August 2017, Vol. 244, No. 8

Features

Natural Gas Putting Israel and Egypt on Energy Leader Board

Israeli Pipeline Prospects Politically, Economically Complex

Israel’s desire for increased energy security, alongside the opportunity of importing natural gas through the planned Arish-Ashkelon gas-pipeline in the 1990s, encouraged the adoption of that fuel. Between 2008 and 2012, the Arish-Ashkelon pipeline brought Egyptian gas to Israel. LNG imports began in 2013 via the offshore Hader Deepwater LNG Terminal.

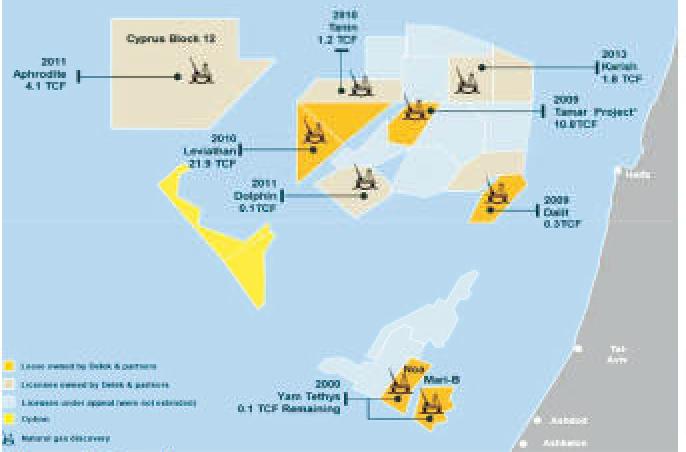

The new millennium inaugurated a series of small offshore gasfield discoveries culminating in the 10.8 Tcf Tamar field that came online in 2013, and the 21.9 Tcf Leviathan field that will be fully on stream in 2019, (Figure 1.)

Increasing availability of natural gas and its adoption for electricity generation saw consumption rise from 5.2 Bcm in 2010 to 9.8 Bcm in 2016. By 2020, consumption of natural gas is expected to reach 12.5 Bcm, climbing to 18 Bcm by 2030, of which 85% will be accounted for by electricity generation and industry, according to the Israeli Ministry of National Infrastructure, Energy and Water Resources, (Figure 2).

LNG imports enter the maritime portion of Israel Natural Gas Lines natural gas transmission system. Offshore gas is collected by pipelines owned and operated by field operators and enters the state-owned gas pipeline network whose 530-km pipelines service major cities, power stations and industry, (Figure 3).

The company is in the midst of expanding its network to serve the Jerusalem area, new towns and power plants that are converting to natural gas.

Reaching Markets

With the prospect of increasing natural gas supplies from a fully operational Leviathan in 2019, Israel can satisfy rising domestic demand as well as export to close neighbors such as Jordan, Egypt and the Palestinian Authority with whom it already has gas-supply agreements. In addition, exports to Western Europe and Turkey are being proposed. Although access to its close neighbors would be primarily by overland pipelines, Egypt is already connected by a subsea pipeline, and more distant markets could be accessed by subsea pipelines or by LNG tanker.

Pipeline Gas Exports

Egypt, Jordan, Turkey and Europe are considered the main market prospects for the Israeli gas and accessible by pipelines.

Completed in 2008, the 62-mile subsea Arish-Ashkelon pipeline connects Israel’s gas distribution network with Egypt’s. With up to 1.7 Bcm annual capacity, it supplied 40% of Israel’s natural gas needs until 2012 when the Egyptian government canceled exports in favor of its own market situation.

With an acute shortage of natural gas, the Arish-Ashkelon pipeline could be swiftly reversed to allow Israeli gas to flow to Egypt in the first instance, at least until Eni’s super-giant 30 Tcf Zohr field comes fully online in 2020. Thereafter, Israeli gas could be converted to LNG at underused liquefaction plants near Port Said or near Alexandria for export to third markets.

Concerning Jordan, a 2016 report, Israeli Gas: Too Soon to Declare Victory, by the German Marshall Fund, found that in business terms, the nation is “an obvious market.” Pipeline distances, it noted, are short — measuring “in mere tens of kilometers” at potential linkages between the Israeli pipeline network and that of Jordan.

Additionally, the largest prospective customer, national electric power company NEPCO, is “a reliable partner with a reputation for ensuring its customers pay their bills.” The 2014 supply agreements for Tamar and Leviathan will be implemented by two new pipelines, the report said.

Construction of a pipeline in the Sdom area by the Dead Sea is underway to link the Tamar gas fields with the Jordan market. The deal by Delek and Noble Energy, the lead operators of the Tamar field, will supply $500 million worth of natural gas over 15 years to two private Jordanian companies — Arab Potash and the Jordan Bromine — according to Reuters. In February, the Tamar partners also signed a letter of intent to supply private customers in Jordan with 1.8 Bcm of Tamar gas over a 10-year period.

A second pipeline will be built in the Beit Shean area to deliver 45 Bcm of natural gas, valued at over $15 billion, during a 15-year period, from the Leviathan field to NEPCO, reported the Jerusalem Post.

Turkey also could receive gas from the Leviathan field by the end of 2020, according to Yossi Abu, chief executive of Delek Drilling and Avner Oil. This would come through a new 500-km (300-mile) pipeline. Turkey, with rapidly rising demand, is looking to reduce its reliance on expensive Russian pipeline gas and improve its energy security with new sources of supply. However, relations between Cyprus and Turkey will have to stabilize first.

In April, Israel reached a preliminary agreement with Cyprus, Greece and Italy to export Israeli and Cypriot natural gas via a planned $6 billion pipeline. At 2,200-km long and 3-km deep in places, this would be the world’s longest, deepest subsea pipeline and could supply Europe with Israeli and Cypriot gas by the mid-2020s. (Figure 4)

European Climate and Energy Commissioner Miguel Arias Canete described the project as meeting “all relevant requirements” and offering “a valuable contribution to the EU’s strategy to diversify sources, routes and suppliers.”

LNG Exports

Israel could choose to build an export liquefaction plant at either Ashkelon on the Mediterranean coast or at the Red Sea port of Eilat. Alternatively, Israeli natural gas could be piped to a proposed LNG plant at Vasilikos on the south coast of Cyprus. In Israel, with a highly built-up Mediterranean coastal strip, Ashkelon would seem to be the only suitable site as it has sufficient area to accommodate a land-based. two-train or floating LNG facility.

In theory, an LNG export plant at Eilat would allow Israel to access Asian markets. In practice, this would mean competing with other Middle East, Australian and even U.S. supplies. However, directing gas from Israel’s Tamar and Leviathan fields by an undersea pipeline to the proposed LNG plant at Vasilikos would improve not only the viability of Israeli gas exports, but also help develop the Aphrodite gas field in Cyprus waters.

In view of a continuing supply glut and low prices, Jordan is the best immediate prospect for Israeli gas exports, given that long-term supply agreements with power and industrial customers are in place. Egypt offers short-term temporary gas sales, requiring only a reversal of an existing pipeline.

As for pipeline exports reaching Turkey and European markets, political and financial hurdles will need to be overcome and natural gas prices would have to rise considerably before any pipeline scheme is bankable. There is also the question of timescale and relative cost. It could take up to 10 years to construct the proposed subsea pipeline to Europe, whereas a floating liquefaction facility (FLNG) can be set up in a couple months and an onshore export plant could be constructed in about four years.

A FLNG would also cost much less than a pipeline. However, pipelines can deliver large quantities of gas continuously while LNG tankers or virtual pipelines offer market flexibility. The final decisions on markets and routes will be guided by multiple complex political, financial and economic considerations.

Offshore Gas Discoveries Loom Large for Egypt

Major gas discoveries during the 1990s and this decade have enabled a shift toward natural gas power generation at the expense of oil and coal. In 2005, Egypt’s reserves of natural gas were estimated at 66 Tcf, the third-largest in Africa, and probable reserves are estimated at nearly double, at over 120 Tcf.

Nevertheless, rising demand of 7% a year resulting from increased population and industrialization is being met with imports of LNG via two leased floating storage and regasification Units (FSRUs). LNG imports climbed from 2.8 mtpa in 2015 to 6 mtpa in 2016 and may peak at 6.6 mtpa this year after which recent exploration successes will translate into increased production. Forecasts envisage a natural gas deficit developing around 2021 and rising sharply from 2029, (Figure 1).

Egypt’s Western Desert, the Nile Delta and eastern Mediterranean waters have attracted investment from many foreign energy companies including Eni, BP, Anadarko, Dana Gas and Rockhopper. Big discoveries include Shell’s 2016 find of 5 Tcf of natural gas at its Alam El Shawish concession in the Western Desert, with the possibility of more reserves waiting to be recovered.

But, 150 km off the Egyptian coast, lies Eni’s 2015 discovery of the spectacular super-giant 30-Tcf Zohr gas field, which is larger than all the finds in both neighboring and Israeli offshore waters. Eni believes Zohr will start producing at yearend, reaching 2.6 Bcf/d by 2019. There are also new gas finds in the Nile Delta, including BP’s West Nile Delta North Alexander and SDX Energy’s discovery at South Disouq, (Figure 2). Investment by foreign energy companies this year could reach $10 billion, reports Egypt Daily News.

Domestic Production

New finds have allowed Egypt to rank as the Middle East and North Africa’s sixth-largest natural gas producer, with an output of 5 Bcf/d which will be boosted by the coming on-stream of Zohr later this year and the West Nile Delta North Alexander field next year.

Energy consultants Gaffney, Cline & Associates predict peak gas production at 8 Bcf/d in 2019-20 and an ability to maintain production above 6 Bcf/d until 2024. Adding in known, but as yet unsanctioned natural gas developments, could extend this plateau until 2027, (Figure 2).

In parallel with increased supply, the natural gas market is expected to grow by at least 50%, boosted by new gas-fired power plants, improved distribution, increased access to electricity and expansion of industry.

State-owned Egyptian Natural Gas Holding Company (EGAS) distributes gas, produced by foreign companies, to three main market segments: power plants, local distributors and industry.

The country’s 59 power plants consume 56% of all distributed gas with local distributors taking 22% and the remainder shared by industries such as cement-making, and petrochemicals and by households, 1.5 million of which have been connected through the World Bank’s $1.53 billion Natural Gas Connections Project.

Generating capacity is planned to increase by 50% in the next decade, enabled by upgrades to existing plants and construction of 14 new gas-fired power plants along the Nile Valley, including three 4.8-GW capacity gas-fired combined-cycle power plants. These should be fully operational at the end of 2018, providing stable electricity to 11 million people.

Natural gas demand could be further boosted by expansion of the petrochemical industry near Alexandria under the National Plan. The Egyptian Petrochemicals Holding Co. foresees production of propylene, formaldehyde and derivatives reaching $1 billion, says the Egypt Daily News.

Domestic Pipeline Grid

The 7,500-km main transmission grid delivers natural gas from onshore and offshore fields and LNG regasification facilities to major distribution hubs located close to major cities and industrial centers.

The regional distribution pipeline network delivers natural gas from hubs to customers and reached 35,000 km in length in 2016, according to Egyptian energy solutions group TAQA. The entire gas grid of national and regional networks transports 215 MMscf/d. Egypt’s entire pipeline network is believed to be the longest in Africa.

EGAS plans to expand that network. One $105 million project, designed to transport 450 MMcf/d from the Raven gas field to a gas complex in the Western Desert and a cooking gas extraction factory in El Ameriya, could be completed in mid-2019, said EGAS Chairman Karem Mahmoud.

Offshore Pipelines

New gas field developments would be incomplete without associated pipeline construction. For example, the Zohr gas field is being furnished with a 26-inch gas export trunk line, with 14- and 8-inch service trunk lines. This will be alongside EPCI work for the field development in deep water (up to 1,700 meters) of six wells and the installation of the umbilical system. Work started in July 2016 and is scheduled for completion by the end of this year.

BP has awarded Subsea 7 a contract to install over 40 km of rigid pipelines and associated structures for the new Atoll field. The water depths for the installation work range from 100-900 meters. Subsea 7 will be tying these pipelines into the existing Taurt field facilities which are in water depths of 100 meters, and installing 105 km of umbilicals to connect subsea wells on the Atoll field.

Cyprus and Egypt have announced a plan to build a connecting subsea natural gas pipeline to enable export of Cypriot gas to Egypt for domestic consumption and elsewhere, via Egypt’s existing LNG export ports.

Until recently the 1,200-km Arab Gas pipeline exported Egyptian natural gas to Israel, Jordan and Syria. Due to sabotage, exports have virtually ceased. However, EGAS now has plans to reverse the pipeline flow and import gas via Jordan’s LNG terminal at Aqaba.

New gas fields, further investment in exploration and transmission alongside pipe and LNG imports, could combine to reduce the gap between projected demand and supply.

Comments