February 2015, Vol. 242, No. 2

Features

Pursuing Northeast Gas Pipeline Projects The Hard Way

Developing new natural gas pipeline capacity in the Northeast isn’t easy. Environmental rules are tough, local residents are well-organized, and – in New England in particular – the electricity market structure is not, shall we say, pipeline development-friendly.

Still, with gas needs in the region rising, and all that Marcellus gas close at hand, midstream companies are doggedly and creatively pursuing pipeline projects and making some headway.

It’s no secret the gas pipeline infrastructure that for decades served the Mid-Atlantic states and New England well has needed a major reworking. Back in the pre-shale era, when most people would have guessed that “Marcellus” was a lesser-known Roman emperor, the Northeast as a whole received its gas from the Gulf Coast via long-haul pipelines.

Now, with Marcellus gas production on a tear and gas prices relatively low and stable, the big concern of producers and midstream companies alike isn’t getting Gulf Coast gas to the Northeast, it’s getting Marcellus gas to nearby consumers in New Jersey, New York City and New England, as well as those farther away.

Expanding gas pipelines can have a tremendous effect. New capacity into New York City has eliminated the traditional price premium (or basis) to Henry Hub. Wholesale gas prices in December, for example, were lower in Manhattan than they were in Baton Rouge, LA.

But while some capacity to New England is being added, the Algonquin Incremental Market (AIM) project, for instance, efforts to add game-changing amounts of capacity to the six-state region have been stymied. That major-project logjam may be beginning to break, however.

Before addressing recent developments, a recap of the regulatory politics behind New England’s slow-boat opening up of access to Marcellus gas seems in order.

There are two distinct project types designed to bring more natural gas to New England. The first is backstopped by LDCs that are designed to increase gas supplies to residential and commercial end users and have the regulatory support to make long-term “firm” commitments for pipeline capacity. Two examples of this type of project are the Spectra Energy-owned AIM, which by late 2016 will add 332 MMcf/d of capacity to that company’s Algonquin Gas Transmission (AGT) pipeline network, and Atlantic Bridge, which by late 2017 could add another 582 MMcf/d.

The second and more controversial type of project is based on the premise that New England will need a lot more gas pipeline capacity if regulators and the overseers of the region’s competitive electricity market determine the problem requires a long-term fix to LDCs monopolization of gas deliveries on extremely cold winter days.

For this second type of project, the biggest challenge for midstream companies sponsoring proposals is securing firm shipper commitments from electric power generators to get the pipelines approved by regulators and built. It is this type of project that has seen recent signs of positive developments.

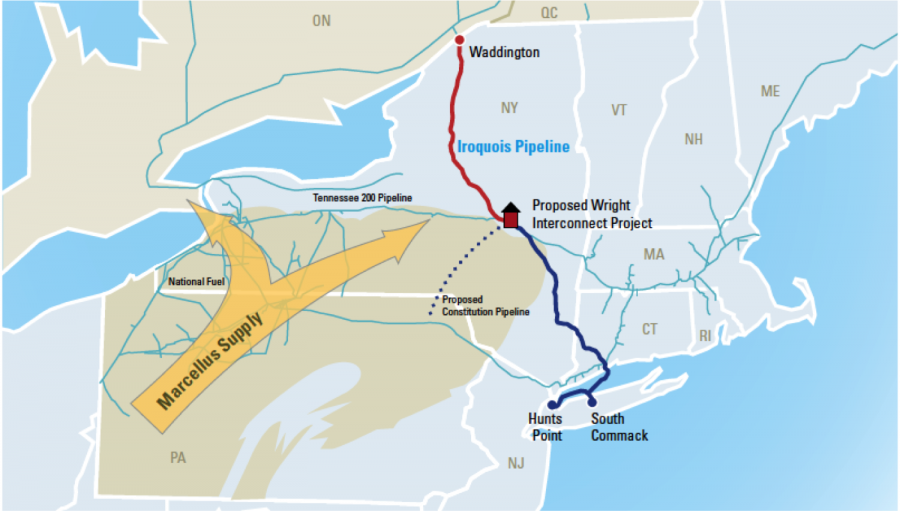

In early December the Federal Energy Regulatory Commission (FERC) approved two key projects (Figure 1) aimed at increasing New England’s access to Marcellus gas: the Constitution Pipeline and the Wright Interconnection Project (WIP).

Constitution, a joint effort by Williams Partners, Cabot Oil & Gas, Piedmont Natural Gas and WGL Holdings, is a proposed 124-mile, 630 MMcf/d pipeline to bring Marcellus supplies from Susquehanna County, PA to Schoharie County, NY (blue dotted line, Figure 1).

Constitution would connect to Iroquois Gas Transmission (IGT) (red and dark-blue lines, Figure 1) via WIP, which would link the Constitution to the IGT and Tennessee Gas Pipeline (TGP) (most of the light blue line, Figure 1) near Albany. This interconnection, known as the Wright Hub, is designed to become the Marcellus gas northern gateway to New England.

Before the recent FERC approval, the Constitution project ran into more than its share of opposition and controversy – many of those fighting the line are environmental groups and local residents also battling to keep hydraulic fracturing out of New York. But the project’s developers persisted, making adjustments to more than half the project’s route to address environmental and landowner concerns.

Constitution’s capacity is fully subscribed, by the way, with Cabot, one of the Marcellus’ largest gas producers, committed to 485 MMcf/d, and Southwestern Energy Services taking the remaining 145 MMcf/d.)

Another potential logjam break is the decision by Kinder Morgan, owner of TGP, in December to propose an alternate, presumably less contentious, route for its proposed Northeast Energy Direct project (Figure 2).

The original proposal would have added 2.2 Bcf/d of capacity from TGP’s 300 Line in the Marcellus in northeastern Pennsylvania to the Wright Hub and then to Dracut, MA, north of Boston. Like Constitution, Northeast Energy Direct (NED) has been facing strong environmental and local opposition, in part because it’s a Greenfield project and not – like Spectra’s AIM project – an expansion of existing pipelines. The first “supply path component” of the pipeline would run 135 miles along a route similar to Constitution’s, from Susquehanna County to Wright.

The second “market path component” of the project would run 188 miles from Wright to Dracut (magenta dotted line, Figure 2). With the newly proposed route realignments, the Wright-to-Dracut leg of NED would move to an existing gas pipeline and electric transmission corridors between Wright and Hinsdale, MA and to existing electric transmission corridors in southern New Hampshire and eastern Massachusetts. By using existing rights-of-way, Kinder Morgan hopes to avoid some regulatory hurdles. Whether that’s enough to satisfy opponents (probably not) or regulators (maybe) remains to be seen.

However, NED’s biggest challenge may be competition from Spectra Energy and Northeast Utilities’ (NU) Access Northeast project, which also moved forward in early December. Access Northeast would add as much as 1 Bcf/d of incremental gas-transmission capacity to Spectra’s existing AGT pipeline and the Maritimes & Northeast pipelines, the latter of which is only partly owned by Spectra. The Access Northeast project appears to have been more successful so far in lining up alliances to attract crucial shipper commitment from power generators.

The recent advance for Access Northeast is that Spectra and NU have formed an alliance with IGT, whose generally north-south pipeline will be receiving Marcellus gas through Constitution. With IGT as a Spectra-NU ally, shippers interested in some of Access Northeast’s capacity will be able to select from multiple receipt points along AGT, including IGT at the Wright Hub and AGT’s other existing, interconnecting pipelines (Texas Eastern, Millennium, TGP, Columbia Gas and Transco).

Still another Access Northeast receipt point is on the horizon: the proposed PennEast Pipeline, which would deliver 1 Bcf/d of Marcellus gas from Luzerne County, PA to the Transco interconnect in northern New Jersey’s Mercer County. Access Northeast’s biggest selling point is that the AGT, Maritimes & Northeast and IGT pipelines are directly connected to nearly three-quarters of New England’s gas-fired generating capacity.

One more thing worth noting is ISO New England, which oversees the regional electric grid, is running an expanded Winter Reliability Program (WRP) to provide incentives to oil and dual-fuel generators to increase oil inventories and – for the first time – to gas-fired generators to contract for LNG to augment pipeline gas.

The final WRP numbers show that by the Dec. 1 deadline the owners of 80 generation units participating in the program have procured about 4.47 MMbbls of oil for use in running oil-fired generators in the event of gas-supply problems, extremely high power demand or a combination of the two. Also, the owners of six gas-fired units have notified ISO New England they have purchased about 500,000 MMBtu of LNG.

The generators’ access to LNG will enable them to produce significant amounts of power even without access to pipeline gas caused by gas-supply issues like those that affected New England last winter. The WRP is just a stop-gap, though – unless, that is, New England decides that, unlike the rest of the country, gas-fired power only needs to be reliable in the spring, summer and fall.

FERC’s approval of the Constitution Pipeline is clearly a step forward in the multi-pronged effort to bring more Marcellus gas into New England, but it’s not a given that either Spectra/NU’s Access Northeast or Kinder Morgan’s NED will advance. The good news is the developers are doing their best to mitigate concerns about the projects’ environmental and other impacts.

That seems to have worked in the case of Constitution. What’s still needed, though, is progress on enabling New England’s power generators to commit to long-term gas pipeline capacity. That’s a tough nut to crack, but the sky-high power costs New Englanders could face this winter may push ISO New England, regulators and others into action.

Comments