August 2014, Vol. 241, No. 8

Features

Russia-China Natural Gas Pipeline Agreement

The conclusion of a decade-long negotiation between Russia and China was announced May 21 during Russian President Vladimir Putin’s visit to Shanghai. The $400 billion natural gas supply contract between Russia’s Gazprom and China’s National Petroleum Corporation (CNPC) entails 38 billion cubic meters (Bcm) or 1.34 trillion cubic feet (Tcf) of Russian gas supply annually to China for 30 years via a new pipeline.

The commercial agreement between the world’s top energy supplier and the largest energy consumer came at a particularly interesting time when Russia’s relationship with its European energy customers is under strain as a result of the ongoing crisis in Ukraine. While several key aspects remain unknown, this pipeline gas deal highlights the growing importance of robust Asian markets over comparatively stagnant European markets and reflects the eastward shift in Russian energy strategy.

Q: Did the recent tension with Europe lead Russia to seal this deal?

A: The current tension between Russia and the West over Ukraine may have nudged forward the pipeline gas deal with China, but it did not drive the deal. Geopolitical tensions, triggered by Russia’s annexation of Crimea and uncertain ambitions in southeastern Ukraine, have put Russia’s already-weak economy under further pressure. It also increased Putin’s political need to return from China with a big gas deal in order to demonstrate the West cannot isolate Russia.

The most significant impasse was over the price. Gazprom wanted to use oil-linked sales contracts in Europe as a benchmark price, while CNPC proposed a lower price comparable to its pipeline gas imports from Turkmenistan, below $10 per MMBtu. While Gazprom puts the total value of the announced deal at $400 billion, the average delivered price is now believed to be about $350 per thousand cubic meters.

Meanwhile, details reveal that this may not exactly be a done deal. For example, the deal is supposed to entail a $25 billion Chinese loan or prepayment to help Russia finance field development and pipeline construction to the Chinese border, but the interest rate and repayment schedule may only become final in September.

Q: Does this deal signify a new and warmer phase in Sino-Russian relations?

A: There is growing economic synergy between the two countries, particularly in energy. While Russia needs diversified and growing market for its natural gas supply to help sustain its economy, China needs greater and diversified gas supply to meet its domestic energy demand that is essential for its economic growth and to improve environmental conditions.

To underscore the closer relationship between the two countries, several notable energy deals have been announced within the past 12 months. For example, a deal for Russia’s Novatek-led Yamal LNG project to supply at least 3 million tons of liquefied natural gas (LNG) to CNPC was also finalized during the Putin visit to Shanghai. Also, in June 2013, Rosneft agreed to double its oil supplies to China in exchange for $60-70 billion pre-payments from China.

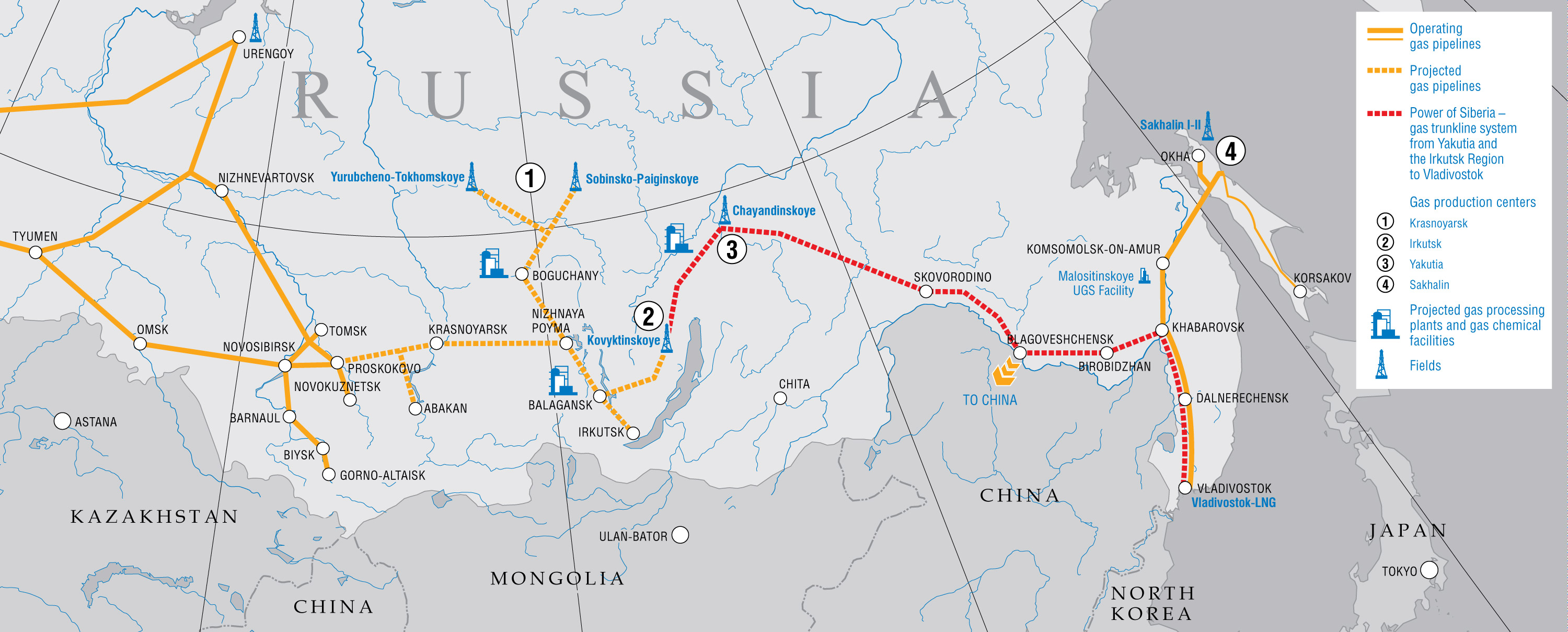

More notably, the Russians have agreed to allow Chinese equity investment in Novatek’s Yamal LNG project (a 20% stake by CNPC) and in one of Rosneft’s oil development projects in East Siberia (a 49% stake by CNPC) – rare moves by the Russian energy sector, which is generally closed to foreign equity investment. It thus has become a subject of intense interest and speculation whether the announced gas deal will include future CNPC investment in the two East Siberia fields of Chayanda and Kovykta, which the Chinese demanded to be the source of the pipeline gas.

Q: How significant is this deal to China and Russia from an energy market perspective?

A: The agreed-upon Russian gas supply volume is equivalent to a quarter of current Chinese natural gas consumption and about 10% of estimated demand by 2020. Depending on the Chinese gas demand outlook, the Russian supply volume would not preclude China’s future interest in concluding a deal to import LNG from the United States or anywhere else.

Russia is acutely aware of how robust shale gas production in the United States and future U.S. LNG supplies, along with other LNG supplies coming online in the next decade, will compete directly with Russia for market share in Asia. Given stagnant energy demand in Europe, Russia aims to increase its gas supply to Asia from 6% of exports currently to 31% by 2035. Russia’s pipeline gas supplies to China will likely begin in four to six years when global gas markets may see substantial levels of new supply added from Australia, Canada and East Africa, in addition to the United States. From the Russian perspective, the deal was always important to secure timely access to growing Asia gas markets but was perhaps pushed over the finish line by the additional need to send important geo-economic signals to the West in light of the crisis over Crimea.

Q: Does this deal mean that China is more interested in pipeline gas than LNG imports?

A: The Chinese government sees natural gas as a viable energy source to help address its over-reliance on coal, which supplies about 70% of the country’s electricity generation, but is a major cause of severe air pollution. China has become a growing natural gas consumer and importer as its domestic production is outpaced by demand in recent years.

China has been pursuing both pipeline gas and LNG imports. As of 2013, about one-third of the domestic consumption is met by imports, and the import volume is split nearly half-and-half between pipeline gas from Turkmenistan and Myanmar, and LNG from Asian and Middle Eastern producers, such as Australia, Qatar, Indonesia and Malaysia. The current Chinese government plan includes more than doubling the LNG receiving capacity in the next five years – 31 million metric tons per year (mmt/y) – or 1.51 Tcf/y today at nine terminals to more than 80 mmt/y or 3.9 Tcf/y at 15 terminals by 2018.

It is uncertain, however, whether there is enough room for both additional pipeline gas and LNG in China’s natural gas market down the road. One determinant is the future volume of pipeline gas imports from Central Asia and Russia. The Turkmen gas supply volume could triple to 65 Bcm/y or 2.3 Tcf/y, while the Russian gas supply volume may eventually amount to 68 Bcm/y or 2.4 Tcf/y. Another major uncertainty is the pace and success of shale gas development in China, with resources estimated at 1,115 Tcf, according to a U.S. Energy Information Administration (EIA)-commissioned study.

Q: Does the supply volume commitment endanger future Russian gas supplies to its European customers?

A: There should be no direct, immediate competition as the gas supplies to Europe come from West Siberia while the supplies to China will come from East Siberia. Specifically, the freshly inked agreement will see Gazprom produce and supply from two new producing fields in East Siberia. Gazprom is expected to invest $55-70 billion to develop two large gas fields in East Siberia and to build necessary pipeline infrastructure to the Chinese border. The region has become critical for the future viability of the Russian energy sector as production declines in West Siberia, where super-giant fields were discovered first, and are much closer to Europe. A second pipeline route, mentioned recently only by Russia but not China, entering western China could supply additional 30 Bcm of gas yearly, including from West Siberia.

Moreover, the prolonged economic crisis in Europe and the resultant slowdown in the regional energy consumption have posed economic difficulty to Russia, along with anemic domestic economic growth. Energy export revenue accounts for over 70% of its total export revenue and half of Russia’s federal budget revenue. Europe has been the destination for about 80% of the Russian oil and gas exports. The sluggish energy demand in Europe was another key reason for the Russian leadership to seek new opportunities in Asian markets.

Comments