June 2012 Vol. 239 No. 6

Features

Low Gas Prices Drive Operators To Liquids Shale Plays

Pipeline & Gas Journal, in partnership with the Interstate Natural Gas Association of America (INGAA), held its eighth annual Pipeline Opportunities Conference April 4 at the George R. Brown Convention Center in Houston.

Jeff Share, conference founder and organizer, said the single-day event drew 400 attendees, said reaction at the event was reflective of the intense focus on the pipeline industry, both for natural gas and for oil products.

“We’re in a time when natural gas is making news somewhere in America every day. Add the controversy over the Keystone Pipeline project in a crucial election year and there has never been more interest in our business. There is only one certainty today in the oil and gas industry which is that no one is certain about anything that could happen tomorrow,” said the editor of Pipeline & Gas Journal.

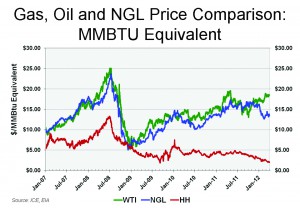

In the natural gas perspective session, Adam Bedard, senior director, Energy Analysis, Bentek Energy, provided an overview on how low natural gas prices are driving producers to the nation’s oily shale plays.

To put this in perspective he shared the accompanying slide showing a comparison of gas, oil and NGL prices on an MMBtu equivalent basis. “If you are a producer and have assets around the country you’re going to go after natural gas liquids or oil because you’re going to get two to three times the value that you would get for dry gas,” he said.

To push the point further he shared the accompanying slide and told attendees, “You can see the numbers changing dramatically as natural gas prices and the rate of return (ROR) in these dry gas plays decline.”

He was also quick to point out that while the rate of return (ROR) on dry gas plummeted, oil plays are holding up, with the Bakken reporting a 50% ROR; Niobrara, 48% , Permian Basin, 66%, etc.

Bedard said given the low ROR, producers are not going to be drilling as many dry gas wells and that is reflected in the drilling rig count shown in the accompanying slide.

“One example is the Haynesville where 66 rigs are currently active, 43 less than a year ago. If you look at the hot oily plays, Eagle Ford has 250 active rigs, which is an 85-rig increase from a year ago; Permian Basin, 480 active rigs, up 89 from a year ago; and Anadarko 251, up 16 from a year ago.

“So, the liquids plays are attracting the producers and the rigs.”

In the challenges for oil and natural gas session, Bill Moss, Partner, Mayer Brown LLP, provided a look at the prospect of natural gas becoming a world global market, with particular reference to the U.S. market.

Noting the radical changes in supply and demand of natural gas in the U.S. from the shale revolution, Moss said, “In the last five years the entire situation has changed and we’re looking at a vast oversupply of natural gas. Looking back to 2000, shale gas was 1% of our natural gas supply.

“Future projections by the U. S. Energy Information Administration show shale gas contributing 47% of the nation’s natural gas supply production in 2035. Moreover, North American natural gas reserves are reportedly sufficient to supply current consumption for more than 100 years.”

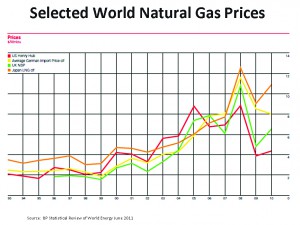

Turning to gas prices, Moss used the accompanying slide to show the disparity in natural gas prices in the U.S. vs. select areas of the world.

“Obviously, this incredible difference in price offers a real opportunity if you can get the gas, in the form of LNG, out of the U.S. and export it elsewhere,” he said.

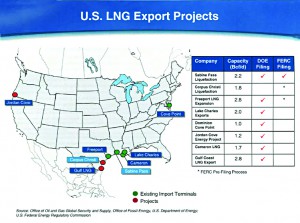

As to future LNG export regulatory hurdles, Moss doesn’t view this as insignificant. A number of companies have filed for LNG export permits and Sabine Pass Liquefaction, a subsidiary of Cheniere Energy Inc., won approval from U.S. regulators to export 2.2 Bcf/d of LNG around the world from a terminal in Sabine Pass, LA. The permit is a second for the Cheniere subsidiary. The company won a permit earlier to export LNG to countries that have a free-trade agreement (FTA) with the U.S., such as Mexico and Canada.

The accompanying figure shows LNG export filings that have been submitted to the U.S. Department of Energy and the Federal Energy Regulatory Commission (FERC).

He also noted that it was unclear if companies are going to be able to obtain a non-FTA license, like Cheniere has, to export gas to a much broader array of countries.

While LNG exports are expected to create jobs and provide markets for domestic natural gas, there is a tremendous amount of political pressure against allowing the export of natural gas. One main concern is that exports could lead to higher natural gas prices in the U.S. That latter point is why Moss said the manufacturing sector, which is concerned that the competitive advantage the industry in the U.S. now has and credits in part to cheaper energy, is one of the main opponents to the export of natural gas.

“There is also that core opposition from environmental groups that oppose any extraction of hydrocarbons,” he said.

Other highlights of the session included speaker Robert Bryce, energy writer and author of Power Hungry and Gusher of Lies, who discussed the impact of CO-2 emissions.

Bryce said that over the last decade the five countries with the biggest percentage growth in CO-2 emissions were Vietnam, 137%; China, 123%; Qatar, 115%; Trinidad 84%; and India with 78%.

Over the last decade, he said, U.S. CO-2 emissions could have gone to zero and global CO-2 emissions still would have increased.

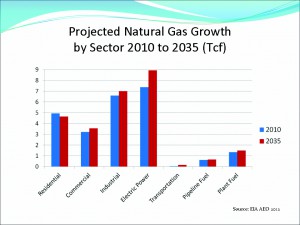

Also, J. Mark Robinson, consultant, URS Corporation, who spent 31 years with the FERC, gave a lively Washington perspective focusing on energy past and energy future.

Robinson shared the accompanying slide showing the growth of natural gas by sector from 2010-2035 and the 1.5 Tcf of growth in electric power projected over the 25-year period.

In a Q&A session, Kelcy C. Warren, chairman and CEO of Dallas-based Energy Transfer Partners, outlined key issues facing midstream operators in today’s fast-moving environment.

A huge challenge, he said, is determining the rules of the game. The worry is that the government will suddenly say we’re not playing that game anymore and come up with new rules, he said.

Touching on what would enhance the midstream sector, Warren said consolidation would help. Warren had just finished completing the acquisition of Southern Union Group and was quietly in the process of acquiring Philadelphia-based Sunoco in a pair of multibillion-dollar acquisitions that will make ETP a major player in the natural gas and natural gas liquids businesses.

In giving his perspective on mature shale plays he considered the most profitable, Warren identified the Marcellus, Eagle Ford and the Permian Basin as “extremely profitable.”

“We’re higher right now on the Permian Basin than any other region in the U.S., he said. “There are multiple zones in the Permian and the producing community is proven. They know what they’re doing and have been doing it for a long, long time.”

In noting concerns, Warren saw problems with future pipeline in the Marcellus. “You don’t know what it will cost to build infrastructure,” he said.

He also noted that the Marcellus is in Pennsylvania and West Virginia, areas that don’t have eminent domain. “The bandwidth of cost estimates could well be a 50-70% contingency,” he said. “Unlike Texas, where you have eminent domain, you might have a 5% contingency vs. a 70% contingency in the Marcellus.”

Warren also considers the Haynesville Shale dry. “I question whether you can drill a Haynesville well today that would make any economic sense unless you are just drilling it to hold acreage,” he said.

As for the Bakken, he sees a lack of infrastructure in this region as a problem. “There is not a lot of natural gas associated with the Bakken,” he said, “and the majority of the crude in the Bakken is presently being trucked to rail sites and railed to wherever possible.”

He anticipates a crude line being built in the Bakken although now it remains a problem.

Cathy Landry, communications director for INGAA and the INGAA Foundation, shared her thoughts on what could be expected in the near-term in Washington.

For the most part she indicated that since no one knows who will win the election there is little incentive in Washington to move forward with new legislation. Nevertheless, she did express concern that both the EPA and environmentalists seem to be focusing on methane and the capture of fugitive emissions.

This could be potentially serious for the natural gas industry, Landry said, because on a carbon footprint basis natural gas does pretty well, then again, there is a lot of methane from natural gas and methane is a much more potent greenhouse gas than carbon dioxide.

In the event the EPA and the environmentalists go after methane, she warned natural gas could face some serious limitations.

Landry also briefly discussed a recently released INGAA Foundation study which estimates that by 2035 $230 billion will be invested in oil, gas and NGL pipeline infrastructure projects, (see Pipeline & Gas Journal, May 2012 for details.)

Luncheon keynote speaker Mark R. Rosekind, Ph.D. Board Member, National Transportation Safety Board, provided an informative presentation on the findings and recommendations resulting from the San Bruno explosion in 2010.

While noting that mistakes were made prior to the San Bruno explosion, Rosekind said pipelines remain the safest and most cost-effective means to transport the extraordinary volumes of natural gas and liquids that fuel our economy.

The NTSB official emphasized that pipeline companies follow strict regulations and standards to ensure pipeline safety. “As a result,” he said, “serious pipeline incidents are increasingly rare.”

A major focus of the pipeline construction session was on new and planned projects. Royston Lightfoot, senior vice president Business Development at Crosstex, discussed the Cajun Sibon expansion that involves expanding the company’s fractionation facilities in Louisiana and constructing a new NGL pipeline that would expand access to these facilities and the Louisiana products markets.

The new pipeline will be an extension of the company’s 440-mile Cajun Sibon NGL pipeline.

When completed in 2012, the 130-mile, 12-inch extension will connect the company’s Eunice fractionation facilities in Louisiana to its Mont Belvieu supply pipelines in Texas. Crosstex will invest an estimated $230 million in these projects.

Also in the session, William Moler, president and COO, Inergy Midstream L.P. overviewed development of the Marc I Pipeline and the opposition encountered in trying to get the project approved.

According to Moler, 21,000 letters of opposition were submitted to the FERC about the project, while only eight of those came from landowners who would actually be impacted by construction of the project.

Noting that the highest number of letters came from China, Switzerland and France, he said, “The opposition is changing. It is not about the pipeline, it is about hydraulic fracturing. The pipeline simply gives the opposition a voice and – in FERC’s public way of approving pipelines – it gives them a very loud voice.”

Nevertheless, the 39-mile, 30-inch bi-directional Marc I gas pipeline in northern Pennsylvania is under construction and scheduled for completion this summer.

Insert Slide from Inergy titled: Commonwealth Pipeline

The Inergy official also discussed plans to jointly market and develop the Commonwealth Pipeline with affiliates of UGI Corp. and WGL Holdings, Inc. The proposed 200-mile, 30-36-inch pipeline is expected to transport at least 800,000 Dth/d when it is placed into service in 2015. Its primary purpose is to provide a direct and flexible path for bringing natural gas produced in the Marcellus and Utica Shale plays in Pennsylvania and neighboring states to growing natural gas markets in central and eastern Pennsylvania, the metropolitan areas of Philadelphia, Baltimore, and Washington, DC, and the Delmarva Peninsula. Plans are for Inergy Midstream to construct and to operate the pipeline, which is expected to cost approximately $1 billion.

Shortly after the conference, sponsors of the project announced a non-binding open season running to June 8, 2012 for the pipeline.

J. Mario Rivera, Energy Transfer Partners’ senior vice president, Commercial Operations, shared the accompanying slide with attendees. It lists the company’s gas pipeline and processing facilities with completion dates into 2013.

Insert Energy Transfer Slide titled: Gas Pipeline Project

Marc Rothbauer, director of Operations Support, Atmos Energy, focused on the company’s steel service line replacement of distribution service lines.

In explaining the decision to tackle the replacement project, he said the decision came at a time when many distribution integrity management activities were going on.

He said, “After a lot of conversations and data evaluation we looked at where our problems were and it pointed to steel service lines. Those assets had been in the ground for many, many years and had served us well…Nevertheless a decision was made to move forward with the goal being to replace 100,000 service lines from the main to the customer’s meter.”

After Atmos confirmed exactly where all the service lines were located throughout their system, the project kicked off in March 2010. Today, there are a total of 10 contractor and 117 three-man crews working in 18 different cities to complete the project. So far, 73,000 have been completed. Rothbauer said the target completion date for the project is September.

Spectra Energy’s Elie Atme, director, Northwest Business and Development, overviewed the company’s expansion opportunities in the 2014-2017 time frame and shared a slide listing the projects. Conference attendees can access the slide on the Pipeline Opportunities website. www.pipelineopportunities.com/

Comments