February 2013, Vol. 240 No. 2

Features

Natural Gas Production Growth To Continue In 2013, 2014

Natural gas production levels in 2012 will establish a new record for the third straight year. Year-over-year production growth has slowed from 2010 and 2011 levels, but it has not reversed. Production growth is forecast to continue into 2013. Additional production growth also is expected in 2014.

The shale revolution is transforming the natural gas industry in the U.S. Just five years ago, natural gas was viewed as an unreliable and scarce energy source, causing the U.S. to be dependent on natural gas imports. Today, natural gas production in the U.S. has surpassed even the most optimistic forecasts. The U.S. is projected to become an exporter of natural gas by 2016.

Abundance of supply has created new issues. Prolific natural gas production is altering historical pipeline flows. New pipeline construction in the previously constrained Northeast is good news for consumers in that region. However, this growth is causing other pipelines to be severely underutilized, forcing those pipeline operators to consider the alternatives of bidirectional service, conversion to the transportation of crude oil or natural gas liquids, or abandonment.

Additionally, coal-fired power plants are being retired and replaced with clean-burning natural gas-fired power plants in order to help operators comply with pollution and emission regulations.

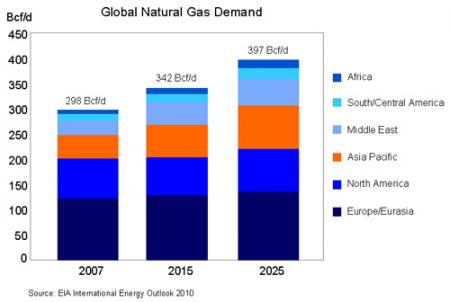

The potential surge in natural gas demand has prompted questions on how this increase in demand will impact natural gas prices, particularly when the U.S. begins to export natural gas supplies.

Energy Solutions, Inc. Natural Gas Price Outlook evaluates numerous natural gas price drivers and concludes production will remain strong with the pricing environment remaining relatively weak into 2013, before moving gradually higher in 2014 and 2015.

This conclusion is based on the following:

Production Levels Continue To Climb In 2013 And 2014. The economic benefits of natural gas liquids (NGLs) and associated gas production, combined with improved rig efficiencies, reduced drilling times, higher production yields, reduced expenditures, and overall improved profitability, causes natural gas production levels to continue to expand by 0.5 Bcf/d in 2013.

Growth primarily will be focused in the Appalachians as new pipeline capacity was projected to support an additional 1.8 Bcf/d of natural gas flows from the Marcellus Shale by the end of 2012, and another 3.4 Bcf/d of gas flows in 2013. This is new supply that is projected to come from approximately 1,000 wells waiting to come online in the Marcellus Shale.

Producers Plan To Continue Drilling Efforts. Data shows producers established realistic budgets for 2012 drilling commensurate with the expectation of lower revenues. Data also indicates that several large shale producers are well-hedged for 2013. These hedged positions provide insulation from low natural gas prices by stabilizing sale prices.

Significant budget and drilling cuts are not expected in 2013 because natural gas prices are expected to rise from 2012 levels. In addition, improved efficiencies, lower expenses and revenue supplements of NGLs and associated gas, are yielding rates of return ranging from 40-80% in some liquid-rich supply basins.

Coal Prices Will Serve As Both A Price Floor And A Price Ceiling For Natural Gas Prices. Record summer heat and collapsing natural gas prices were the perfect solution to an oversupplied natural gas market. On average, in 2012, natural gas demand from the electric power sector rose by 5 Bcf/d, virtually eliminating the year-over-year surplus in storage inventories. Even with this increase in natural gas demand, natural gas storage inventories reached a new record high in 2012.

Slightly stronger natural gas prices, but steady coal prices, are expected to force about 2 Bcf/d of natural gas demand from the electric power sector back to coal-fired electric generation. Absent site-specific considerations, including transportation, on a per MMBtu basis, fuel switching from coal to natural gas in eastern markets, which use Central Appalachian (CAPP) coal, tends to occur at around $2.75 per MMBtu.

Fuel switching from coal to natural gas will accelerate as natural gas prices fall below that price level. When natural gas prices are above this price level, there typically is an economic incentive to utilize coal-fired electric generation, which reduces natural gas demand, but also reduces coal stockpiles. Falling natural gas demand tends to lead to weaker natural gas prices and falling coal stockpiles tend to lead to rising coal prices.

As natural gas prices fall and coal prices rise, a larger amount of coal-to-natural gas fuel switching will occur. As this occurs, natural gas demand rises, and coal stockpiles rise. Rising natural gas demand tends to lead to stronger natural gas prices and rising coal stockpiles tend to lead to weaker coal prices. As natural gas prices rise and coal prices weaken, the economic incentive to utilize natural gas-fired electric generation as a substitute for coal-fired electric generation diminishes. The battle of these two fuels for a share of the electric generation market is expected to keep the price of both commodities in check.

Natural Gas Prices Remain At Historically Low Levels Into 2015. There are no concerns over meeting near-term natural gas demand for the upcoming winter and into the next few years, keeping natural gas prices, on average, at historically low price levels. In 2012, the average calendar year natural gas NYMEX price was $2.789 per MMBtu. By comparison, the average calendar year 2013 natural gas NYMEX price is expected to range from $3.35-3.85 per MMBtu with an increase to $3.50-4.25 per MMBtu in 2014 and an increase to $4.75-5.50 per MMBtu in 2015.

In 2012, the front-month natural gas NYMEX price hit a low of $1.902 per MMBtu on April 19 and climbed to a high of $3.91 per MMBtu on November 21. While these prices are still very low in comparison to historical levels, the price move does represent a 200% increase in the value of the front-month natural gas NYMEX price. Similar price volatility is expected in 2013, with price weakness primarily concentrated in the first four months of 2013.

The market research and conclusions in Energy Solutions, Inc. Natural Gas Price Outlook will help businesses better understand the changing natural gas environment in order to make more informed decisions related to the purchase or sale of natural gas or related products. Natural Gas Price Outlook concludes that while there are no immediate threats of a return to the double-digit natural gas prices experienced in 2008, the overall price trend does turn higher.

For more information on this in-depth analysis, visit www.NaturalGasOutlook.com or e-mail the publisher, Valerie Wood at vkwood@energysolutionsinc.com.

Comments