July 2016, Vol. 243, No. 7

Features

Electric-Gas Buying Trend: Transformational, but with What Implications?

“Now is the right time for this transaction; we see an emergence of technology, consumer behavior, market forces and regulatory changes that over time will change the way customers use energy,”

— Tom Fanning, Southern Co. CEO, August 2015, announcing acquisition of AGL Resources

Since the middle of 2015, the CEOs of major electricity giants such as Duke Energy, Southern Co. and Dominion Resources have all been talking about transformational, strategic and sure-fired growth engines. And that’s just the understated part before they get warmed up. Those engines are in reality natural gas properties, long an anathema to the power side of the energy business, but today the future looks different. The electrics are stocking up on gas buys, particularly with midstream pipes, looming up big time these days.

When Southern Co.’s CEO Tom Fanning talks about the transformation, he gets visibly excited, noting that the need for expanding natural gas infrastructure has been a familiar part of the industry lexicon for some time as an offshoot of the shale revolution that has produced ever-larger production of U.S. gas supplies and elongated periods of unusually low prices. He calls the increase of gas used for electric generation “a prime example” for today’s industry pivot shift. Southern, itself, projected gas consumption last year for its power plants of 1.8 Bcf/d, up 20% over the past three years. Its gas usage has nearly doubled in the last 10 years.

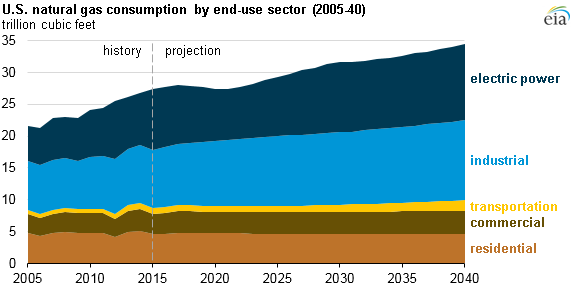

Early in 2016, the U.S. Energy Information Administration (EIA) predicted that natural gas would remain the dominant fuel for power generation all of 2016, the first time that has ever happened, and it is likely to continue in future years. Another factoid from the government’s storehouse is that new infrastructure tied to all the development of the Utica and Marcellus shale plays added over 51 Bcf/d of pipeline capacity during the past five years, and it is expected to add another 49 Bcf/d of capacity in the next five years.

Convergence of electric-gas provides operational diversity on the electric side at a time when there is not much growth opportunity over there, according to Moody’s Investors Service analysts, Jairo Chung and Ryan Wobbrock. The need for growth on the electric side and cheap plentiful gas from the fuel side are what executives like Fanning call the latest perfect storm.

“The convergence provides additional revenue growth and growth in earnings-per-share at a time when electric utilities are finding it hard to grow organically,” said Wobbrock, an assistant vice president who has authored a report on the subject. “An electric utility automatically gets a huge amount of diversity by acquiring a gas utility, diversifying its revenue from 100% electric to 80% electric and 20% gas.”

While not large compared to the majors or mid-majors in the oil world, the deals stacking up amount to multi-billions of dollars – Duke acquiring Piedmont Natural Gas Co. for $4.9 billion in cash; Virginia-based Dominion Resources, Inc. nabbing Utah-based Questar Corp. for $4.4 billion; and Southern Co. buying Atlanta-based AGL Resources for $12 billion in a transaction that ultimately will create a utility infrastructure rate base in excess of $50 billion. Fanning dubbed it “playing offense in supporting America’s future.”

Long an important source of natural gas demand and infrastructure build out, the power sector will be the premier gas consumer in future generations, driven by climate change mitigation, renewable-based power and increasing clean power requirements.

“It certainly is an appealing avenue to lock in lower prices, and lock in rate base growth,” Julien Dumoulin-Smith, UBS Securities’ director of equity research, who thinks regardless of ongoing court challenges, the Obama administration’s move to a clean power plan for the generation sector will persevere in some form. “Gas buys provide some vertical integration and stability in pricing for customers.

“The drivers are pretty consistent across a lot of the deals of late,” Dumoulin-Smith says. “We’re seeing gas acquisitions as a proxy for better earnings growth outlooks. The name of the game in the electric space is distribution, and distribution includes the natural gas sector.”

Distribution’s growing importance is what Dumoulin-Smith calls a key element behind many deals that have been done and those in the works, and it is particularly relevant to the Southeast where future gas infrastructure becomes very big in the face of what is needed, given the region’s historic heavy reliance on coal. The question down the line is to what extent the rise of solar rooftop systems can displace some of that gas-fired power generation market, Dumoulin-Smith notes without pre-judging the outcome.

“That’s a real wildcard because the Southeast up until a few years ago was not thinking about solar in a big way. Now that has changed as states like Georgia get more involved,” he says.

When telling financial analysts about buying Piedmont, Duke CEO Lynn Good emphasized that the deal will give Duke a serious presence in natural gas infrastructure, along with bringing under the fold a company that has supplied gas to Duke’s power plants for many years. She emphasized the plan to invest heavily in new gas infrastructure, and promised at the time of the deal’s closing late in 2016 that more specifics on those plans will be outlined for stakeholders. She cited growth benefits to Charlotte, NC-based Piedmont and strategic advantages to similarly headquartered Duke.

In mid-March this infrastructure hunger expressed itself in a rare bipartisan way when 30 Virginia state lawmakers collectively voiced their support for the proposed Atlantic Coast Pipeline (ACP), calling the 550-mile, 1.5 Bcf/d large-diameter natural gas transmission pipeline a major step in promoting their state’s economic and environmental health. ACP is a joint venture between Dominion, Duke, Piedmont, and AGL. The 42-inch pipeline would begin in Harrison County, WV and travel through Virginia before forking into a 36-inch line running through North Carolina and a shorter 20-inch line running to the Hampton Roads area.

With its acquisition of Piedmont, Duke looks to triple the scale of its natural gas operations, according to CEO Good, noting these added assets include liquefied natural gas (LNG) peaking storage facilities and underground gas storage. There are “compelling benefits” to this prospective marriage, said Good, ticking off several of them, not the least of which is furnishing Duke’s electric juggernaut with a “strong natural gas infrastructure platform.”

“Abundant, low-cost natural gas increasingly will become part of the nation’s energy mix as the shift from coal to gas continues,” she told analysts last year in announcing the acquisition plans. She also mentioned the historic irony that Piedmont was originally formed in 1951 by a spinoff of Duke’s gas assets. Strategically, the expanded Duke will be eyeing business out of both the Utica and Marcellus shale plays in Ohio and Pennsylvania.

The low-price commodity environment helps to subsidize the spending needs of an electric acquiring a gas utility. Given 2015’s low commodity price environment, large-cap utilities moved in to buy mid-cap and small-cap gas utilities.

“The idea is acquire a [gas] company, spend a lot on the infrastructure and the ratepayers are not going to feel quite the impact because it is being subsidized by very cheap natural gas prices,” said Shahariar (Shar) Pourreza, director, North American power/utilities for Guggenheim Partners LLC in New York City. “In this country, infrastructure needs to be increased, and utilities are spending a whopping amount of money on infrastructure needs.”

An example this year comes from one utility in New Jersey, Public Service Enterprise Group (PSEG), whose executives told investors of plans for $16 billion in capital investments in their electric and gas utilities and power generation fleet over the next five years.

In the Dominion-Questar combination, Dominion CEO Tom Farrell called Utah one of the fastest growing states and Questar one of the nation’s fastest growing utilities, noting commitments in play for over $1 billion in new infrastructure. This fits well with Dominion’s master limited partnership (MLP) Dominion Midstream Partners.

“While Dominion’s transmission system is known as a hub of the Atlantic, the Questar system is the hub of the Rockies,” Farrell told analysts when the deal was struck in February, noting that Utah and surrounding states will likely rely more in the future on gas-fired generation.

“We see a lot of value in hub systems,” he says. “Almost every pipeline going into the Northeast hits our pipeline system somewhere. Questar’s pipeline provides that same service to the Northwest and a large chunk of California. Almost a third of the gas in the western United States goes through this pipeline system, so we are very familiar with hubs.”

As with all of the recent electric-gas marriages, Questar brings Dominion $4.2 billion in assets, including 27,500 miles of gas distribution pipelines, 3,400 miles of transmission pipe, and 56 Bcf of working gas storage, along with a regional cost-of-service gas supply program for its utility customers. “We were principally attracted to Questar’s assets largely by the pipeline,” Farrell says, adding that Utah is often ranked as the leading state in which to do business.” The MLP assets were the game-changer for Dominion, though.

“This is a pipeline that is going to have a lot of growth opportunities in a well-run, active-in-the-community, safety-conscious company at the utility,” said Farrell, noting the acquisition takes care of added MLP growth for several years at Dominion Midstream. “The MLP now has a long runway of contracted, long-term gas infrastructure assets available to it with zero commodity price risk. There is a lot of distress in the midstream area these days, and this is a company that is not stressed.”

Moody’s Wobbrock sees some “fascinating” aspects to the Dominion-Questar combination in which Dominion is not only capturing diversity by getting the natural gas distribution utility in Utah, but it also adds valuable assets to its midstream MLP. “Part of the strategic rationale for Dominion is to extract Questar Pipeline Co. and put it into Dominion Midstream,” Wobbrock says. “That’s a unique aspect of growth for Dominion.”

His colleague at Moody’s, Chung’s latest analytical work is looking at how companies are financing the transactions and credit implications. From the end of 2013 until the end of last year, 11 of these transactions took place, including two involving Canadian companies. Only two of the 11 were done entirely with equity. “The rest were a mix of all debt, debt and equity, and some hybrid securities,” Chung says. Example: Nova Scotia, Canada-based Emera Inc. buying TECO Energy Corp. (gas/electric), serving U.S. utility customers in Florida and New Mexico in the U.S., and Canada-based Fortis Inc. buying Tucson, AZ-based UNS Energy.

“Another trend we see is that given the environmental shift away from coal-fired power, the electric utilities are looking to convert their coal assets to gas-fired power,” she says. “So for Southern and Duke having a direct access to low-cost natural gas assets complements their power assets. They are looking to utilize more gas and their strategic thinking is that they might as well own a piece of that as well.”

Guggenheim’s Pourreza is of the mind that any kind of energy source has environmental concerns, so even if natural gas has those concerns, it emits only half the CO-2 of a coal plant. “The more you diversify away from coal, you’re cutting CO-2 in half. Environmental considerations are driving this whole shutdown of U.S. coal assets.”

The trend carries profound implications for future capital investments, according to Pourreza. He is unequivocal in saying the gas asset buying spree will definitely boost cap-ex spending. “There are huge amounts of spending that these gas utilities will have. In fact, gas utilities grow faster than electric utilities and they always have, and they have better rate-recovery mechanisms than the electrics.”

Cap-ex and financials both will be impacted, he says. “The cheap money that is out there has helped the utilities; financing for transactions is easier to obtain.”

What are the hidden stumbling blocks for all this good financial news? He doesn’t think growth of the utilities will be impacted by economic twists and turns. “Utilities have been decoupled from GDP and the [macro] economy years ago. Utilities don’t grow by selling more power anymore; they grow by building more infrastructure and earning a return on that investment.”

In the energy part of Warren Buffett’s Berkshire Hathaway conglomerate, BH Energy already has acquired $82 billion in assets that possess a good regional and functional mix of electric/gas utilities and pipelines in which efficiency is a hallmark. In his 2016, 25,000-word letter to shareholders, Buffett said his trademark efficiency is paying off big time in the energy sector and he expects it to be even more important in the years ahead. His natural gas pipeline revenues (Northern Natural Gas and Kern River companies) dropped slightly in 2015 to just over$1 billion, but profits were still higher for the year ($401 million) than the previous year ($379 million).

The attractiveness of the gas assets comes in an environment that is marked by what Southern’s CEO Fanning calls sustained low prices, a growing U.S. economy, increased LNG export facilities and potential impact from environmental regulations. However, he notes even with a projected century’s worth of cheap U.S. gas supplies, “sufficient infrastructure does not currently exist in all regions.” That’s what drew Southern to AGL; Duke to Piedmont, etc., etc.

The gas additions are touted as not just a form of diversification and bigger profits. They are a platform for growth and a way to negotiate where climate change-driven interest in efficiency and renewable energy sources will loom ever-larger regardless of which way the political winds eventually blow.

(Richard Nemec is Los Angeles-based contributing correspondent for P&GJ. He can be reached at: rnemec@ca.rr.com.)

Comments