, from a year ago. Texas’s economy is more diversified than that of other major oil-producing states, and severance taxes account for a lower percent of its tax total receipts (11% in 2014), meaning Texas can likely respond to the lower severance tax receipts without drastic changes to its enacted 2016 budget.

North Dakota. Despite oil production volumes remaining largely flat throughout 2015, total severance tax revenues fell from more than $3.5 billion in 2014 to $2 billion in 2015 as oil prices declined. The state’s general fund budget collections from July through November 2015, the first five months of the 2015-17 two-year budgeting period, were $152 million, which was 8.9% below the budgetary forecast. The below-budget revenue was attributed to weaker sales tax collections, which are in part driven by oil exploration and production in the Bakken region. If projected revenue remains 97.5% or less of the budgeted amount, across-the-board spending reductions would be imposed for most state agencies.

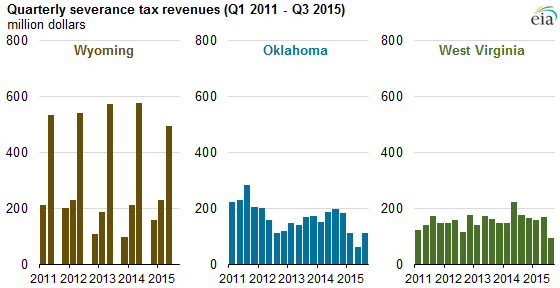

Wyoming. Mineral severance taxes from oil, natural gas, and coal production, along with associated federal mineral royalties, are the primary revenue sources for Wyoming. Severance taxes alone accounted for 39% of the state’s receipts in 2014. However, despite recent increases in oil production, Wyoming is seeing lower revenue projections in response to lower oil prices and declining natural gas and coal production. In October 2015, the state revised its 2015-18 severance tax projections downward by nearly $160 million from January 2015 projections.

Oklahoma. Although severance taxes accounted for 8% of Oklahoma’s revenue collections in 2014, collections from state sales taxes and individual and corporate income taxes are also significantly affected by oil and natural gas prices. The state faces a fiscal year 2017 budget deficit of $900 million on a general fund budget of nearly $7 billion. In December 2015 the state declared a revenue failure, which requires state agencies to reduce spending, and allows for use up to 37.5% of the state’s budget stabilization fund.

West Virginia. Severance taxes accounted for 13% of West Virginia’s tax revenues in 2014. Falling coal production and low natural gas prices in the third quarter of 2015 resulted in the lowest total tax collection since 2008, mostly as a result of decreased severance tax receipts, helping create a projected fiscal year 2016 budget deficit of more than $250 million. West Virginia’s coal production in 2015 was down more than 15% from 2014. Lower natural gas prices have more than offset an increase in the state’s natural gas production, resulting in lower natural gas severance tax receipts. In October 2015, the governor announced 4% reductions to budgets for most state agencies.

Written by Energy Information Administration’s Robert McManmon, Grant Nülle

Comments