April 2018, Vol.245, No.4

Features

Capacity Center’s Annual Top 20 Pipeline Capacity Traders

By Michael Reed, Managing Editor

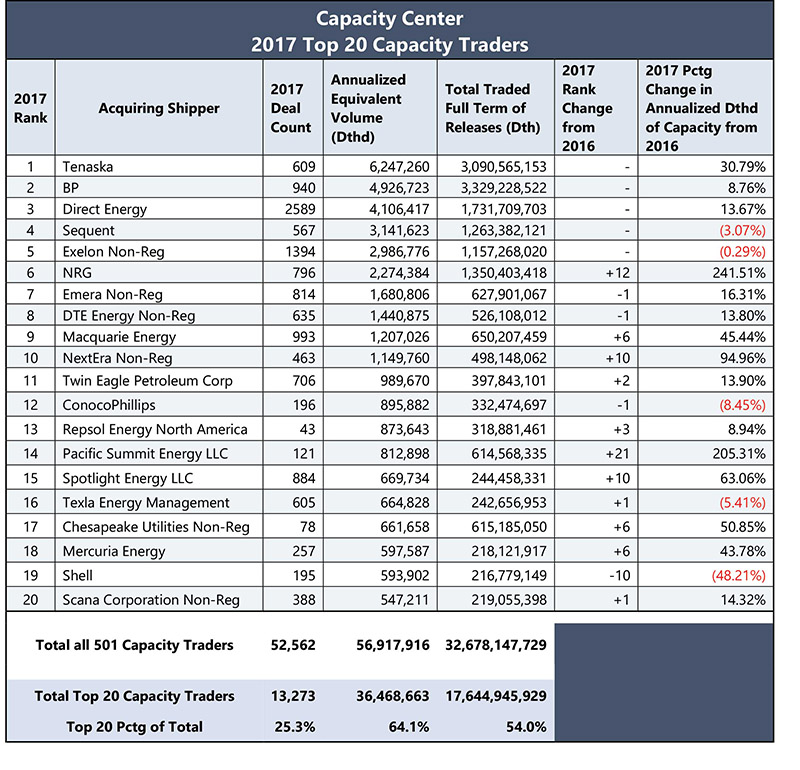

Once again, Tenaska emerged as the top trader on Capacity Center’s annual listings, acquiring almost 6.25 Dth/d of annualized capacity during in 2017. The change represented an almost 31% increase over the previous year.

While the Top 5 in 2017 were unchanged from 2016, there was movement and jockeying in the sixth through 20th positions. Notably however, five companies in the top 20 traded less in 2017 than in 2016. Among the other 15, most saw increases in traded volume from just under 8% to over 240%.

Rounding out the Top 5 were BP, which came in second with 4.93 Bcf/d; Direct Energy, third with 4.11 Bcf/d; Sequent, fourth with 3.14 Bcf/d; and Exelon Non-Reg (Constellation), a close fifth with 2.99 Bcf/d.

“Although the five companies at the top have maintained their places from 2016, there was a lot of movement among the other 15 and most saw increases in traded volume.” said Greg Lander, president of Capacity Center’s parent company, energy consultant Skipping Stone.

The biggest upward movers, according to Capacity Center, were Pacific Summit, 21 slots, from 35th place in 2016 to 14th place in 2017 and NRG up 12 places into 6th place. For NRG, the upward movement represented a whopping 241% increase in annualized capacity.

Both NextEra and Spotlight Energy moved up 10 spots to 10th- and 15th-place, respectively.

Of course, where there are gains, there are also decreases, with the biggest decline shown by CenterPoint Non-Reg, which fell 68 spots from 8th to 76th. Others companies leaving the Top 20 were Concord Energy Trading, EDF North America and Infinite Energy – all of which slipped into upper-Top 20 spots.

Overall, for 2017, there were 52,562 transportation capacity trades between non-affiliated entities, according to Capacity Center. This excluded trades to effectuate merger and acquisition (M&A) transactions. This trade count represented an 11% increase over the 47,398 trades during calendar year 2016.

Top Pipeline Traded

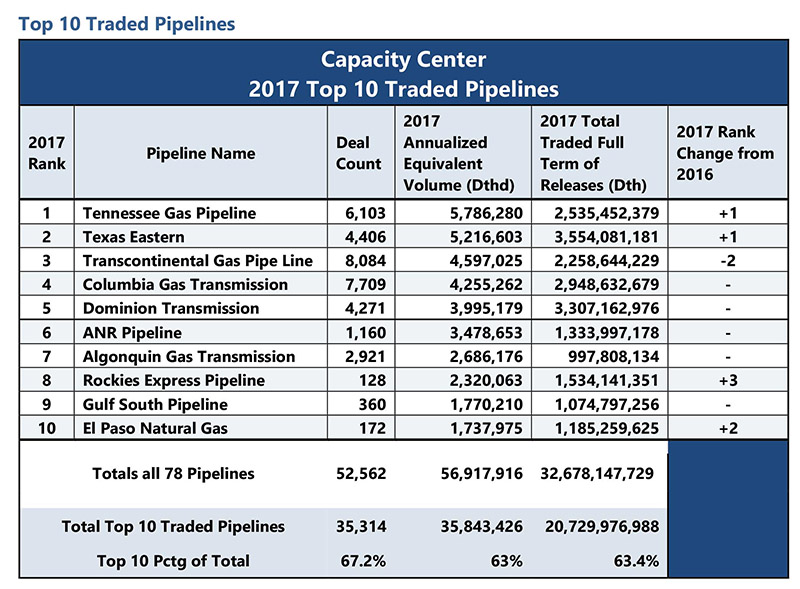

In addition to the Top 20 Traders, the report listed the Top 10 pipelines traded, which saw over 35.3 Bcf/d, an increase of nearly 20% over its previous 30 Bcf/d of annualized capacity. The 10 pipelines represented 63% of the total traded on all pipelines.

Topping the other pipelines in annualized traded capacity for 2017 was Tennessee Gas Pipeline, displacing perennial leader Transco with 5.8 Bcf/d in traded capacity. Rounding out the Top 5 were Texas Eastern at 5.2 Bcf/d, Transco slipping to third at 4.6 Bcf/d, Columbia Gas at 4.3 Bcf/d and Dominion at 4.0 Bcf/d.

The Top 10 pipelines accounted for more than 35,000 separate trades, or 67% of the total number of trades, according to Capacity Center.

For the year, there were 501 “distinct trading partner company groups” trading more than 56.9 Bcf/d of annualized transportation capacity on 78 pipelines, a 13% increase in annualized volume over the previous year’s 50.3 Bcf/d.

Forward Capacity Trading

For 2017, Capacity Trading Report analyzed the trend toward forward market trading in capacity, looking at two forward market time frames:

Case 1 – the number, duration and traded quantities of deals entered into 60 days or greater before the traded capacity became effective

Case 2 – The same criteria for deals entered into between 30 and 59 days. before the traded capacity became effective

In Case 1, 101 trading companies did forward market capacity trades that became effective 60 days or greater from trade date to effective date. The average number of days across the entire group for forward trading Case 1 was 203 days in advance of the capacity becoming effective. Among the Top 10 forward market Capacity Traders, the average forward trade date of their Case 1 deals was 248 days.

The total number of long-dated forward deals in 2017 (Case 1, plus Case 2) was 641 up from less than 500 in 2016 for an increase of 28%, and the Top 20 forward deals comprised 61% of this total. At the same time, the annualized volume increased 21% to 4.45 Bcf/d, or 7% of all traded capacity. This was up almost 15% over 2016, and just ahead of the overall market’s year-over-year 13% volume traded growth.

Even more interesting, the report said, was comparing the volumes between Cases 1 and 2. The annualized Dth/d of capacity for deals starting 60 days or more into the future was 4.45 Bcf/d, which greatly exceeded 1.82 Bcf/d, the quantity traded in deals effective between 30 and 59 days in advance of effective date.

The combined results show 6.25 Bcf/d, or 11%, of all capacity traded in 2017 were deals done 30 days or more prior to release dates. This is a slight increase from just over 10% last year.

“This apparent, slight relative growth of the forward market may indicate that traders are approaching parties with capacity already sold to lock up that capacity when current deals roll-off,” Capacity Center said. “In future reports, we will keep a close eye on trends that may develop, especially once the current build-out rush is completed.” P&GJ

Editor’s note: In compiling its rankings, Capacity Center analyzed over 1,200 companies that acquired capacity to affiliated company groups. Those results are reported as totals by parent company rather than each affiliate or subsidiary. Capacity Center then divides those groups into regulated and non-regulated when a group has both regulated and non-regulated affiliates or subsidiaries.

Comments