July 2009 Vol. 236 No. 7

Features

Wake Up Pickens Natural Gas May Not Be Panacea

T. Boone Pickens’ energy plan for the U.S. has fatal flaws that challenge its real potential and the notion that natural gas is the panacea fuel for solving all the nation’s energy and environmental problems. Do not count on it as the long-term policy solution for energy independence or the fuel to depend on for your investment decisions. He may make another fortune but it is not necessarily in the best interests of the country, our economy, or our standard of living.

The Pickens Energy Plan

T. Boone Pickens has always liked to play the role of the bootstrap visionary: a man of big and audacious ideas, ideas that are so big and so audacious that they can sweep aside the myriad pragmatic objections such notions raise.

But as he learned in his elusive quest for Gulf Oil (and many other oil and gas companies) in the 1980s, conceptual purity and singular focus are usually not enough to overcome the messy details that ensnare such visions. The Pickens Plan for mass conversion of the U.S. transportation fleet to natural gas vehicles (NGVs) and for wind farms the size of New Jersey shares this trait.

The heart of the Pickens Plan is a call to replace all natural gas-fired power generation with wind power and to take the natural gas thus saved and put it into all new government vehicles, all fleet vehicles, all long-haul transport vehicles, etc., within a decade. Pickens has specified repeatedly that this must take place over the next 10 years or something very bad will happen. Therefore, the federal government must get on the ball and make it happen, quickly. Remember, this directive is coming from a man with large natural gas holdings and a project in progress to build 2,000 wind mills in the Texas Panhandle.

When this plan was first pitched in the spring and summer of 2008, it had several things going for it. Gasoline and diesel fuel prices were skyrocketing (Pickens helpfully projected $300/Bbl as a likely equilibrium price in television interviews), the global economy was unraveling, and the campaign rhetoric on global warming and energy independence was escalating in step with the oil-driven U.S. trade imbalance. The public did not know what to make of any of this, but the public was scared and angry.

The Pickens Plan, on the surface, appeared to address all of these frightening issues with a simple quid pro quo: wind mills for power, natural gas for transportation. Result: crude oil imports cut in half, carbon emissions reduced, problems solved. An unspecified amount of government money would lubricate the process in an unspecified manner. You could keep the whole plan in your head; describe it in a sound bite. The environmental lobby could live with the message and cable news reporters loved the oft-trumpeted irony of the messenger, a “legendary Texas oil man,” pushing wind mills. All that was needed was a little common sense and some willpower.

Here are some pitfalls in the Pickens Plan. First quibble: for all the (several) pie charts and graphs that accompanied Pickens’ advocacy campaign, the Pickens Plan is not a plan. Real plans must identify an implementation process, not just a set of goals with a target completion date. For example, there are approximately 450,000 MW of installed gas-fired generating capacity in the U.S. providing about 20-22% of current electricity demand – roughly the availability factor that transmission system operators typically assign to wind resources. Presumably, then, we would need about 450,000 MW of installed wind capacity to replace the gas-fired fleet. As of year-end 2008, after the construction of a record annual 8,300 MW, installed wind power capacity stood at 25,170 MW, or about 3% of the U.S. installed capacity. This raises a few initial questions:

- How do we compel the retirement of 45,000 MW of gas-fired generating capacity each year for the next decade?

- Do the owners of that capacity receive any compensation for their loss? From whom?

- How do we compel the efficient financing and construction of 45,000 MW of wind turbines each year for the next decade, coming off a record year of 8,300 MW?

- How do we integrate the two processes seamlessly, such that massive and prolonged service interruptions do not become the norm?

But these power sector questions are paralleled by equally challenging questions on natural gas supply. One premise of the Pickens Plan is a direct swap of 18-20 Bcf/d of gas demand for power generation for an equivalent amount of transportation fuel. But note that interim carbon reduction targets, if enacted into law, would be most efficiently achieved by supplanting coal-fired generation with gas-fired generation for a 50% net reduction in emissions. Pace power market forecasts foresee a growth in gas-fired generation over the next two decades as substitute technologies are deployed for baseload generating capacity.

Further, the greater our reliance on wind power to meet baseload power demand, the greater will be the need for redundant gas-fired power generation, the best available technology to backstop wind power (the correlation between electricity demand and prevailing wind speed being quite low). A wind availability factor of, say, 25% at rated capacity, implies the need for sufficient gas-fired capacity to cover as much as 75% of installed wind capacity during periods of peak demand. Conclusion: the envisioned offset of power generation demand for transportation fuel demand is illusory. Any program to convert a third or more of the nation’s transportation fuel demand to natural gas would require a commensurate increase in natural gas supply for at least a decade beyond the stipulated completion date for implementation of the Pickens Plan.

Where does the additional 20 Bcf/d we would need come from? Leaving aside for the moment the challenges and costs associated with converting a third of the U.S. surface transportation fleet to natural gas and installing the necessary infrastructure to fuel this new NGV fleet, where would we get the incremental fuel supply for all this new demand – eventually around 20 Bcf/d?

Looking back to 2007, U.S. domestic production provided about 80% of demand, supplemented by Canadian pipeline imports amounting to some 17% of demand with the balance covered by imported LNG from places like Algeria, Nigeria, Trinidad and Qatar. Canadian gas production has been declining for years despite the recent price incentives. This leaves us with imported LNG and domestic production. If we are to reduce energy imports, where would we turn domestically for that incremental 20 Bcf/d on top of current demand of 64 Bcf/d?

Pickens’ answer appears to be the large accumulations of natural gas in geological deposits known as shales. Recent and cumulative advances in drilling and development technologies and practices have demonstrated that these “unconventional” domestic resources can be commercially developed and produced at an average cost of roughly $6/MMBtu. Despite the apparent magnitude of domestic shale gas resources, however, recovering those resources is not as simple as Pickens would allow us to believe.

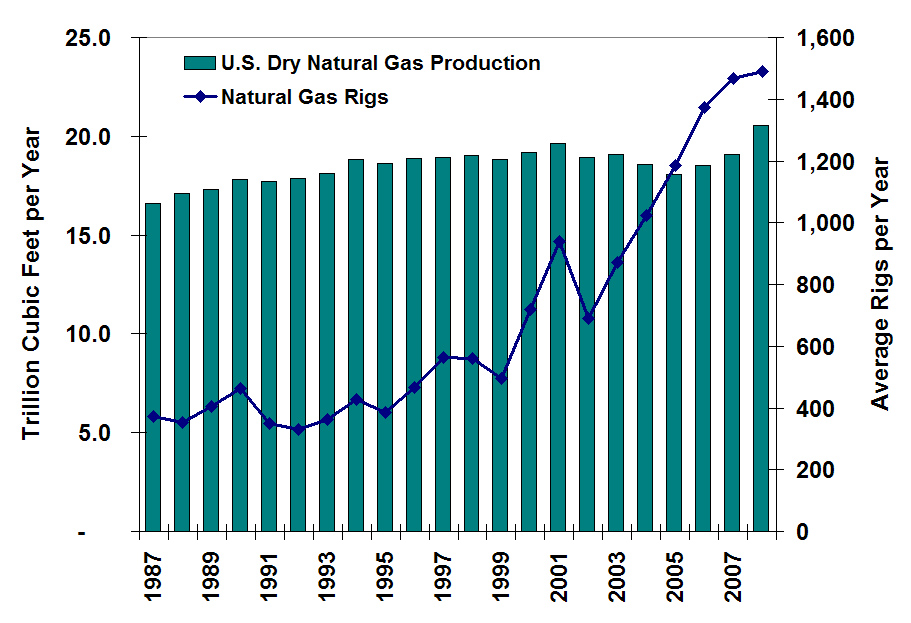

The “shale boom” of recent years pulled every available and shale-capable horizontal drilling rig into service before prices crashed in late 2008. Yet, despite more than doubling the number of rigs searching for natural gas, from an average of 691 in 2002 to 1879 in 2008 (including a weekly peak rate of 650 horizontal drilling rigs needed for commercial shale gas development), domestic production managed to climb only 4.3 Bcf/d over that period.

What would it take to increase current levels by 20 Bcf/d within 10 years? First, it would take a sustained price increase of at least 75% above current levels to convince developers and their bankers that it was safe to expand the shale development effort. Then it would take the construction of 1,200-1,500 new horizontal drilling rigs over the next five years at a cost of $12-22.5 billion.

Using Pace’s shale development model, drilling activity would need to double from today’s level to return to the recent peak hit in September 2008 and then double again over that same five-year period, assuming the new rigs and the necessary capital became available. The domestic oilfield services industry would need to double in size to support the drilling activity, which itself would require thousands of new skilled personnel to operate the equipment and manage the process.

It would take a large amount of good luck as production rates from identified “sweet spots” in the shale formations proved to be reproducible over large geographic areas underlain by shales of highly variable quality and thickness. It would take the construction of gathering and transmission pipeline systems to get the new production, much of it located in relatively remote areas, into the interstate pipeline system. It would take the aforementioned development of natural gas fueling infrastructure and the conversion or replacement of millions of existing vehicles to create the market to support the prices to justify all the capital investment. In short, it would take something just shy of a miracle.

Cheap And Easy Gas Is Not A Quick Fix

Pickens likes to say that “the simple truth is that cheap and easy oil is gone.” We agree, but the same can be said of domestic natural gas resources. The sequence of events listed above is unlikely to occur, given the number and magnitude of financial, geological and logistical barriers to be simultaneously overcome. At best, we might achieve half the goal if we started today (which we will not). If the transportation fleet conversions proceed according to plan, we will have nowhere to turn but increasing LNG imports. Granted, we still would have reduced our net energy imports, but at what cost? And given the “transitional” nature of the Pickens Plan, we would no sooner have created this new transportation fuel supply industry when it would be time to begin creating the next iteration of the Pickens Plan.

Pickens just has it wrong. Replacing our primary transportation fuels, gasoline and diesel, with natural gas will not provide us with a sustainable path to energy independence; quite the contrary, it would simply replace one form of dependency with another at great cost.

This is not to say that there is no role for NGVs in the U.S. transportation fleet or wind mills in our power generation mix. There is. This is not to say that North America’s shale gas endowment and our technological prowess to extract it is not considerable. It is. But the chief beneficiaries of the Pickens Plan would not be the U.S. economy, our national security or the standard of living of our citizens. The chief beneficiaries of the Pickens Plan would be owners of wind mills and natural gas reserves. Know anyone who fits that description?

Authors

Greg Ballheim, Mark Eisenhower and Bob Linden are with Pace Global Energy Services. This article is from the firm’s MarketLink. 703-818-9100, info@paceglobal.com, www.paceglobal.com.

Comments