July 2015, Vol. 242, No. 7

Web Exclusive

Summer Gas Prices in the Northeast: Why So Low? Why So Unpredictable?

As summer approaches, there are two things to know about natural gas prices in the New York/New England area. First, it is a difficult time to predict gas price movements in the Northeast. But in general, prices are down – and are likely to stay that way for this summer.

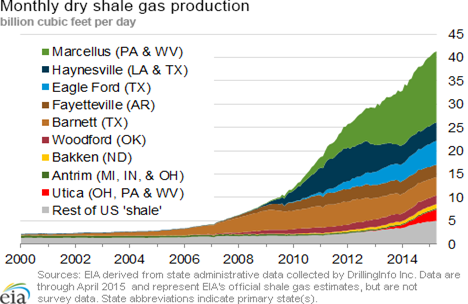

It’s hard to predict prices because there are a lot of new and unpredictable supply-and-demand dynamics across the country that are particularly pronounced in the Northeast. For instance, the explosion of shale gas production in the Marcellus and Utica shale regions.

Production in the nearby Marcellus, based in Pennsylvania and West Virginia, has tripled in just the past three years to 15 Bcf/d, roughly 20% of national production. This means that all of a sudden, we are awash in local natural gas.

How does this production boom fuel unpredictability? Persistent pipeline bottlenecks for local delivery in New England (and even sometimes the New York area), which cause prices to spike when shortages arise. Plus, gas shippers are looking to ship the Marcellus gas, which is cheap because of the production glut, south to Louisiana and west to Chicago, where it can be sold at better prices.

Meanwhile, no one quite knows at what rate new production will continue to increase, or how new pipelines coming on line will change the regional supply.

If production keeps quickly rising, the price will drop. But if new pipelines that are opening ship the Marcellus gas elsewhere faster than new production comes on line, local prices will rise. The result? A very unsettled and unpredictable market.

There are, however, three reasons to feel confident that prices will stay low this summer:

• First, there are the “forward” or “futures” markets, which put a million Btu of gas (a standard measure) at $2.70 or less for the summer, versus $4.40 last year. Basically, the futures price is what the market expects the going price to be a few months from now – but it affects today’s price too. The “contract,” or current monthly market price, on the local exchange, NYMEX, was at a three-year low in May, and is still low in June. This is because the region has restored our stocks of natural gas since the super-cold winter of 2013-2014, when prices spiked on account of a shortage. The shortage persisted into last summer, causing higher prices, but it is now essentially gone.

• The second reason is the weather itself. The region uses lots of gas to meet power and heating demands during super-hot summers and especially during super-cold winters. We had a moderate winter overall and temperatures have been moderate so far this spring, so there has been little pressure on supplies. On top of that, the National Weather Service and other private weather services predict a very cool summer that will not put a strain on gas supplies. This affects the futures market, where expected future prices partially dictate today’s price.

• The third reason is the potential for Marcellus shale gas supply to keep rising.

So how do these two forces – uncertainty but low price expectations – balance out? It’s a mix. The market is fairly confident that prices will stay moderate for the next few months; if they rise, it will be in accordance with historical averages, and stay below last summer’s price. After that, though, all bets are off. We’ll have to stay tuned to see how the supply, demand, and weather dynamics play out.

Author: Scott LaShelle is the newest member of Great Eastern Energy’s executive board, having joined the company in 2013. Prior to that, he was co-manager of Freepoint Commodities East Gas business after having managed Sempra’s East Gas desk. LaShelle holds a bachelor’s degree in foreign service from Georgetown University.

Comments