January 2015, Vol. 242, No. 1

Features

Opportunities In Africa Lean Heavily Toward Exports

Africa’s importance as a major energy supplier will grow with the development of recently discovered oil and gas fields, most notably in West and East Africa, which will generate 8,558 miles of additional oil and gas pipelines (Table 1).

According to the Organization for Economic Cooperation and Development (OECD), two-thirds of energy investment in Africa since 2000 has gone toward developing and transporting oil and gas for export. This investment can be characterized as either a component of national infrastructure, or in three cases, as a contribution to cross-border pipelines:

• Those that link Algeria with Europe (Figure 1)

• West African Gas Pipeline that links Nigeria with Ghana, Togo and Benin

• Pande Gas Pipeline that links Mozambique’s onshore gas fields with its major market in Johannesburg

A relatively new development in both East and West Africa is a shift toward regional integration of supply with its markets, as well as an intensive drive for domestic gas pipeline construction, distributing gas to power stations and industry, notably in Nigeria.

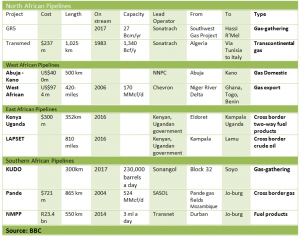

Table 1: Highlights of oil and gas pipelines by region

North African Pipelines

The planned East African trans-border regional pipeline network for Kenya, Uganda, Tanzania (LAPSET) is a response to the recent discovery of 1.7 Bbbls of oil in Uganda and 600 MMbbls of oil in the Lokichar basin of northern Kenya.

To develop these finds pipelines will gather oil from the fields of northern and western Uganda and join with a Kenyan pipeline connected with the port of Lamu, which is being expanded to act as a hub for the region’s oil exports. In addition, there are tentative proposals to develop a transport corridor to include South Sudan and Ethiopia, which would include the longest heated pipeline in the world.

In addition to exploring security issues, “Pipeline promoters need to get the plan, business model, tariffs, regulations and allocations right,” said consultant Elias Pungong, EY’s Africa Oil & Gas Sector (Figure 2).

Figure 2

National Pipelines

In Algeria, Sonatrach is investing about $3.48 billion in developing its Southwest Gas fields. Construction of the GR5 pipeline, designed to carry 20 Bcm/y to Hassi R’Mel for export to Europe, has started and is expected to be complete in July 2016.

Apart from Algeria, no other country in Africa has a nationwide gas pipeline network. To spur industrial development, Nigeria plans to invest $80 billion in the next five years in gas-fired electrical power generation, construction of 2,500 km of national gas pipelines and to nearly triple its gas output from 4 Bcf/d this year to 11 Bcf/d by 2020, according to Bloomberg.

This includes plans to build three pipelines from the Niger Delta to cities and power plants in the north, east and west of the country at a cost of $2 billion, according to the Lagos Africa Oil and Gas Report. There is also a plan to double capacity to 2 Bcf/d along the Esravos-Lagos pipeline system from Oben to Lagos by adding a 320-km, 36-inch pipeline.

At a cost of $4 billion, this will provide gas for the Geregu power plants, Dangote’s Obajana cement works and other industrial customers. The move will also supplement gas supplied to its neighbors, Ghana, Togo and Benin, via the frequently sabotaged West African Gas Pipeline (WAGP).

“It is generally recognized that better utilization needs to be made of the WAGP,” said Pungong. “Therefore, there are plans to have an LNG barge in Benin waters, connected to the WAGP in order to supply gas to power and industrial customers in Benin, Togo and Ghana.”

Offshore Pipelines

Pipelines are also being built offshore. A good example is the Kaombo Ultra-Deep oil project, lying in water up to 1,900 meters deep about 260 km from Angola’s coastline. Due for completion in the first half of 2018, 59 subsea wells will be connected via 300 km of pipelines to two floating production storage and offloading (FPSO) vessels.

Associated gas will be transferred to the Angola Liquefied Natural Gas (LNG) plant in Soyo for export. This is a classic example of an oil and gas export scheme designed to monetize resources for which there is little domestic demand (Figure 3).

Figure 3

Source: Enerdata

Refined Products Pipelines

In South Africa, government-owned Transnet recently completed construction of a petroleum products pipeline to ASME B31.4 standard for design materials, construction, assembly, inspection and testing of piping transporting liquids.

Designed to carry domestic and imported refined petroleum products from Durban to Johannesburg, it crosses 49 main rivers, 95 km of major wetland and 169 trenchless crossings. The project involved a variety of installation techniques to minimize excavation. This development has allowed Transnet to reduce fuel tankers on South Africa’s roads by up to 60% (See Figure 4).

Figure 4

Source: Frontier Market Network

Elsewhere in Africa, there are plans to extend the existing Kenyan Mombasa to the Eldoret refined products pipeline to Kampala, Uganda at a cost of $300 million. This, while Namibia’s stranded Kudu gas field, with an estimated 1.3 Tcf of reserves and the Nene Maine oil and gas discovery in the Congo, await development.

The dramatic 30% fall in oil prices since last summer will reduce revenues and capital budgets of governments and the energy majors, causing delays, postponements and even cancellation of some projects.

“It is becoming clear that as various domestic African economies advance, there will be an increasing need for output to be diverted to meet national economic needs,” said Pungong, citing Algeria, Nigeria and South Africa as examples.

“Elsewhere, despite the discoveries of oil and gas, this will not be enough to spark development of a significant local market for petroleum products, since other vital criteria are not in place, such as an educated workforce, oilfield service industry and well-developed road, rail and power infrastructure.”

In these cases, resource-rich fields will be developed for overseas markets and will require additional pipelines.

Comments