EIA: Annual Energy Outlook Through 2040

The latest Annual Energy Outlook 2015 (AEO2015) prepared by the federal Energy Information Administration (EIA) presents long-term annual projections of energy supply, demand and prices through 2040. This analysis focuses on six scenarios: a reference case, low and high economic growth cases, low and high oil price cases, and the high oil and gas resource case.

The table gives the case descriptions used in AEO2015, along with a brief explanation of the major assumptions underlying the projection. Regional results and other details of the projections are available at: www.eia.gov/forecasts/aeo/tables_ref.cfm#supplement.

This article focuses primarily on the sections of the report referencing crude oil, petroleum and other liquids and natural gas.

Energy Prices

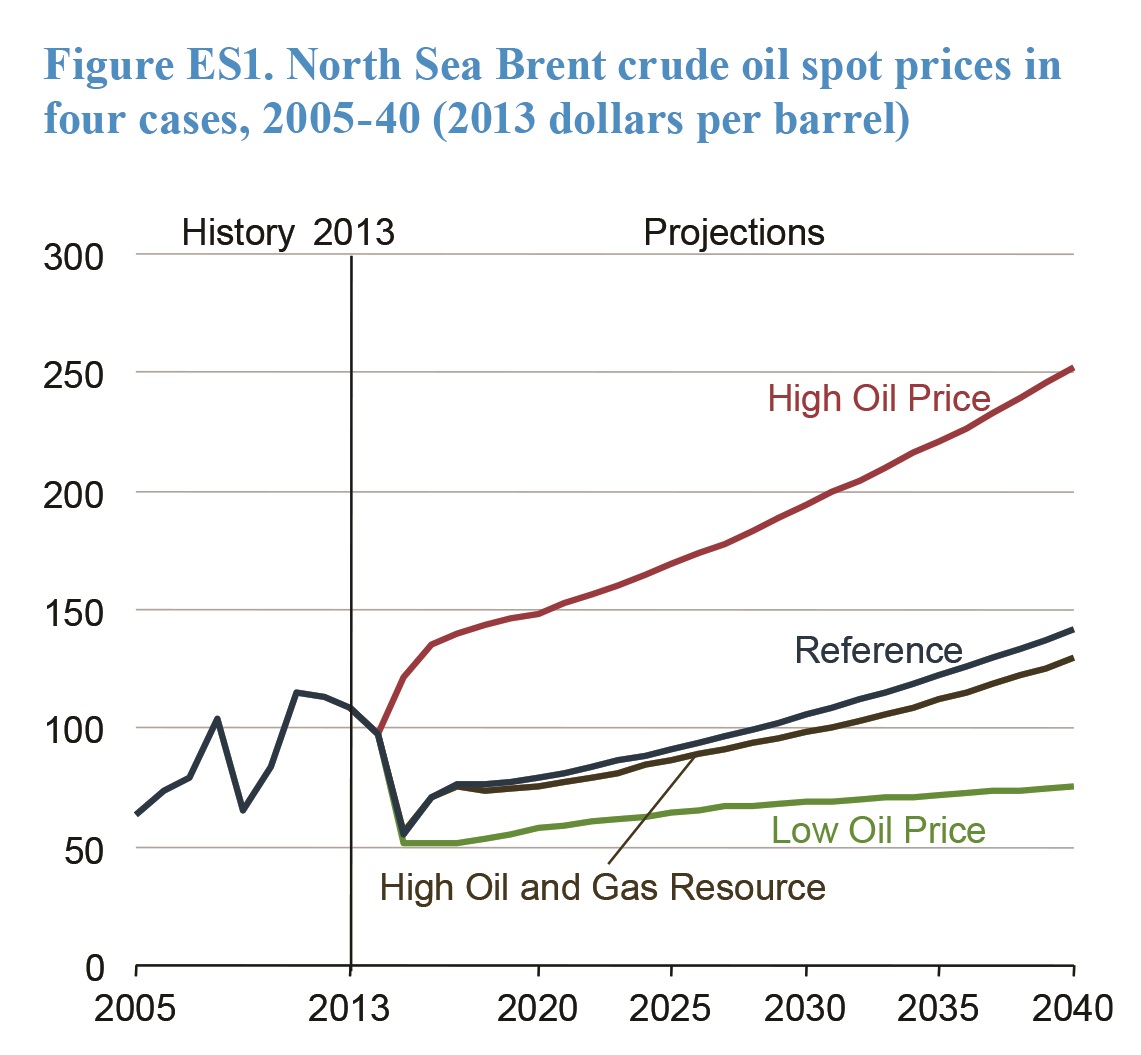

In the AEO2015 reference case, the Brent spot price for crude oil (in 2013 dollars) falls from $109/bbl in 2013 to $56/bbl in 2015 and then increases to $76/bbl in 2018. After 2018, the price increases, reaching $141/bbl in 2040 ($229/bbl in nominal dollars), as growing demand leads to the development of more costly resources (Fig. ES1). In the AEO2014 reference case, the projected Brent price in 2040 was $144/bbl (2013 dollars).

The report noted there is significant price variation in the alternative cases using different assumptions. In the low oil price case, Brent drops to $52/bbl in 2015, 7% lower than in the reference case, and reaches $76/bbl in 2040, 47% lower than in the reference case, largely as a result of lower non-OECD demand and higher upstream investments by OPEC.

In the high oil price case, Brent increases to $122/bbl in 2015 and to $252/bbl in 2040, largely in response to significantly lower OPEC production and higher non-OECD demand. In the high oil and gas resource case, assumptions about overseas demand and supply decisions don’t vary from those in the reference case, but U.S. crude oil production growth is significantly greater, resulting in lower U.S. net imports of crude oil, and causing the Brent spot price to average $129/bbl in 2040, which is 8% lower than in the reference case.

The EIA projects energy imports and exports to come into balance in the reference case, starting in 2028. In the high oil price and high oil and gas resource cases, with higher crude oil and dry natural gas production and lower imports, the U.S. becomes a net exporter of energy in 2019. In contrast, in the low oil price case, the nation remains a net energy importer through 2040 (Fig. ES3). Economic growth assumptions also affect the U.S. energy trade balance.

In the low economic growth case, energy imports are lower than in the reference case, and the U.S. becomes a net energy exporter in 2022. In the high economic growth case, the nation remains a net energy importer through 2040.

The share of U.S. energy production from crude oil and lease condensate is shown to rise from 19% in 2013 to 25% in 2040 in the high oil and gas resource case, as compared with no change in the reference case.

Dry natural gas production remains the largest contributor to total U.S. energy production through 2040 in all the AEO2015 cases, with a higher share in the high oil and gas resource case (38%) than in the reference case (34%) and all other cases. In 2013, dry natural gas accounted for 30% of total U.S. energy production.

On natural gas prices, the report finds future prices will be influenced by a number of factors going forward, including oil price, resource availability and natural gas demand.

In the reference case, the Henry Hub natural gas spot price (in 2013 dollars) rises from $3.69/MMBtu in 2014 to $4.88 MMBtu in 2020 and to $7.85 MMBtu in 2040.

In the high oil price case, spot price remains close to the reference case price through 2020. However, higher overseas demand for U.S. LNG exports raises the average price to $10.62 MMBtu in 2040, which is 35% above the reference case price.

The EIA projects the U.S. transitioning from being a modest net importer of natural gas to a net exporter by 2017, predicting export growth continuing after 2017, with net exports in 2040 ranging from 3 Tcf in the low oil price scenario to 13.1 Tcf in the high oil and gas resource case.

In the reference case, LNG exports reach 3.4 Tcf in 2030 and remain at that level through 2040 when they account for 46% of total U.S. natural gas exports. The growth in LNG exports is supported by differences between international and domestic natural gas prices. LNG supplied to international markets is primarily priced on the basis of world oil prices, among other factors.

This results in significantly higher prices for global LNG than for domestic natural gas supply, particularly in the near term. The relationship between the price of international natural gas supplies and world oil prices is assumed to weaken later in the projection period, in part because of growth in LNG export capacity.

As U.S. natural gas prices are determined primarily by the availability and cost of domestic natural gas resources, in the high oil price case, with higher world oil prices resulting in higher international natural gas prices, LNG exports climb to 8.1 Tcf in 2033 and account for 73% of total U.S. natural gas exports in 2040.

In the high oil and gas resource case, abundant dry natural gas production keeps domestic natural gas prices lower than international prices, supporting the growth of LNG exports, which total 10.3 Tcf in 2037 and account for 66% of natural gas exports in 2040.

In the low oil price case, with lower world oil prices, LNG exports are less competitive and grow more slowly, to a peak of 0.8 Tcf in 2018, and account for 13% of total natural gas exports in 2040.

Additional growth in net natural gas exports comes from increasing natural gas pipeline exports to Mexico, which reach a high of 4.7 Tcf in 2040 in the high oil and gas resource case (compared with 0.7 Tcf in 2013). In the high oil price case, natural gas pipeline exports to Mexico peak at 2.2 Tcf in 2040, as higher domestic natural gas prices resulting from increased world demand for LNG reduce the incentive to export natural gas via pipeline.

Natural gas pipeline net imports from Canada remain below 2013 levels through 2040 in all of the AEO2015 cases, but these imports do increase in response to higher natural gas prices in the latter part of the projection period.

Other key results from the AE 2015 reference and alternative cases include:

• Growth in crude oil and dry natural gas production varies significantly across oil and natural gas supply regions and cases, forcing shifts in crude oil and natural gas flows between U.S. regions, and requiring investment in or realignment of pipelines and other midstream infrastructure

• U.S. energy consumption grows at a modest rate over the projection period, averaging 0.3% a year from 2013 through 2040 in the reference case. A marginal decrease in transportation sector energy consumption contrasts with growth in most other sectors. Declines in energy consumption tend to result from the adoption of more energy-efficient technologies and existing policies that promote increased energy efficiency.

• Growth in production of dry natural gas and natural gas plant liquids (NGPL) contributes to the expansion of several manufacturing industries, such as bulk chemicals and primary metals, and the increased use of NGPL feedstock in place of petroleum-based naphtha.

• Growth in U.S. energy production, led by crude oil and natural gas, and only modest growth in demand reduces reliance on imported energy supplies. The national energy imports and exports come into balance starting in 2028 in the AEO2015 reference case and in 2019 in the high oil price and high oil and gas resource cases. Natural gas is the dominant U.S. energy export, while liquid fuels continue to be imported.

• Through 2020, strong growth in domestic crude oil production from tight formations leads to a decline in net petroleum imports and growth in net petroleum product exports in all AEO2015 cases. In the high oil and gas resource case, rising crude production before 2020 results in increased processed condensate exports. Slowing growth in domestic production after 2020 is offset by increased vehicle fuel economy standards that limit growth in domestic demand.

Net import share of crude oil and petroleum products supplied falls from 33% of total supply in 2013 to 17% of total supply in 2040 in the reference case. The U.S. becomes a net exporter of petroleum and other liquids after 2020 in the high oil price and high oil and gas resource cases because of greater production.

Related News

Related News

- Keystone Oil Pipeline Resumes Operations After Temporary Shutdown

- Freeport LNG Plant Runs Near Zero Consumption for Fifth Day

- Biden Administration Buys Oil for Emergency Reserve Above Target Price

- Mexico Seizes Air Liquide's Hydrogen Plant at Pemex Refinery

- Enbridge to Invest $500 Million in Pipeline Assets, Including Expansion of 850-Mile Gray Oak Pipeline

- Evacuation Technologies to Reduce Methane Releases During Pigging

- Editor’s Notebook: Nord Stream’s $20 Billion Question

- Enbridge Receives Approval to Begin Service on Louisiana Venice Gas Pipeline Project

- Mexico Seizes Air Liquide's Hydrogen Plant at Pemex Refinery

- Russian LNG Unfazed By U.S. Sanctions

Comments