May 2014, Vol. 241, No. 5

Features

Outlook Bright For Utility Construction Market

The utility construction market, and particularly the distribution and transmission pipeline construction market, are exceptionally healthy and the overall mood and perspective of contractors is one of great optimism.

In the immortal words of Led Zeppelin, the utility construction market has seen both good and bad times. The current market is perhaps the best for over 60 years and utility contractors are optimistic this market will continue for the foreseeable future. The optimism is particularly strong in the distribution and transmission pipeline construction markets, which are exceptionally healthy.

Utility Construction Index

Periodically, Continuum Advisory Group tests the perspectives of firms in the utility construction space to develop a utility construction index (UCI). This index is designed to test perspectives of infrastructure and utility construction industry firms and establish the degree of optimism or pessimism prevalent.

The index is made up of a confidence level, backlog projections, cost and productivity factors, and business outlook for all of the utility sectors including: electric power transmission and distribution (T&D), telecom, gas and liquid T&D, and water and sewer. Nine factors were fed into the summary and were tested through two recent nationwide surveys of utility contractors. The results demonstrate seven factors as optimistic and improving and two factors rated as pessimistic or worsening (Exhibit 1).

The greatest points of optimism are the expected improvements in backlog, continued improvements in the firm’s performance and continued improvement in the utility construction markets where they do business. The least optimistic area is in the overall economy, where the level of optimism has fallen since third quarter 2013. The concerns that have slowed the level of optimism revolve around federal monetary policy, deficit spending, the national debt, executive branch leadership and a dysfunctional Congress. Expectations of rising costs in construction materials and labor are the two factors where pessimism rules.

Historic Perspective

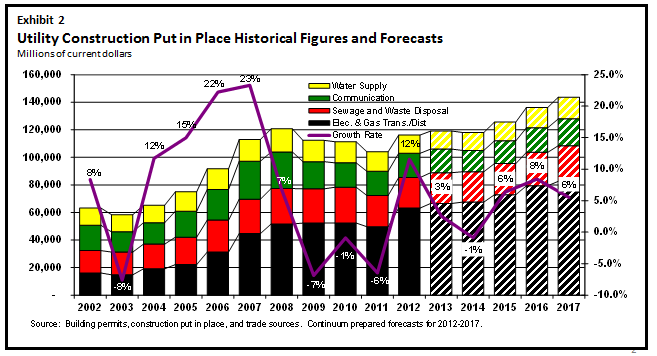

Perspectives on utility markets have moved up and down dramatically since the financial and economic crisis in 2008-2009. Utility construction spending has performed better than any other type of construction, exhibiting the smallest amount of shrinking in 2009, 2010, and 2011. The electric and gas sector performed the absolute best, exhibiting steady spending from 2008 through 2010 and only very modest shrinking in 2011. Growth has and will continue unabated in this sector through the forecast period of 2017 (Exhibit 2).

As a frame of reference, electric and gas construction has experienced more than a decade of spending growth, moving from about $20 billion in 2004 to more than $60 billion in 2014, and potentially $80 billion in 2017. It is Continuum’s belief and forecast that the pipeline construction market will experience three 5-to-7 year waves of spending increases.

The first wave began in earnest in 2010-2012 and will flatten out around 2015-2017, after which it will again accelerate. A second and third wave will take place, and by 2030-2035 much of the pipeline infrastructure in the United States will have been newly built or replaced with high-quality and performance materials yielding a more effective and safe system.

The swings in construction spending yield swings in perspective that are evident in the UCI. Two troughs in perspective and optimism occurred prior to third quarter 2009 (not depicted) and in third quarter 2012. Since 2012, the level of optimism about the utility market and specifically the pipeline market has continued to exhibit both positive perspective and very high optimism with index figures well above 50.0 (Exhibit 3).

Among the various utility construction sectors, gas transmission and distribution exhibit the highest optimism over three-month, one-year, and three-year timelines (Exhibit 4). Index scores above 50 indicate an improving market and level of optimism. An index score of 100 is the maximum on the scale, and the pipeline sector exhibits scores of 80 or higher over all of the timelines. This far exceeds the level of optimism in any of the other segments.

Scarcity And Constraint

The optimism in this sector is only tempered by the scarcity that is faced. The utility market sector, and more particularly the pipeline construction sector, is already experiencing scarcity. Looking forward, these challenges will continue to the point at which only the most progressive and forward-thinking contractors will thrive. What will be faced includes:

• Labor: Low birth rates, aging population and lower percentage of people participating in the workforce.

• Utility internal workforce over age 55: 40% of inspectors, 25% of surveying and mapping specialists, 25% of operating engineers, 25% of petroleum engineers, 25% of frontline supervisors, etc.

• User rate increases: Ratepayer and Public Utility Commission (PUC) fatigue due to rates rising faster than inflation since 2005.

• Technology innovation: The pace of change in the construction industry is glacial and must accelerate.

The obvious reaction to scarcity is to see challenges as opposed to promise and opportunity. We believe successful firms will embrace the growth and potential scarcity in these markets for what they are … promise and opportunity.

Conclusion

“No matter how I try, I find my way into the same old jam…” Don’t get caught in the same old jam and embrace our environment as one filled with promise and opportunity. We offer three critical strategies to help innovative contractors thrive:

• Strategic thinking: Picking the right geographies, market segments, customers and service types will prove critical and applying strategy thinking techniques to this challenge is one powerful solution.

• Skill building: Given the various types of scarcity, particularly labor scarcity, building internal skills through training can provide the stamina needed in a challenging environment. Three types of training, technical, management and cross functional, are necessary.

• Embrace innovation, disruption and scarcity: Three areas require particular attention: integration of communication and asset management technology into design and construction; 4D and 5D design and construction preparation techniques, generically referred to as building information modeling (BIM); and integrated project delivery techniques.

Utility capital asset owners, facility operators and utility construction service providers must pick the right markets, build their skills and embrace scarcity for the opportunities it presents in order to cause the optimism felt to come to fruition.

1. “Civilian Labor Force Participation Rate” Bureau of Labor Statistics, October 1, 2013.

2. “Current Population Survey” Bureau of Labor Statistics.

3. “Electric Power Monthly” U.S. Energy Information Administration, September 30, 2013.

Authors: Mark Bridgers and Nate Scott are consultants with Continuum Advisory Group, which provides management consulting, training, and investment banking services to the worldwide utility and infrastructure construction industry. They can be reached at (919) 345-0403 or MBridgers@ContinuumAG.com

Comments