March 2016, Vol. 243, No. 3

Web Exclusive

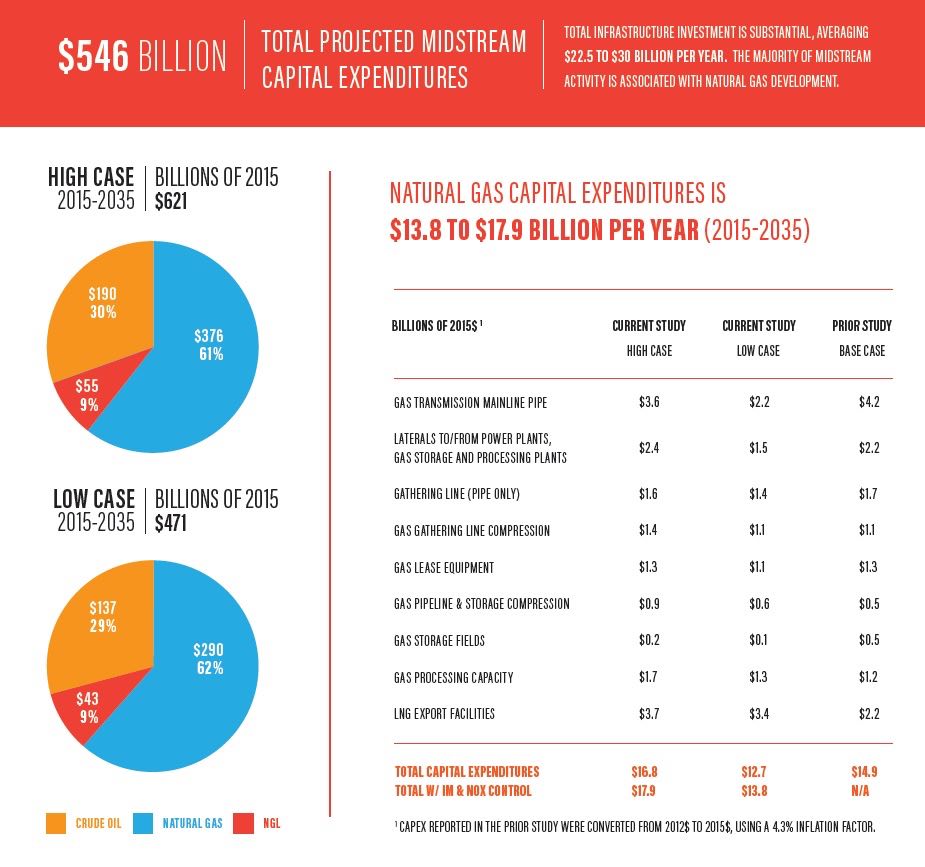

US, Canada to Require $546 Billion in Gas, Oil and NGL Infrastructure Investment

WASHINGTON – The United States and Canada will require annual average midstream natural gas, crude oil and natural gas liquids midstream infrastructure investment of about $26 billion per year, or $546 billion (real 2015$) total over the 21-year period from 2015 to 2035, a new study found.

The report, North American Midstream Infrastructure Through 2035: Leaning into the Headwinds, conducted by ICF International on behalf of the INGAA Foundation, updates a 2014 infrastructure report to reflect the dynamic changes in the natural gas, NGL and crude oil industry in recent years.

“We saw a need to reexamine infrastructure needs in light of significantly lower commodity prices,” said INGAA Foundation President Don Santa. “While E&P activity may dip temporarily because of lower prices, we still will need significant capital investment, particularly in natural gas midstream infrastructure.”

Natural gas infrastructure makes up over 60% of the needed energy infrastructure in the report, with total investments of between $290 billion and $376 billion ($333 billion midpoint) required from 2015-2035. Natural gas infrastructure includes gathering and transmission pipelines, compressors, laterals, gas-lease equipment, processing, gas storage and LNG export facilities.

Meanwhile, between $137 billion and $190 billion of crude oil infrastructure (gathering pipeline, lease equipment, mainline pipeline and pumping, storage laterals and storage tanks) and between $43 billion and $55 billion of new NGL infrastructure (transmission pipelines, pumping, fractionation and NGL export facilities) will be required in the next 20 years.

For the first time, in the report’s 20-plus year history, ICF presents two scenarios: A High Case, which is characterized a plausibly optimistic case for midstream infrastructure development, and a Low Case, a less-optimistic case, in which a slower economic recovery reduces the need for oil and gas and pipeline development. The market growth projected in the two cases is very different. For natural gas, the Low Case projects gas use rising to 110 Bcf/d by 2035, while the High Case sees growth to over 130 Bcf/d. The biggest difference occurs in the power sector, where the Low Case assumes lower electricity demand growth, greater energy efficiency and more significant penetration of non-gas generating resources.

Comments