July 2015, Vol. 242, No. 7

Features

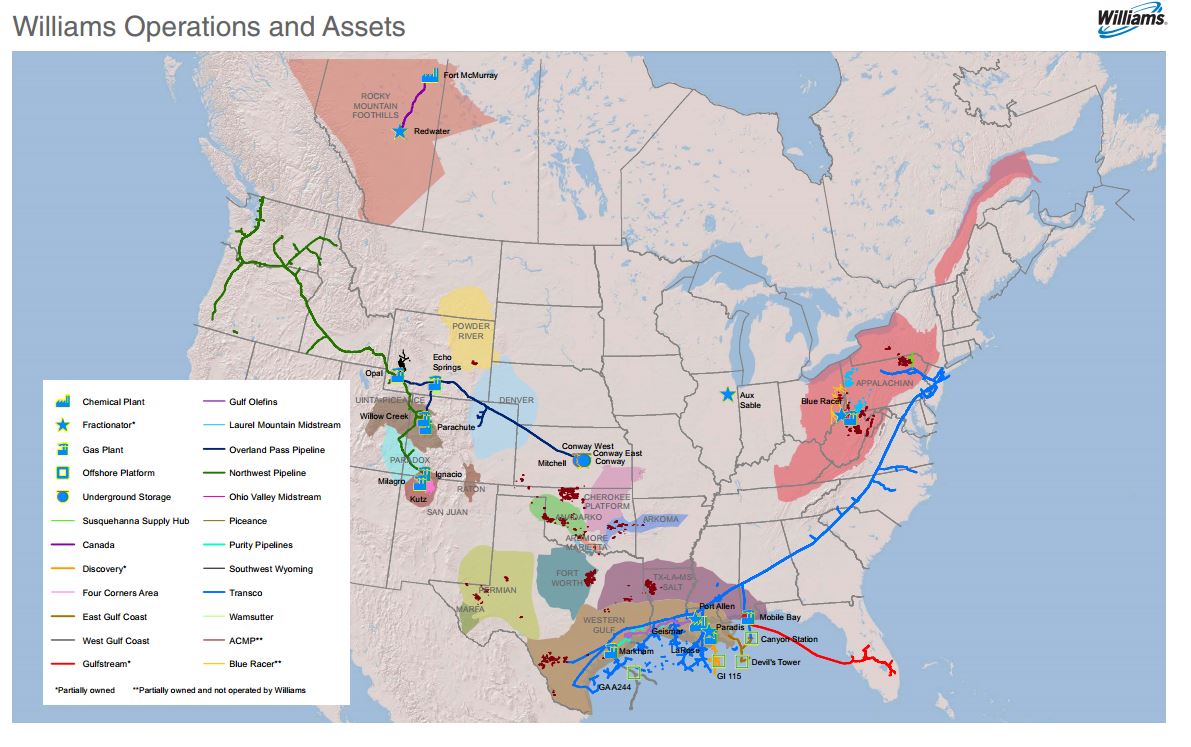

Analysis: Williams Takeover Bid Portends Moves to Come

In the wake of Energy Transfer Enterprises’ (ETE) thus far unsuccessful takeover bid of Williams Cos., some in the industry are predicting more of the same type of activity as cheap energy spurs stronger companies to look for less sound rivals to gobble up.

In fact, some analysts see the ETE offer as an early example of an anticipated consolidation among companies in the fuel transfer business. To some extent, companies that operate pipelines have been spared the pain of the sharp decline of oil prices during the past year. However, observers say enlarging their operations through mergers would be profitable regardless of the price of oil.

“We think there will be more merger activity in the current environment,” Mark Bridgers, a consultant at Continuum Advisory Group, told P&GJ. “Some pundits have forecast that low oil prices will slow down exploration and production activity in the United States and subsequently slow down the pipeline market and the building of new pipelines. We see the opposite as long as oil prices don’t fall and stay below about $50 a barrel.”

On June 22, ETE confirmed it proposed a merger with Williams in an all-equity transaction valued at $53 billion, including the assumption of debt and other liabilities. Williams rejected the takeover offer.

While spurning of the unsolicited offer would be an expected response, at least initially, Williams also said its board of directors empowered the company “to explore a range of stategic alternatives,” which was far from the norm.

“Williams board members know that they have a strong asset base, a good growth plan and good management,” Robert W. Baird analyst Ethan Bellamy told Oilprice.com. “Williams shareholders should go for the best deal from the highest bidder, not necessarily this one, though that might end up being the case.”

Following the public disclosure, Williams stock rose 26% by midday trading to $60, giving the company a market valuation of $45.58 billion. Williams said ETE’s bid significantly undervalued the business, and that it was exploring strategic options of its own.

ETE, a sister partnership to Energy Transfer Partners (ETP), said it offered $64 per share, a 32% premium to Williams’ closing price of June 19.

In a written statement, ETE said it was “disappointed that, despite the best of intentions and its efforts to reach a friendly, negotiated combination, it is forced into a position to publicly confirm its offer for Williams.”

Under the proposal, ETE would acquire all of the outstanding common stock of Williams at a price, representing a 32.4% premium to the Williams common share closing price as of June 19. The ETE deal was dependent on Williams dropping its $14 billion purchase of Williams Partners LP units it doesn’t already own.

“Generally, I have not been supportive of transactions that involve the issuance of ETE units given my belief that ETE units remain significantly undervalued,” said Chairman Kelcy Warren. “However, I believe that a combination of Williams’ assets with ETE will create substantial value that would not be realized otherwise.”

While pipeline operators have been less affected by low prices than exploration and drilling companies, they have had increasing difficulty building pipelines in several areas, in part due to political opposition.

“We see an environment where if oil stays between $50 and $70 it will create significant pressure on existing producers to move from transporting the product via rail into pipelines to lower the overall cost of getting the product to market,” said Bridgers.

In Bridgers’ opinion a potential merger, such as the one between ETE and Williams, is predicated on the view that more pipelines will be built and existing pipelines will have capacity expansions resulting in both more assets and higher prices to move product, all supporting “a long-term higher valuation of pipeline companies.”

ETE said it has made several attempts “over an almost six-month period to engage in meaningful, friendly dialogue with the senior management of Williams, regarding a proposed merger.”

In a statement, Tulsa, OK-based Williams said, the bid “significantly undervalues Williams and would not deliver value commensurate with what Williams expects to achieve on a standalone basis.”

Darren Horowitz, a Raymond James analyst, agreed with the midstream giant’s assessment, telling the Wall Street Journal, “I don’t think that this offer truly reflects the long-term intrinsic value of Williams,” he said.

A public pursuit “will certainly make it more contentious,” Jeff Schmidt, the associate of equity research for Tudor Pickering Holt & Co. of Houston, told the Dallas Business Journal. “That’s my gut instinct.”

The deal would have given ETE access to Williams’ assets in the Northeast. Most of ETE’s operations are in the Midwest and South.

If a deal for Williams takes place it will rank as the largest in pipeline industry history. In 2014, Kinder Morgan consolidation of its partnership assets was valued at $48.9 billion, according to data compiled by Bloomberg.

A merger with Williams would give ETE, which primarily has pipelines in the South and Midwest, substantial holding into the Northeast. Williams’ Transco natural gas infrastructure is among the most critical links from Texas to New Jersey and New York. Williams is also building the 650,000 MMbtu Constitution Pipeline from Pennsylvania’s Marcellus to New York and on to New England.

Just last year, Willians found itself on the other end of a takeover bid, this one successful, when it gobbling up Access Midstream Partners LP in a $6 billion phased acquisition. Some in the industry called it a “monster deal,” and officials inside the company said it made Williams a “natural gas powerhouse,” doubling its gathering volume to more than 11 Bcf/d.

In October, Williams’ master limited partnership (MLP), Williams Partners LP and Access agreed to merge the two MLPs into one entity. The merger was finalized Feb. 3.

Williams used the acquisition to transform Williams Partners LP into a large presence in the midstream space. Senior company officials characterized the move as a chance to provide a clear pathway for growth in what some have dubbed a “super cycle” for U.S. energy expansion.

Ironically, at the end of 2014, Platts’ Global Energy Awards in New York recognized Williams for the “strategic significance and successful closure” of the Access Midstream acquisition, awarding it the “Deal of the Year.”

Richard Nemec, P&GJ contributing editor, contributed to this article.

Comments