Effects of the Clean Power Plan

The Clean Power Plan (CPP) [1] rule, issued under Section 111(d) of the Clean Air Act, is the U.S. Environmental Protection Agency (EPA) program to regulate carbon dioxide (CO2) emissions at existing fossil-fired electric power plants. EPA estimates that the CPP will reduce CO2 emissions from the power sector by 32% from 2005 levels by 2030. As described in the Annual Energy Outlook 2016(AEO2016) Legislation and Regulations section, the CPP rule allows states to choose either mass-based or rate-based emissions targets. A mass-based target simply specifies an annual limit on the amount of CO2 that can be emitted by states from the affected sources. A rate-based target requires states to meet an annual adjusted emission rate (lbs CO2/MWh) based on emissions from affected sources divided by generation from affected sources, which for this calculation includes new non-emitting sources, such as nuclear and renewable capacity, and incremental energy efficiency. The rule also provides flexibility in other areas, such as regional cooperation through trading.

The final rule incorporated in the AEO2016 is a revision to the initial proposal [2] that U.S. Energy Information (EIA) analyzed in May 2015 [3]. The final rule differs from the initial proposal in several ways, including:

- The compliance start date has been delayed from 2020 to 2022, and there are three interim phase-in periods instead of one.

- Demand-side energy efficiency was not used in setting rate-based targets although it still may be used for compliance.

- The variations between state targets have been reduced by using source-specific rates for fossil fuel steam and natural gas-fired combined-cycle generation at the interconnection level, rather than individual state emission rates.

- Compliance calculations for rate-based targets have been limited to capacity additions since 2012, rather than including pre-existing renewable capacity and at-risk nuclear plants.

- Greater detail is provided for mass-based implementation approaches and emissions credit trading.

In comparison with the EIA’s analysis of the preliminary CPP rule, which was based on the Annual Energy Outlook 2015 (AEO2015) Reference case, the analysis described here includes other differences in underlying trends that are unrelated to the CPP but influence compliance decisions. These differences include lower natural gas prices, lower capital costs for renewable electricity generation plants, and extension of renewable tax credits.

In February 2016, the U.S. Supreme Court issued a stay of enforcement of the existing plant rule [4], pending resolution of legal challenges from the states and the affected industries. The AEO2016 Reference case assumes that the CPP will proceed as currently promulgated, and that all states will implement it by using a mass-based standard that caps emissions from both existing and new power plants, with allowance revenues rebated to ratepayers [5]. Alternative cases consider how outcomes could change with different implementation approaches, without the rule in place, and in a scenario with tighter standards beyond 2030.

Reductions in CO2 emissions can be achieved by switching from carbon-intensive fuels (such as coal) to less carbon-intensive natural gas-fired power plants or to zero-carbon technologies (such as renewables and nuclear power). Other options to reduce CO2 emissions include improving plant efficiency to reduce fuel use and increasing energy efficiency to reduce energy demand. Compliance decisions made by the states, as well as any future court decision regarding the rule, would have implications for plant retirements, capacity additions, generation by fuel type, demand, and prices.

ALTERNATIVE CLEAN POWER PLAN CASES

As described in the Legislation and regulations section below, the AEO2016 Reference case assumes that the CPP is upheld, and that all states choose to meet a mass-based standard to cover both existing and new sources. Using the standard that includes new sources ensures that leakage (which would represent a shift of emissions from existing sources to new natural gas-fired sources not covered by the CPP) does not occur. Because EIA’s model is not developed at the state level, and because some level of trading is likely to happen among states with the mass-based approach, the Reference case assumes compliance at the same level in the 22 electricity regions included in the Electricity Market Model (EMM) [6]. An aggregate cap is calculated for each region, with the implicit assumption that carbon allowance trading can occur within the region. The Reference case also assumes that the allowances are allocated to load-serving entities, which provide the revenue back to consumers through lower distribution prices. The cap is specified for 2022 through 2030, based on EPA specifications, and remains flat at 2030 levels thereafter.

No CPP case

The No CPP case assumes that the final CPP rule is permanently voided and is not replaced by other controls on power sector CO2 emissions. States have no federal requirement to reduce CO2 emissions from existing power plants, but other programs remain in place, including the Regional Greenhouse Gas Initiative (RGGI) [7], the California Assembly Bill 32 (AB32), and the Global Warming Solutions Act of 2006 [8]. Also, state and regional renewable portfolio standard programs remain in place, as described in the Legislation and regulations section, and may have an indirect impact on CO2 emissions.

CPP Rate case

The CPP provides state-specific, rate-based targets as an option for compliance. The affected electricity generation used in the rate calculation includes existing fossil steam and natural gas-fired combined-cycle units, incremental renewable generation added since January 2012, incremental nuclear generation, and incremental energy efficiency. Renewable capacity added in the end-use sectors also can be used to offset the affected emissions in the rate calculation. The CPP Rate case assumes that all regions (even those currently under mass-based programs such as in the Northeast and California) choose to comply with the CPP by meeting average rate-based targets—calculated as pounds of CO2 per megawatthour (lb/MWh)—in each EMM region. The rates are based on a weighted average of the state targets, specified by year from 2022 to 2030 as provided in the rule. After 2030, the average emission rates for each region remain constant through 2040, implying that total emissions can increase after 2030 as electricity generation increases.

CPP Interregional Trading case

The EPA allows trading of carbon allowances among states, as long as the states involved use the mass-based compliance option. The CPP Interregional Trading case assumes that all regions choose to meet mass-based targets, covering existing and new sources (as in the AEO2016 Reference case), but with trading of carbon allowances between regions within the Eastern Interconnection and within the Western Interconnection. In the CPP Interregional Trading case, regions that reduce emissions by more than is needed to meet their own regional caps may trade their excess allowances, enabling the purchasing regions to exceed their nominal emissions caps.

CPP Extended case

The CPP Extended case further reduces the CO2 targets after 2030 instead of maintaining a constant standard, as specified in the CPP. This case assumes that the mass-based limits in 2030, which result in power sector CO2 emissions that are about 35% below 2005 levels, continue to decline linearly to achieve a 45% reduction below 2005 levels in 2040. The post-2030 reductions are applied using the same rate of decline for each state.

CPP Hybrid case

Unlike the CPP Rate case, the CPP Hybrid case assumes that regions in which existing programs enforce carbon caps (RGGI in the Northeast [9] and AB32 in California) comply with the CPP through a mass-based target (considered more likely given their public comments on the rule). The CPP Hybrid case also assumes that states in other regions implement the CPP using a rate-based approach. This case assumes no interregional trading for CPP compliance. Because the RGGI and AB32 constraints already are reducing emissions in these regions, the RGGI states and California tend to overcomply with their CPP requirements, whether implemented as a mass-based or rate-based standard. Consequently, the results of the CPP Hybrid case are similar to those of the CPP Rate case, because these regions do not need to behave differently to comply with either a cap or a rate-based standard. The remaining regions are assumed to have rate-based standards in both cases. Because the results are indistinguishable, the following discussion of the case results does not include the CPP Hybrid case.

CPP Allocation to Generators case

The CPP Allocation to Generators case assumes that (as in the Reference case) all regions meet mass-based caps that include new sources; however, the case also assumes that the carbon allowances are allocated to electricity generators rather than to load-serving entities. The CPP Allocation to Generators case also assumes that generators in competitive regions will continue to include the value of their carbon allowances in their operating costs. As a result, marginal generation costs will reflect the costs of allowances. The Reference case assumes that allowances are allocated to load-serving entities, which then refund the revenue from allowance sales to consumers through lower distribution prices. In the CPP Allocation to Generators case, retail electricity prices are higher than in the Reference case because there is no reduction of distribution costs, showing the impact of allowance allocation alternatives on retail prices. Because the impact of the CPP Allocation to Generators case is primarily on retail prices—and not on changes in how compliance is achieved, so that capacity and generation mix results are close to those in the Reference case—this case is discussed primarily in terms of pricing impacts.

Results

CO2 Emissions

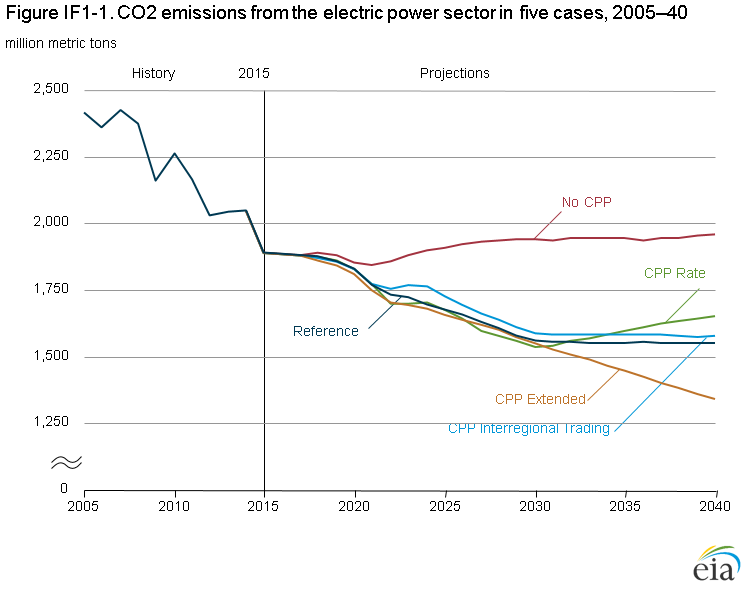

In the Reference case, which assumes that states comply with mass-based CPP requirements, total CO2 emissions from the U.S. electric power sector in 2030 are 35% below their 2005 level. Emissions from the electric power sector, which have historically been the largest source of energy-related CO2 emissions in the United States, fall below those in the transportation sector by 2020 and throughout the remainder of the projection. After 2030, with the carbon cap assumed to remain flat and binding in almost all regions, emissions remain constant through 2040 (Figure IF1-1). Roughly the same reduction is seen in 2030 in the CPP Rate case, consistent with EPA’s intent to develop equivalent measures for the alternate programs. After 2030, emissions increase in the CPP Rate case, and in 2040 they are only 32% below the 2005 total, because a constant emission rate standard can result in increasing emissions when overall generation is growing. Relative to a case without the CPP, the power-sector CO2 emissions are 18% to 21% lower in 2030 across the cases that include the CPP and 16% to 21% lower in 2040 in all CPP cases except the CPP Extended case. The CPP Extended case assumes that further CO2 emissions reductions, beyond those currently specified in the CPP, are required after 2030, to 45% below 2005 levels in 2040, or 32% below the 2040 emissions total in the No CPP case.

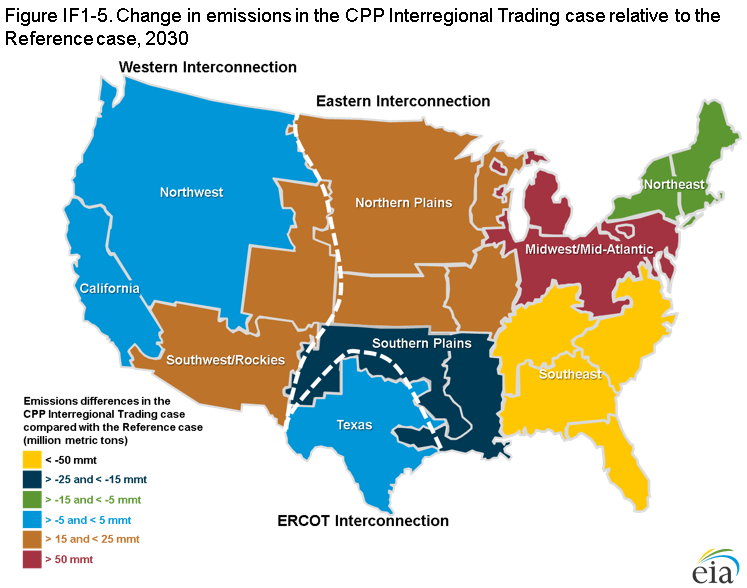

In the CPP Interregional Trading case, emissions are slightly higher than in the Reference case because several regions overcomply, emitting less than their caps. This is typically because of enforcement of other state- or region-specific programs to reduce emissions or encourage renewables. In the CPP Interregional Trading case, where a market exists for those regions to sell their excess allowances, enabling other regions to emit above their caps. As a result, overall U.S. electricity-related CO2 emissions in the 2030–40 projection period are approximately 2% higher in the CPP Interregional Trading case than in the Reference case.

Capacity expansion and retirements

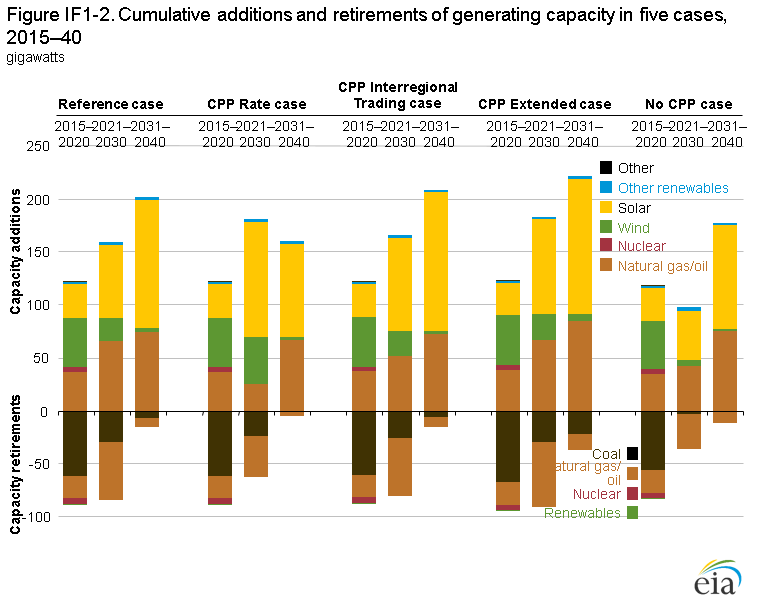

Relative to the No CPP case, the AEO2016 Reference case and the other CPP cases all result in more retirements of coal-fired and other fossil-fired steam plant capacity and increases in total renewable capacity additions, as regions reduce emissions to comply with mass-based or rate-based CO2 emissions standards (Figure IF1-2). The impact on natural gas-fired capacity varies somewhat with the CPP implementation decisions. Natural gas-fired plants produce less CO2 per kilowatthour (kWh) of electricity generated than is produced by coal-fired plants. However, replacement of coal plants with new natural gas plants does not reduce emissions to the same extent as replacement with new renewable plants.

figure data

Of the cases that maintain the final CPP target in 2030, the AEO2016 Reference case (which includes the mass-based approach) has the highest level of fossil-fired capacity retirements and the most new natural gas-fired capacity additions. To comply by EMM region using a mass-based standard, the EMM regions choose to replace existing fossil-fired plants with both new renewable generating capacity and new, more efficient, natural gas-fired combined-cycle plants. In the CPP Rate case, zero-emitting generation can help meet the rate standard both by offsetting emissions and by providing additional affected generation used to calculate the rate. As a result, more new renewable capacity is added than in the Reference case. Natural gas-fired combined-cycle capacity additions are 48 gigawatts (GW) lower than in the Reference case, and fossil-fired capacity retirements are 33 GW lower.

Because the rate standard allows new renewable generation to be included in the base of the rate calculation, additional incentive exists to meet incremental load growth with renewable capacity rather than with natural gas-fired capacity. Consequently, more existing fossil-fired capacity continues to operate. In the CPP Rate case, significantly more wind and solar capacity is added by 2030 than in the Reference case, but less is added after 2030. In the CPP Rate case, less incremental change is required after 2030 to maintain the emission rate standard than is required to maintain the mass-based cap in the Reference case as electricity demand increases.

In the CPP Interregional Trading case, a shift from natural gas-fired additions to renewable additions also occurs. Although regions are still required to meet a mass-based standard in the CPP Interregional Trading case, the ability to trade allowances provides regions that have cheaper renewable sources an incentive to exceed the required standards so they have excess allowances to sell. The availability and costs of renewable energy resources can vary significantly across the country. Broader allowance trading can allow for more economical means to achieve compliance overall. Regions that are best able to lower their emissions can sell allowances to regions that have fewer options to reduce emissions. In the CPP Interregional Trading case, solar capacity additions increase by 31 GW and natural gas-fired additions decrease by 15 GW from the 2040 totals in the Reference case. Also, 5 GW less capacity is retired as more existing capacity remains online in regions that purchase allowances.

In the CPP Extended case, the mix of compliance actions is similar to that of the Reference case, but larger shifts are needed after 2030. From 2015 to 2030, plans for future declines in emissions targets will result in changes to the generation capacity mix, retiring an additional 12 GW of fossil-fired capacity and adding 20 GW of solar capacity beyond the Reference case totals. After 2030, the differences are more significant, with another 21 GW of incremental retirements in the CPP Extended case and additional solar (7 GW) and natural gas-fired (11 GW) capacity.

Generation fuel mix

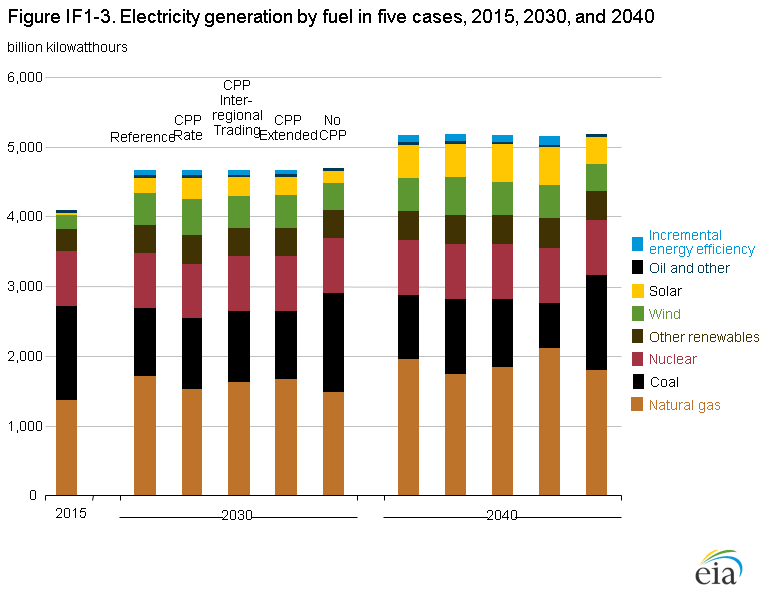

Across the AEO2016 Reference case and CPP cases, shifts in the generation fuel mix reduce coal-fired generation by between 24% and 28% from 2015 to 2030 (Figure IF1-3). The declines from 2015 to 2040 vary across the cases, ranging from 20% to 32% across the cases that keep the CPP target constant after 2030. The rate-based case allows some increase in coal generation in the later years as long as sufficient renewable generation is available to offset it. The mass-based case continues to reduce coal generation and uses lower-emitting sources to meet new demand and maintain the same emission cap. In the CPP Extended case, which assumes that CO2 emissions target continues to decline after 2030, coal generation in 2040 is 52% below 2015 levels. In the No CPP case, coal electricity generation increases slightly from 2015 levels, as natural gas prices increase and as existing coal units are used at higher levels than in 2015, but remains relatively flat after 2020. Most growth in electricity demand is met by generation with natural gas and renewable capacity, which are more economic to build to meet new demand even without the CPP in place.

The tradeoff between natural gas and renewable capacity for compliance in the AEO2016 Reference case versus the CPP Rate case similarly affects the electricity generation mix across the cases. The natural gas share of total electricity generation grows from 33% in 2015 to 37% in 2030 in the Reference case and remains at 33% in the CPP Rate case, while the renewable share grows from 13% in 2015 to 24% in the Reference case and to 27% in the CPP Rate case. The CPP Interregional Trading case provides regions with more flexibility by allowing them to purchase allowances and reduce their own emissions, resulting in more renewable generation and less replacement of coal-fired generation with natural gas-fired generation than in the Reference case. Incremental demand-side energy efficiency (EE), measured as additional to what occurs without the CPP in place, lowers electricity demand by 73 billion kWh to 76 billion kWh in 2030 across the Reference, CPP Rate and CPP Interregional Trading cases. The additional EE impacts the calculation of the achieved emissions rate for a region, as the kWh are included in the denominator of the calculation. However, incremental EE can also help in meeting a mass-based target by reducing the need for additional fossil-fired generation by reducing electricity demand.

The CPP Extended case requires further shifts beyond 2030, resulting in a significant drop in coal’s share of generation, from 33% in 2015 to 21% in 2030 and to 13% in 2040. In 2040, both the renewable share and the natural gas share, at 29% and 42% of total electricity generation, respectively, are higher than those in the Reference case. Incremental EE is also 21 billion kWh higher in the CPP Extended case compared with the Reference case. In 2030, natural gas-fired generation in the CPP Extended case is slightly lower than in the Reference case, as more early development of renewable capacity occurs in anticipation of the declining target.

Electricity prices

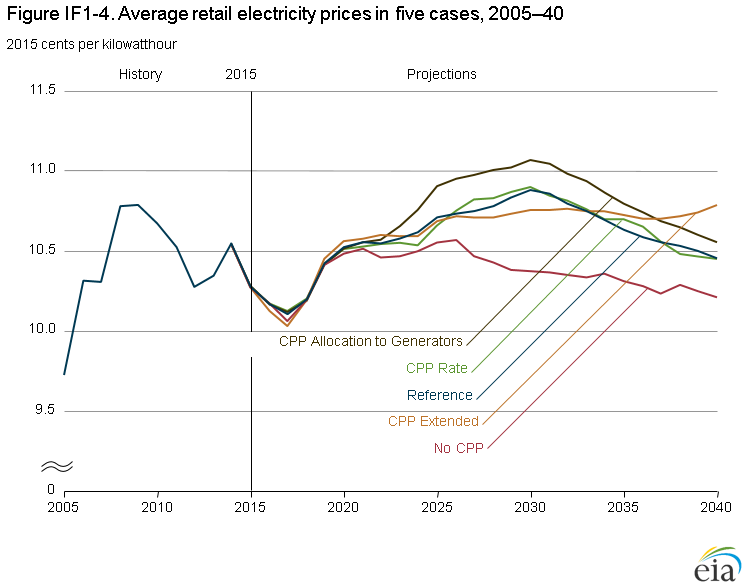

Retail electricity prices are higher when the CPP is in place than when it is not, as the fuel and capital costs of complying with the rule by shifting to natural gas-fired generation, or by building new renewable capacity, are passed through to retail prices. Price impacts are similar in the Reference and the CPP Rate cases, with constant dollar retail prices increasing by 1% to 5% above prices in the No CPP case over the 2022–30 CPP compliance period (Figure IF1-4). Prices remain, on average, 3% higher in constant dollars in the Reference and the CPP Rate case than in the No CPP case after 2030. In the CPP Extended case, average electricity prices are slightly lower than in the Reference case through 2030, as additional renewable capacity is added and as less natural gas-fired capacity is used for generation, with less impact on natural gas prices. Delivered natural gas prices in 2030 are 4% lower in the CPP Extended case than in the Reference case; but after 2030, the CPP Extended case requires further emissions reductions and more natural gas use. In the Reference case, electricity prices decline after 2030. In the CPP Extended case, incremental compliance costs keep electricity prices higher, and in 2040 they are 3% and 6% higher than in the Reference and No CPP cases, respectively.

Under a mass-based standard, states have options for the allocation of carbon allowances, with implications for electricity prices. The AEO2016 Reference case assumes that allowances will be allocated to load-serving entities, which will pass along the revenues from allowance sales to consumers in the form of rebates to lessen the price effects of CPP compliance. This rebate is reflected through lower electric distribution system costs. The CPP Allocation to Generators case assumes that allowances are distributed to generators. As a result, retail prices in competitive regions are higher, and average electricity prices from 2022 to 2040 in the CPP Allocation to Generators case are 1% higher than in the Reference case and 4% higher than in the No CPP case.

Regional Impacts

Electricity generation in 2040 is 17% lower in the Low Electricity Demand case than in the Reference case, with natural gas-fired generation 472 billion kWh lower and coal-fired generation 343 billion kWh lower. Figure IF8-5 shows total electricity generation from the electric power sector and the end-use sectors, with the contributions broken out for natural gas and renewable generation to display the relative levels of generation from the end-use sectors. As in the Reference case, natural gas-fired generation overtakes coal-fired generation by the end of the projection period, but overall shares for both fuels are lower than in the Reference case. In 2040, the coal share of total generation drops from 37% in 2012 to 32% in the Reference case, and to 31% in the Low Electricity Demand case. The natural gas share, which increases from 30% in 2012 to 35% in 2040 in the Reference case, grows to only 32% in 2040 in the Low Electricity Demand case. Because there is less need for new generating capacity, there is less opportunity for growth in natural gas-fired generation from new plants.

Although the targets in the final Clean Power Plan rule have less variability across the states than those in the proposed rule, different reduction levels still are required across the country, and compliance impacts differ among regions. As described earlier, EIA’s modeling assumes that the CPP targets are implemented at the level of the electricity model regions [10] (see Appendix F). To permit a more concise display of the results in the following discussion of regional impacts, these 22 regions are grouped into 9 larger regions, with groupings of neighboring regions that have similar generation profiles and tend to use similar measures for CPP compliance (Table IF1-1 and Figure IF1-5). Detailed results for the 22 EMM regions are available on EIA’s website at http://www.eia.gov/forecasts/aeo/data/browser/.

| Aggregate region | EMM regions included in aggregate region | ||

|---|---|---|---|

| Northeast | 5 | NEWE | Northeast Power Coordinating Council (NPCC) / Northeast |

| 6 | NYCW | NPCC / New York City-Westchester | |

| 7 | NYLI | NPCC/ Long Island | |

| 8 | NYUP | NPCC/ Upstate New York | |

| Midwest/Mid-Atlantic | 9 | RFCE | ReliabilityFirst Corporation–East |

| 10 | RFCM | ReliabilityFirst Corporation–Michigan | |

| 11 | RFCW | ReliabilityFirst Corporation–West | |

| Southeast | 2 | FRCC | Florida Reliability Coordinating Council |

| 14 | SRSE | SERC Reliability Corporation (SERC)/Southeast | |

| 15 | SRCE | SERC/ Central | |

| 16 | SRVC | SERC/ Virginia-Carolina | |

| Southern Plains | 12 | SRDA | SERC/ Delta |

| 18 | SPSO | Southwest Power Pool South | |

| Texas | 1 | ERCT | Texas Regional Entity |

| Southwest | 19 | AZNM | Western Electricity Coordinating Council (WECC)/Arizona New Mexico |

| 22 | RMPA | WECC/ Rocky Mountain | |

| California | 20 | CAMX | WECC/ California |

| Northwest | 21 | NWPP | WECC/ Northwest Power Pool Area |

| Northern Plains | 3 | MROE | Midwest Reliability Council–East |

| 4 | MROW | Midwest Reliability Council–West | |

| 13 | SRGW | SERC/ Gateway | |

| 17 | SPNO | Southwest Power Pool North | |

| Notes: Names of grouped regions are intended to be approximately descriptive of location. Exact regional boundaries do not necessarily correspond to state borders or to other regional naming conventions. Aggregate region data are summed or averaged over the electricity model regions listed. | |||

The current mix of generation types across the regions varies considerably. The Northern Plains, Midwest/Mid-Atlantic, and Southwest/Rockies regions rely the most on coal-fired generation (Table IF1-2 and Table IF1-3). Texas, the Southern Plains, and the Southeast have coal-fired generation in their mixes, along with nuclear and renewables, but these regions rely most heavily on natural gas-fired generation. The Northeast and California have almost no coal-fired generation, and their electricity is generated primarily from natural gas, along with renewables in California and a mix of nuclear and renewables in the Northeast. The Northwest has some coal-fired generation but relies predominantly on hydroelectric and other renewable electricity generation, with a relatively small share of natural gas-fired generation.

| 2030 | ||||||

|---|---|---|---|---|---|---|

| Region | Fuel type | 2015 | Reference | CPP Rate | CPP Interregional Trading | No CPP |

| Northeast | Nuclear | 76 | 63 | 63 | 63 | 63 |

| Coal | 7 | 7 | 6 | 1 | 6 | |

| Natural gas | 130 | 150 | 134 | 135 | 137 | |

| Wind/solar | 9 | 25 | 24 | 24 | 25 | |

| Other | 45 | 51 | 51 | 51 | 51 | |

| Midwest/Mid Atlantic | Nuclear | 275 | 242 | 242 | 242 | 242 |

| Coal | 467 | 270 | 270 | 374 | 445 | |

| Natural gas | 177 | 377 | 308 | 317 | 265 | |

| Wind/solar | 25 | 50 | 145 | 50 | 46 | |

| Other | 27 | 32 | 33 | 32 | 32 | |

| Southeast | Nuclear | 253 | 291 | 291 | 291 | 291 |

| Coal | 230 | 232 | 248 | 165 | 333 | |

| Natural gas | 418 | 480 | 438 | 466 | 395 | |

| Wind/solar | 3 | 79 | 112 | 133 | 64 | |

| Other | 60 | 66 | 66 | 66 | 66 | |

| Southern Plains | Nuclear | 41 | 40 | 40 | 40 | 40 |

| Coal | 108 | 69 | 81 | 53 | 99 | |

| Natural gas | 173 | 221 | 176 | 217 | 177 | |

| Wind/solar | 25 | 67 | 81 | 71 | 69 | |

| Other | 20 | 21 | 21 | 21 | 21 | |

| Texas | Nuclear | 40 | 40 | 40 | 40 | 40 |

| Coal | 84 | 73 | 90 | 73 | 115 | |

| Natural gas | 214 | 230 | 195 | 231 | 230 | |

| Wind/solar | 36 | 97 | 111 | 99 | 60 | |

| Other | 3 | 4 | 4 | 4 | 4 | |

| Southwest/Rockies | Nuclear | 32 | 32 | 32 | 32 | 32 |

| Coal | 112 | 74 | 73 | 93 | 99 | |

| Natural gas | 62 | 60 | 84 | 63 | 67 | |

| Wind/solar | 19 | 87 | 70 | 75 | 71 | |

| Other | 18 | 21 | 21 | 21 | 21 | |

| California | Nuclear | 18 | 18 | 18 | 18 | 18 |

| Coal | 9 | 1 | 1 | 1 | 1 | |

| Natural gas | 116 | 116 | 113 | 110 | 122 | |

| Wind/solar | 32 | 83 | 75 | 82 | 75 | |

| Other | 42 | 68 | 67 | 67 | 67 | |

| Northwest | Nuclear | 9 | 9 | 9 | 9 | 9 |

| Coal | 73 | 52 | 56 | 55 | 56 | |

| Natural gas | 47 | 41 | 45 | 41 | 49 | |

| Wind/solar | 24 | 56 | 53 | 56 | 44 | |

| Other | 121 | 148 | 151 | 148 | ||

Related News

Related News

- Keystone Oil Pipeline Resumes Operations After Temporary Shutdown

- Biden Administration Buys Oil for Emergency Reserve Above Target Price

- Freeport LNG Plant Runs Near Zero Consumption for Fifth Day

- Enbridge to Invest $500 Million in Pipeline Assets, Including Expansion of 850-Mile Gray Oak Pipeline

- Williams Delays Louisiana Pipeline Project Amid Dispute with Competitor Energy Transfer

- Evacuation Technologies to Reduce Methane Releases During Pigging

- Editor’s Notebook: Nord Stream’s $20 Billion Question

- Enbridge Receives Approval to Begin Service on Louisiana Venice Gas Pipeline Project

- Mexico Seizes Air Liquide's Hydrogen Plant at Pemex Refinery

- Russian LNG Unfazed By U.S. Sanctions

Comments