May 2017, Vol. 244, No. 5

Features

The Gained Decade: North American Gas Distribution

What a difference a decade makes. In 2007, the Canadian and U.S. housing markets were booming, distribution utilities were focused on new construction, hydraulic fracking was hardly in our vocabulary, natural gas was $7 and oil was $55. The possibilities of financial collapse, economic turmoil and high unemployment seemed remote.

Yet the cracks were visible. In the period 2008-10, the global slowdown punished everyone … except gas distribution utilities.

Today, we have anemic economic growth, slowly recovering housing markets, hydraulic fracking is the norm, distribution utilities are asset-replacement- focused, natural gas is $3 and oil, which peaked at $120 and fell to $30, has now recovered to $50. In the next decade, we wonder, what it will hold … another wave of positive change for LDCs!

Spending Drivers

The surprising elections of Donald Trump and Justin Trudeau – the second-youngest prime minister in Canadian history – is creating optimism. In the U.S., small-business and consumer-confidence ratings are at 17-year highs. Prospects are good across North America and this next decade will be one of the best the industry has enjoyed.

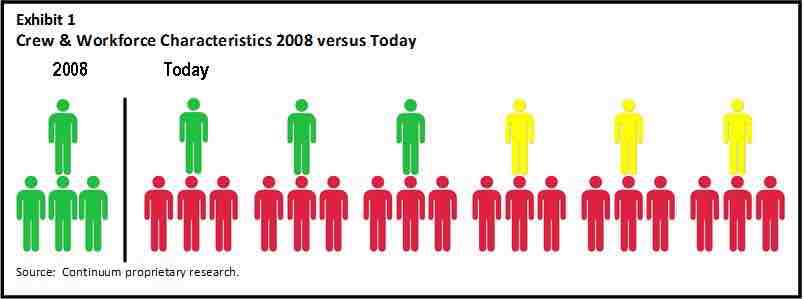

What will drive or stop LDC system construction to another decade of uninterrupted growth? First, we must understand that there are many challenges that can derail this spending forecast, the most controllable of which is workforce availability.

Before discussing drivers, we must first understand that the distribution infrastructure spending growth since 2005 is unprecedented. The traditional utility ratemaking process creates peaks and valleys in capital spending.

The advent and implementation of performance-driven and accelerated recovery mechanism now deployed across the U.S. and Canada have allowed this spending growth to continue and falling natural gas prices have made this increase in spending invisible to many ratepayers. That being said, the drivers of spending in the next decade will include:

- Regulated-driven asset replacement funded through accelerated recovery (Exhibit 1a).

- Low-priced natural gas increasing consumption (Exhibit 1b).

- Return of housing starts to healthy levels (Exhibit 1c).

Canada Distribution

Canada weathered the 2008-10 housing market collapse better than the U.S. due to more rigorous mortgage market controls. However, the 2014-15 oil price collapse was too much to bear, and Canada entered a short recession in 2015 that the country exited in early 2016, but with economic growth well below 2% annualized.

Gas distribution capital spending was historically less than $1 billion per year until 2007 when accelerated cast-iron and bare steel replacement increased across Canada. These programs doubled spending to about $2 billion annually. Going forward, this underlying spend level will remain while methane capture, asset replacement and multi-family/single-family housing growth continues.

Workforce and supervision availability in Canada will remain a challenge, yet liberal immigration policies and effective union and non-union workforce training should help match the workforce need with spending levels.

U.S. Distribution

The U.S. faces a larger challenge in workforce and supervision availability. The continued ramp-up in spending on asset replacement, more intense integrity requirements and housing growth have stretched the workforce to a breaking point and beyond in some markets.

The early asset replacement adopter LDCs have just now reached their spending peaks. Recent asset replacement adopters are a year or two into their accelerated programs and will not hit peak spending until 2020 or later. Late adopters and wholesale vintage plastic replacement is still in our future and will continue to drive spending.

There will be at least one trial first. The general economy has expanded since 2010, and we are approaching the eighth year of this expansion in which the typical business cycle runs five to seven years. All cycles end with a recession, the only question is when. We are currently forecasting a short and shallow recession in late 2018 that will dampen 2019 growth but not stop it.

The combination of energy policy, infrastructure rebuild and small business/consumer confidence will dampen the impact of the economic slowdown. Beyond 2020, the distribution market will continue growing, albeit more slowly, and we remain very bullish over the next 15-20 years of opportunities in the distribution space.

The Next Decade

The next decade is full of promise. Looking forward, we see shifts in the nature of the work that is occurring from broad accelerated asset replacements to more general modernization and integrity-related programs, but no shift in total spending.

This market dynamic will require contractors to take a hard look at their service offerings, better understand where their customers are headed and then decide if they want to follow the spend patterns of their customers or potentially search for new customers with whom their current capabilities fit.

LDCs and contractors jointly face three great challenges: regulation, environmental protest and the big question of “Who will do the work?” Among these, the latter challenge concerning workforce availability is the most controllable. (See “Who Will Do the Work? – Ohio Pilot”).

Building a workforce to complete 15-20 years of potential work is perhaps the largest challenge, and we are aware of a substantial effort led by the Underground Construction Workforce Alliance (UCWA), an industry collaboration kicked off by the Distribution Contractors Association (DCA).

This group is building local resources where the shortages exist and have set up a pilot effort in central Ohio to touch the gathering market of the Utica Shale, and the distribution territories of Dominion, Duke Energy, NiSource and Vectren. We encourage you to sink your teeth into the LDC market and join your peers in working to address the common challenge of workforce availability.

Authors: Mark Bridgers and Dan Campbell are consultants with Continuum Capital, which provides management consulting, training, and investment banking services to the worldwide energy, utility and infrastructure construction industry. They can be reached at (919) 345-0403 or MBridgers@ContinuumCapital.net.

Comments