July 2014, Vol. 241, No. 7

Features

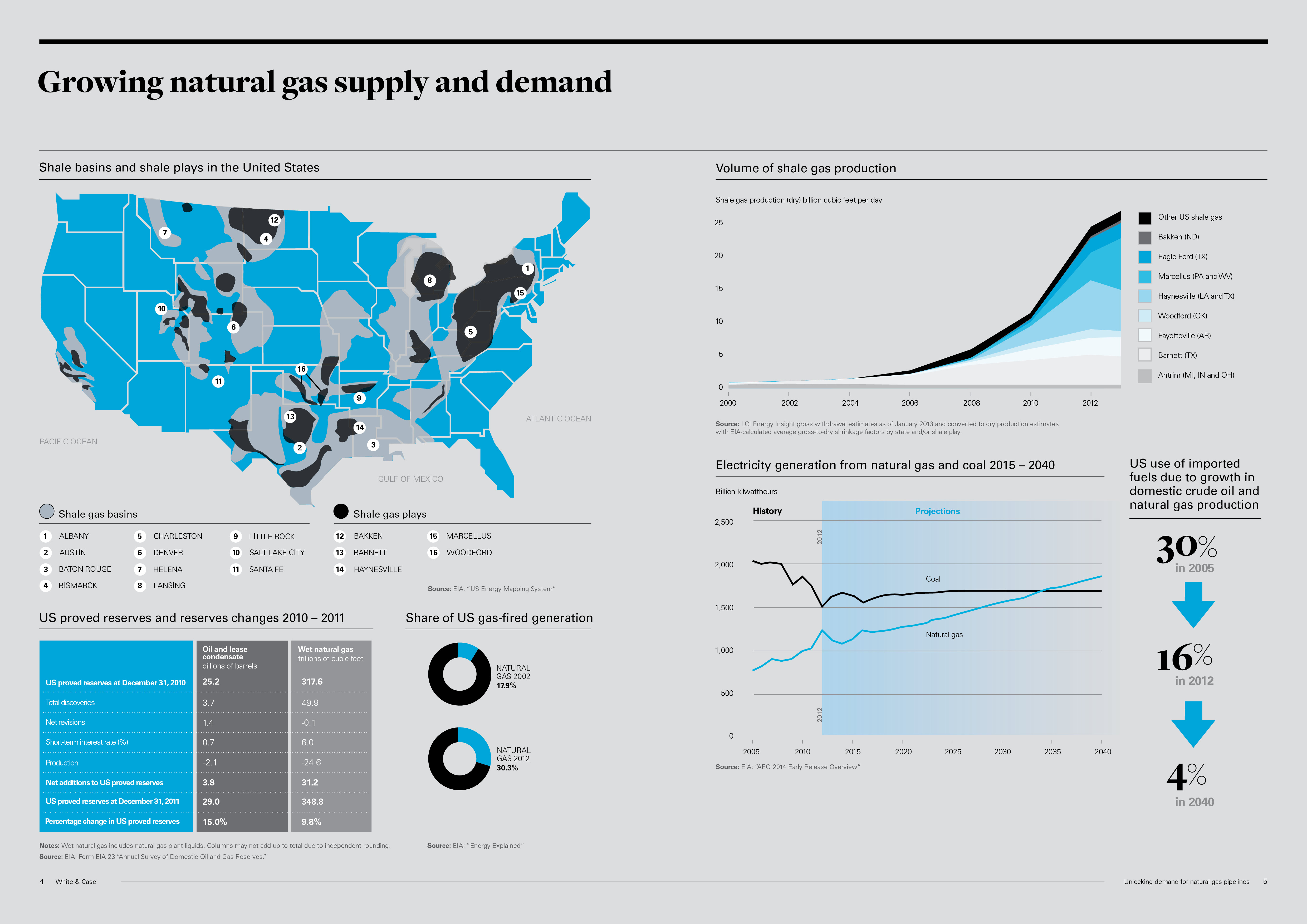

Investment Incentives Must Grow With Capacity Demand

Despite vast U.S. shale gas resources and technological advances making recovery economically feasible, an absence of incentives supporting the usual investment model in which a company builds, owns and operates new pipelines – supported by long-term contracts for capacity – is hampering construction.

This is according to an analysis from the law firm of White & Case which added that the lack of coordination between the gas and power sectors has hampered demand for long-term capacity among gas-fired electric generators – a major source of growth.

“The United States has a golden opportunity to become a powerhouse in global energy markets, but that path is far from assured without a major expansion of the long-distance pipeline network,” said Daniel Hagan, head of the Energy Markets and Regulatory Practice division at law firm White & Case.

Interstate Natural Gas Association of America (INGAA) Foundation data indicates that it will take about $641 billion in investments in the United States and Canada to build infrastructure for transporting dry natural gas, crude oil and natural gas liquids (NGLs) to meet demand.

According to Hagan, who along with Jane Rueger is co-author of “Unlocking Demand for Natural Gas Pipelines,” producers are reluctant to commit to long-term contracts because gas prices are too low and volatile, while local distribution companies (LDCs) and other major purchasers are generally only interested in expanding pipelines when demand from core customers is on the rise.

At the same time, power companies that otherwise would be leaning toward building gas-fired plants are hesitant to move forward without the guarantee of infrastructure to deliver the needed supply.

Lack Of Coordination

That even the market day is structured differently for gas and power companies goes a long way toward underscoring the unwillingness of power generators to commit to firm long-term contracts for natural gas, says the White & Case analysis.

The “gas day” starts at 9 a.m. central time and ends at 9 a.m. the next day, with scheduling for transportation done in regimented nomination cycles by daily quantities to be delivered during the gas day. The “electric power day” takes place from midnight to midnight with scheduling varied, depending on the region. Most regional transportation organizations operate a day ahead with generated units committed to run the next day.

As more electricity generated in the United States is coming from natural gas, however, the Federal Energy Regulatory Commission (FERC) and industry participants are exploring possible solutions to issues related to the coordination between the two markets. Additionally, stakeholders have been pursuing regional initiatives to encourage coordination, White & Case said.

In January, for example, the New England States Committee on Electricity (NESCOE), representing the electricity interests of Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island and Vermont, proposed changes that would address the region’s coordination issues.

Among the changes, it was recommended that the region’s grid operator, ISO New England, develop tariff provisions that enable the recovery of pipeline investment costs with costs being passed on to electricity customers.

“Electric/gas coordination is a real issue, and it’s at its most significant with extreme weather events, and is not limited to one geographic area,” Hagan said. “I think that we will see some sort of policy decisions being made by FERC. These are not easy things to push through, and FERC has been looking for five years now, which is an indication of how terribly complicated the issue is.”

Parity Legislation

Pipeline investment and financing must be made more attractive, according to the report, and extending the benefits of master limited partnerships (MLPs) to infrastructure and renewable energy firms could make it possible to add revenue streams from pipeline systems.

The MLP Parity Act is before Congress and would offer pipeline operators tax incentives to use their knowledge of siting and permitting to install renewable capacity, such as solar panels, to reduce costs. The electricity generated from solar panels would offset the cost of fuel for compressors.

Regarding this potential legislative inroad, however, Hagan said he is not overly optimistic in the short term.

“I’m afraid there hasn’t been much noise at all [about a vote], even though it has received broad-based support,” he told Pipeline & Gas Journal. “Perhaps the benefits that would be accrued are broader than people realize.”

MLPs have already been an effective means of bringing unconventional oil and gas resources online quickly.

Additionally, the report points to tapping into LNG as a significant step toward boosting investment in pipeline infrastructure.

“It is clear that world events are unfolding quicker than the Department of Energy’s (DOE) authorization process,” the report said of the industry’s ability to export LNG beyond the limits already in place.

However, a series of new bills in Congress, which followed events in Crimea and Ukraine, would bolster LNG exports to allies. Also, the Trans-Pacific Partnership Agreement (TPP), if agreed to by the United States and Japan, would cause the DOE to automatically approve LNG shipments to Japan.

The report, however, cautioned that the United States must act swiftly before LNG exporting countries, such as Canada, have LNG-exporting infrastructure in place to meet global demand.

The DOE concluded exporting about 12 Bcf/d would provide net benefits to the U.S. economy and has issued seven permits so far that would enable that level of exportation to countries that don’t have free trade agreements with the United States.

Industry-Regulator Partnership

Among the biggest boosts to pipeline expansion in the United States, according to Hagan and Rueger, would be the advent of a national energy strategy, which moved into its early stages in January when President Obama ordered a Quadrennial Energy Review.

Under that mandate an interagency task force will develop an integrated energy strategy that initially focuses on the nation’s infrastructure needs for transmission, storage and distribution of oil, gas and electricity. The task force will assess legislation and recommend necessary steps to promote infrastructure investment.

“Once a regulator can understand the collective stakeholders’ interest, which is broader than just the industry, then he can go about the business of regulating,” Hagan said.

The energy review will examine current pipeline economics and conduct a wide-ranging search for new solutions to fund pipelines. It will also compare the benefits and drawbacks of shipping large volumes of oil by rail or transporting it by pipeline.

“The real trick is being able to adopt policies that are flexible enough to address the problem and make changes in the market design in ways that are able to address problems in a more timely fashion,” Hagan said.

For near-term investment dollars, pipeline companies must compete with rail and trucking companies which have the advantage of flexibility and adaptable, much faster delivery points.

However, rail and trucking can only transport NGLs and crude oil economically – not dry natural gas – and require more capital, while posing more significant safety risks than pipelines. Recent infrastructure investments have focused on NGL and crude oil shipping due to the comparatively low price of gas. Many analysts, however, feel this trend will reverse itself within the next five years.

“Innovative approaches to energy infrastructure must be developed by industry participants and regulators cooperating together to achieve common goals,” the White & Case report said. “Only through fresh ideas and cooperation can the United States succeed in developing the energy infrastructure necessary to unlock demand for shale gas.”

The Quadrennial Energy Review task force, which will issue its first report next January, will also consider national security and environmental safeguards; feedback will come from consumers, local governments, the private sector and academia.

Comments