February 2018, Vol. 245, No. 2

Features

Canada’s Evolving Pipeline Infrastructure Picture

Canada’s rather ample portfolio of major energy infrastructure projects, including several pipelines, at the outset of 2018 is defined as much by the projects that fell by the wayside in 2017 as by the still-substantial list of potential new infrastructure investments.

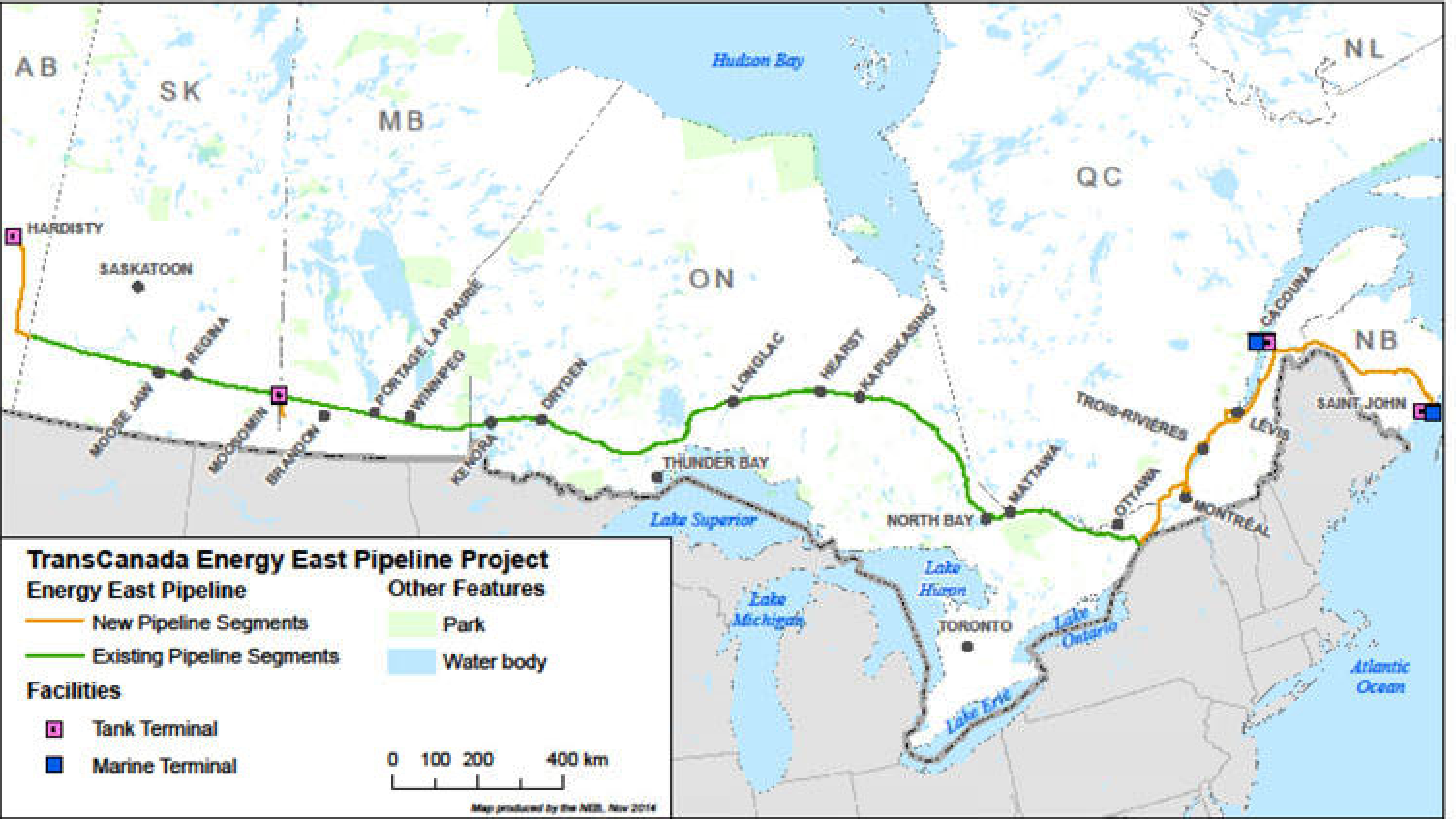

One of the stronger Canadian voices for national energy economic development Cody Battershill, founder of the nonprofit CanadaAction, suggested in an essay near the end of the year that his nation needs a more passionate pursuit of fair trade energy development, as he lamented the demise of projects like Pacific NorthWest LNG and the EnergyEast and Northern Gateway pipelines while a number of Canadian cities were competing to win favors with U.S.-based Amazon.com.

“If Amazon choses Canada, it will be a transformative economic achievement in which [Canada] should take great pride,” the Calgary real estate expert-turned-energy-advocate wrote for energy industry consumption. “But when we show the same passion for fair trade energy as we just have for Amazon that will be the true game-changer.”

The irony for Battershill is that while Canadian cities were working intensely for the chance to help U.S.-based global economic giant Amazon, the now-abandoned TransCanada Corp. EnergyEast oil project would have been 100% Canadian-owned, and it would have “strengthened Canada’s energy security,” according to Battershill, who thinks Canadian energy projects could use some re-branding help.

Thus, from a nationalistic standpoint, there is a little bit of a “chip-on-the-shoulder” approach to what remains of the hottest Canadian projects going forward. Battershill and other energy boosters north of the U.S. border are hoping oil and natural gas as their nation’s largest single economic driver will become even more dominant in the future, helping uplift the national economy, job markets, communities and social programs even. For Battershill energy is an integral part of the Canadian way of life.

If history and the unbroken determination of the nation’s industry are any indicators, Canada promises to keep rolling out major energy infrastructure projects in a changing global and North American socio-political and economic landscape. In mid-November last year U.S., Canadian and Mexican energy ministers met in Houston as part of North American Energy Ministerial to discuss their individual and collective efforts to ensure regional energy security and pursue what they described as their respective “thriving energy sectors that foster economic growth while reducing overall emissions.”

Former Texas Gov. Rick Perry, now U.S. Department of Energy (DOE) secretary, emphasized at the trilateral meeting how the three adjacent nations “share many of the same energy interests and aims,” and how each have “made important contributions to North America’s energy boom.”

Officials in Canada all agree if the major infrastructure projects in their nation advance into construction and completion in 2018-19, they will fulfill Perry’s all-inclusive words. Projects like Kinder Morgan Inc.’s (KM) Trans Mountain oil pipeline, Enbridge Energy Partners Inc.’s Line 3 replacement pipeline and TransCanada Corp.’s well-known Keystone XL project all would help further establish the continental thrust of North American energy almost two decades into the 21st Century.

While there are still plenty of those energy players looking back at the projects like Northern Gateway and EnergyEast that did not advance as planned in 2017, Sonya Savage, senior director for policy and regulatory affairs at the Canadian Energy Pipeline Association (CEPA), says the three major projects out of the West are garnering most of the attention now, but there are smaller natural gas projects, such as some that TransCanada is pursuing in British Columbia that are also important but are falling below the general populous radar.

“TransCanada has some small, but important natural gas projects in northern British Columbia that are important for transporting BC gas into the mainline system, but they don’t get the public play of the large export projects; these are local,” she said. “They are also gas lines, and in Canada we find the media focuses on oil pipelines mostly.”

Savage emphasizes that the three big export liquid projects are still in various stages of development, and each has caused some measure of “excitement” north of the U.S. border. Overcapacity if all three are built is not an issue, she said. “We’re getting proportioning because we don’t have sufficient capacity today to handle production in Canada, and we have a lot of projects upstream in both the Montney and Duvernay shale gas fields being developed.

“All of the pipelines are needed, and the producers certainly want to have options; they don’t want to have every single pipeline full and have proportioning. The three are at different stages so they won’t be built and come online at the same time, and we understand all three could be fully utilized.”

Gavin MacFarlane, vice president and senior credit officer for Moody’s Investor Services’ Toronto office, shares Savage’s enthusiasm for the three liquid pipeline projects teed up to begin construction, if not operations, in 2018, although he also looks back at the failed EnergyEast project as a milepost that is symptomatic of the growing importance of public intervention and community input to major energy infrastructure projects.

Reminding his listener that TransCanada effectively walked away from the eastern oil pipeline project after spending more than $1 billion, MacFarlane called it a “very public and obvious signpost” related to the costs of the increasing difficulty of completing new pipeline projects today.

TransCanada never received a final regulatory decision, and the project languished for a long time, dating back to 2013, said MacFarlane, who keeps an eye on all of Canada’s major rated energy companies and utilities as part of his role at Moody’s.

At the end of 2017 at an investors’ day on Wall Street, TransCanada CEO Russ Girling was emphasizing the so-far smooth integration of the U.S.-based Columbia Gas transmission system into his corporate structure and culture, signaling perhaps that he was not overly dwelling on the hard-to-conclude Keystone XL oil pipeline project, or the loss of Enery East.

Generally in his public presentations, Girling talks in terms of the context of North America, emphasizing that TransCanada, since 2000, has continuously expanded its footprint in the United States and Mexico. “Over the past 17 years, we have invested about $75 billion in high-quality, low-risk pipeline and power generation assets,” Girling told investors in New York.

Looking ahead, TransCanada moved into 2018 with plans to invest about $24 billion in near-term projects over the next five years, Girling said. He noted that under the radar, TransCanada has a host of lesser natural gas infrastructure projects in the U.S. and Canada, totaling $3 billion, that he expected to all come on line in 2018.

TransCanada, even with its recent canceling of Canadian infrastructure projects in western LNG and eastern oil exports, held an enterprise value at the end of 2017 of more than $100 billion, according to Girling. It includes 56,000 miles (90,120 km) of gas pipelines, and is the largest gas storage provider in North America with 653 Bcf of storage capacity.

“Pipelines are not perfect, but we continue to believe that they are by far the safest and most efficient method of moving both natural gas and crude oil,” Girling said, adding that TransCanada’s safety record is “among the best in the world.” It operates $22 billion worth of gas pipelines in Canada, the United States and Mexico.

When Girling talks about growth, he refers to massive additions to an already substantial footprint across North America. These projects are expected to double TransCanada’ earnings before interest, tax, depreciation and amortization (EBITDA) in the next three years, Girling told analysts at the end of 2017. It is expected to grow from $5.9 billion to $9.5 billion in 2020.

A marker for the much touted and maligned Keystone XL (KXL) project in 2018 is for TransCanada to make a final investment decision (FID) for the project. Moody’s MacFarlane said that the timeline for moving the project forward even with a disputed final state OK from Nebraska continues to be an issue. Uncertainty has plagued the northern segment of the project in the United States for years.

“From Moody’s and a ratings perspective, we have never included KXL in any of our forecasts, MacFarlane said. “We’ve always felt there was too much uncertainty, and the company was never far enough along for us to fully include it in our forecasts. We took a position that this was never a done-deal.

“We still don’t include it, and we won’t until the company makes the FID and all issues are fully resolved. It would be premature to include it in our forecasts, and I could probably point to a number of equity holders that take the same approach.”

In 2018, for TransCanada’s officials and Canadian energy industry advocates, KXL is a proposed 36-inch crude oil pipeline that carries tremendous economic consequences. It runs from Hardisty, Alberta in the heart of the oil sands production and would extend to Steele City in Nebraska, where it would connect to the existing KXL system stretching to the U.S. Gulf Coast. Canadians view it as “critical infrastructure” for both economic strength and energy security.

As Girling and his supporters began 2018, they reiterated this project will get built, and it will encompass “enhanced standards, powerful technology and independent [third-party] reviews that ensure it is built and operated to uphold a fundamental commitment to safety.”

Kinder Morgan Inc. (KMI) executives and their supporters echo the same assurances concerning the Trans Mountain oil pipeline export project that has faced local concerns and opposition inside of Canada in Burnaby, B.C., despite federal approvals by the National Energy Board (NEB) dating back to 2016 following a 29-month review process.

The local objections are centered on the project’s need for expanding almost threefold the local terminal operations rather than the $7.4 billion, 715-mile (1,150-km) pipeline itself that parallels the existing oil line that has been operating since 1953. The project plans to add 609 miles (980 km) of new pipeline and re-activate another 120 miles (193 km) of existing line. Supporting this pipeline expansion will be 12 new pump stations, 19 new tanks at existing storage terminals and three new berths at the Westridge Marine Terminal.

At the end of 2017, KMI CEO Steve Kean indicated capital spending on Trans Mountain will remain modest until the final permitting hurdles are cleared, and he gave no specific predictions at the time when that was likely to be in 2018. KMI has about $2.2 billion set aside for growth capital in 2018 related to part of its natural gas Gulf Coast Expansion Project on its Natural Gas Pipeline Company of America system, and another $1.9 billion in capital expenditure (capex) funds primarily for Trans Mountain.

“We are assuming that for the first part of 2018 we’ll be engaged in what is primarily a permitting-only spend; it is not exclusively for permitting, but primarily so,” Kean told analysts at the Wells Fargo Securities 2017 Pipeline, MLP and Utility Symposium. “The main reason for that is we are seeking to get additional clarity on permits and approvals and appeals in the first part of 2018, and once we get that clarity we will be in a position to either push spending further out [in time], or we will be accelerating our spending if we have what we think is a clear line of sight into getting into active construction.”

To put that in context, Kean said that when KMI is ready for a full-construction mode, it will be spending $200-$300 million monthly, compared to what is now a $30 million a month spending rate. “We’re not going to increase our monthly spend rate [by up to 10 times] unless we are clear that we can finish what we start,” Kean said. “We’ve sought that clarity in recent regulatory filings in the context of getting permits in Burnaby, and have a backstop to the municipal and provincial permitting process at the NEB.”

“We’ve also have a federal appeal ongoing of the order we received already approving this project as ‘in the Canadian national interest’,” said Kean, calling Trans Mountain “a valuable project.” Kean told his investors’ audience at the end of 2017, that the oil pipeline project was crucial to Canada and to shippers who he characterized as “suffering a netback that is more than $20 behind an international oil price” that the KMI pipeline would help alleviate.

Similar responsiveness to western Canadian crude producers is found in Enbridge’s Line 3 replacement project from Hardisty to Superior, WI, in the United States, 1,031 miles (1,659 km) of 36-inch pipe with $2.9 billion in investment just in the U.S. portion of the project from the Canadian border to the Wisconsin interconnection. The project already had been delayed twice going into 2018, having originally been scheduled to be in service by late 2017.

As of late 2017, industry analysts were placing the target startup date for the second half of 2019. Enbridge officials tout the project’s “significant benefits,” representing a “major enhancement” of its liquids pipeline system. “The increased reliability of throughput on our system will provide customers with greater certainty of service to key markets, and it aligns well with our Number One priority of safety and reliability,” said an Enbridge spokes representative.

Liquids pipelines and terminal assets are part of what Enbridge CEO Al Monaco calls the company’s “crown jewels” that are assets he intends to nurture and enhance going forward.

Natural gas pipelines and storage, along with the company’s two gas utilities are the other crown jewels, he said. While telling investors in late 2017 at a company hosted session on Wall Street that the company’s assets are projected to grow to $170 billion, Monaco reiterated that the current regulatory and permitting environment is a difficult one in which to complete major infrastructure projects.

In the opening weeks of 2018, Line 3’s fate sits with the Minnesota state regulatory commission where the five-member panel is on a path to make a final decision on the 337-mile (542-km) portion of the international line within its state boundaries by May 1, following an administrative law judge’s recommendation expected by the end of the first quarter in 2018.

For Canadian projects moving through parts of the United States there are distinct differences in theory regarding the national and local/state/provincial approaches to regulation. “Approvals in Canada all reside at the federal level while in the United States, individual states have a lot more autonomy and make decisions that directly affect the pipe projects,” Moody’s MacFarlane said. “That’s not to say that the provinces in Canada don’t have a lot of say in the process, but ultimately the decisions in Canada are made at the federal level. That’s an important distinction between the two countries.”

Both Trans Mountain and Line 3 are approved, and KXL is approved in Canada as well. Parts of Line 3 in Canada are already under construction. The $8.2 billion Line 3 project is the largest in Enbridge’s history with a $5.3 billion Canadian portion and $2.9 billion for the U.S. segments. In total, Line 3 replacement will fully replace 1,031 miles (1,660 km) of Line 3 with new pipeline and associated facilities on either side of the Canada-U.S. international border.

“There are a lot of jobs, a lot of local taxes – national and provincial – and we project a decrease in the differentials and an uptick in the price of oil,” CEPA’s Savage said. “There are big benefits to the country just from the pipelines, not counting the upstream sector that will fill the lines. They are in the national interest for the country.”

While economics and energy security continue to drive new projects forward, the boarder regulatory, political and global crosswinds will continue to be factors, and how much buffeting they contribute in 2018 to new energy development is still an unknown. CEPA’s Savage said the regulatory process is a work in progress, particularly in light of the Trudeau administration now running the national government. North American Free Trade Agreement (NAFTA) negotiations go on, and regulatory processes under Prime Minister Justin Trudeau will change, but in the end CEPA and the rest of the Canadian energy industry is seeking more certainty in the regulatory process.

“We as an industry are trying to assure that at the end of the day the process that unfolds has enough certainty to proceed and for investors to have enough confidence to build in Canada,” Savage said. “The fact that there are major projects proceeding shows that there are markets; they don’t proceed until they have shippers. It speaks to the supply being needed.”

In Keystone and Line 3 there are a lot of jobs and construction on the U.S. side as well.

“The U.S. and Canada have always been pretty good trade partners. These projects are important to the United States and its economy,” he said. “They are getting their energy products from a neighbor who shares their concerns about a clean and healthy environment.”

Canadian energy advocates are confident that time is on their side, whether it relates to global oil prices or LNG export projects. As Savage said, “the world is continuing to need hydrocarbons.” P&GJ

Richard Nemec is a regular contributing writer to P&GJ based in Los Angeles. He can be reached at rnemec@ca.rr.com.

Comments