January 2012, Vol. 239 No. 1

Features

2012 Worldwide Pipeline Construction Report

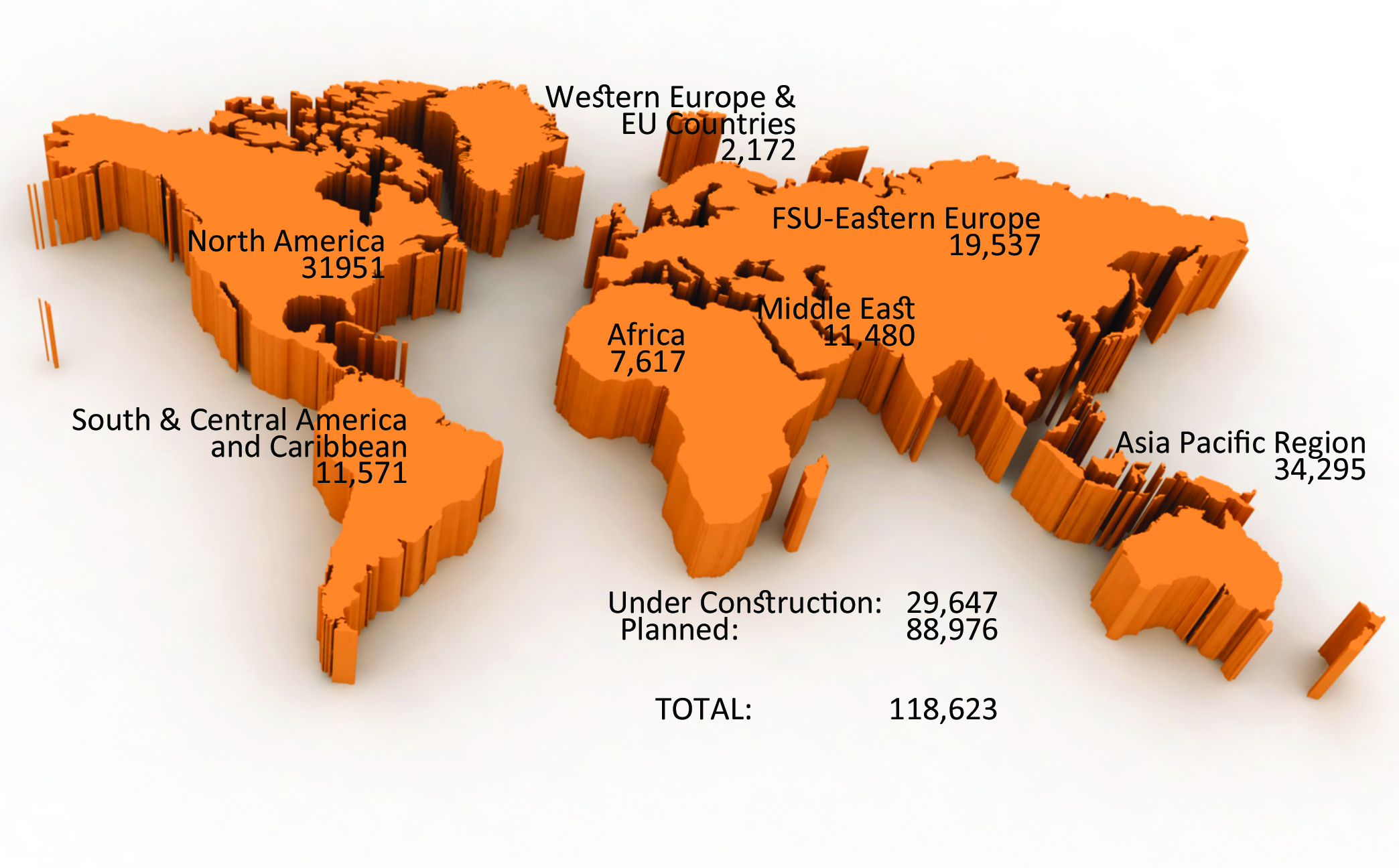

P&GJ’s worldwide survey figures indicate that 118,623 miles of pipelines are planned and under construction. Of these, 88,976 represent projects in the planning and design phase; 29,647 miles reflect pipelines in various stages of construction.

Natural gas pipelines again account for the majority of projects under construction and planned.

Supporting this is a GlobalData report that indicates approximately 75% of the total global planned pipeline additions during 2011-15 will be gas. The report says the Asia Pacific region should be responsible for 41.8% of total planned pipeline additions with China and India being the frontrunners.

Construction Overview

Following is a look at new and planned pipeline miles in the seven basic country groups, (see area map): North America – 31,951; South/Central America and Caribbean – 11,571; Africa – 7,617; Asia Pacific 34,295; Former Soviet Union and Eastern Europe – 19,537; Middle East – 11,480; and Western Europe and European Union – 2,172. For information on these and other pipeline projects, see P&GJ’s sister publication, Pipeline News.

North America

Nothing has changed the outlook for the North American energy industry quite like the discoveries in the shale regions in the U.S. and Canada. North America – which accounts for 26,300 miles in the planning stages and 5,651 miles under construction – should remain strong.

Those building pipelines in shale regions can expect higher costs. Ziff Energy Group reports pipeline owners are seeing higher construction costs in the shale regions of Marcellus, Eagle Ford, Haynesville, Barnett, Woodford, Fayetteville, and Horn River.

After analyzing costs of 120 pipelines from the past decade, Ziff Energy Group’s results show the average estimated shale gas pipeline rose in 2011 to almost $200,000/inch-mile, three times higher than 2004.

“All North America geographical regions appear to experience consistently higher pipeline costs than prior years,” commented Julia Sagidova, gas analyst and lead

author of the report. “The Marcellus shale gas region (Pennsylvania) is the most expensive with an average cost of under $300,000/inch-mile. These large-diameter (24-36 inches) projects are typically 120 miles in length and cost $500 million.”

The report noted that the 30% rise in steel costs over the past year along with new industry regulations and practices to reduce right-of-way and minimize environmental effects are driving up construction costs.

In North America, work is progressing on DCP Midstream’s 700-mile Sandhills Pipeline. DCP is using new construction and existing pipeline to build a 100,000-120,000-bpd NGL pipeline that will run from West Texas to Mont Belvieu in East Texas. The pipeline will be phased into service, with the first completed in the third quarter to accommodate DCP’s growing Eagle Ford liquids volumes. Service to the Permian Basin will be available as soon as the Q2 2013.

Greencore Pipeline Company LLC, a fully owned subsidiary of Denbury Resources Inc., is building the 231-mile, 20-inch Greencore CO-2 Pipeline from the ConocoPhillips Lost Cabin Gas Plant in Fremont County, WY, to a point in the Bell Creek oil field in Powder River County, MT. The CO-2 transported by the Greencore Pipeline will be used for enhanced oil recovery at the existing Bell Creek oil field. Completion is scheduled in late 2012.

Still awaiting a construction start is TransCanada’s $7 billion Keystone XL Pipeline. The route of the 1,661-mile, 36-inch crude oil pipeline begins at Hardisty, Alberta and extends southeast through Saskatchewan, Montana, South Dakota and Nebraska.

Late last year, the State Department announced it would delay a final verdict on whether the pipeline is in the national interest until early 2013 in order to conduct an environmental analysis of an alternative route that would navigate the pipeline away from environmentally sensitive areas in Nebraska.

North America also accounts for several pipelines in the planning and engineering phase, including Kinder Morgan’s 240-mile Cochin Marcellus Lateral Pipeline that will originate in Marshall County, WV and terminate at an interconnect with the KM Cochin Pipeline in Fulton County, OH. Once completed, the pipeline will transport NGLs from the Marcellus producing region of Pennsylvania, West Virginia, and Ohio to fractionation plants and petrochemical facilities in Illinois and Canada. The target in-service date for the pipeline is mid-2012.

Enterprise Products Partners L.P. plans to build a 1,230-mile pipeline to transport ethane from the Marcellus and Utica shale regions in Pennsylvania, West Virginia and Ohio to the company’s natural gas liquids storage complex at Mont Belvieu, The pipeline would have an initial capacity of 125,000 bpd and can be expanded to meet increased shipper demand. Commercial operations are slated in Q1 2014.

Oneok Partners will invest $910 million to $1.2 billion by late 2013 to: 1) construct the new 570-mile, 16-inch Sterling III NGL Pipeline to transport either unfractionated NGLs or NGL purity products from the Midcontinent to the Texas Gulf Coast; 2) reconfigure its existing Sterling I and Sterling II NGL distribution pipelines to transport either unfractionated NGLs or NGL purity products; and 3) build a 75,000-bpd NG fractionators, MB2, at Mont Belvieu. The Sterling III Pipeline will cost between $610-810 million and have an initial transport capacity of 193,000 bpd with possible expansion to 250,000 bpd. The pipeline will traverse the Woodford shale and provide transport capacity for NGL production from the growing Cana-Woodford Shale and Granite Wash play. Completion is scheduled in 2013.

Getting Alaska’s North Slope (ANS) natural gas to market has been an elusive goal since oil production started in the late 1970s. Plans to build a major natural gas pipeline to deliver ANS natural gas to markets have come and gone over the years. One project still being evaluated to deliver North Slope natural gas is the 1,717-mile TransCanada-ExxonMobil Alaska Pipeline that would extend from Prudhoe Bay to points near Fairbanks, and Delta Junction, AK and then to the Alaska-Canada border where it would connect to a new pipeline that will link up with the pipeline system near Boundary Lake, AB.

TransCanada plans to file permitting applications in both the U.S. and Canada in Q4 2012 with approvals anticipated in Q4 2014. Construction of the $32 -41 billion project is scheduled to start in 2015 with first gas being available in mid-2020.

Still awaiting a development decision is Canada’s Mackenzie Valley natural gas pipeline project that received the stamp of approval from an independent panel charged with considering the environmental, social and economic impacts of the proposed $16 billion, 743-mile line on the Northwest Territories.

In Mexico, a McDermott International subsidiary completed a project to install three oil and gas pipelines for PEMEX Exploración y Producción in the Bay of Campeche.

Asia Pacific

Countries in the Asia Pacific region are undertaking massive construction projects to meet growing energy demand. The region accounts for the highest number of new and planned pipeline miles. Some 20,234 miles represent projects in the engineering and design phase; 14,061 miles reflect projects in various stages of construction with China, India and Australia the most active areas.

Work is winding down on one of China’s most significant projects: Petro China’s second West-to-East natural gas pipeline. Eight regional lines should be completed by June. The pipeline will carry 30 Bcm/a of gas from central Asia and northwest Xinjiang Uygur Autonomous Region to the Yangtze and Pearl River deltas.

Total pipeline length, including regional lines, is 5,656 miles. The project traverses 15 provincial regions and will serve more than 400 million people.

A third West-to-East gas pipeline project is expected to take more than 20 Bcm/a of gas from central Asia; a fourth and fifth are planned in the future.

China’s first West-to-East pipeline, which pipes gas from Tarim Basin of Xinjiang to Shanghai, is designed to transmit 12 Bcm/a of natural gas.

In Yunnan Province, China National Petroleum Corp. (CNPC) is building two pipelines and a refinery to transport and process oil and natural gas from Myanmar starting in 2014. The planned 550,000-bpd oil pipeline and the 12 Bcm/d gas pipeline will each require 500 miles of construction in Myanmar to the China border city of Ruili. The two lines will then extend another 1,056 miles in Yunnan Province before reaching their destination.

In India, a consortium of four state-run companies led by Gujarat State Petronet Ltd. (GSPL) has received contracts for construction of three major pipeline projects. The contracts are for the 951-mile from Mallavaram-Bhilwara in the southern state of Andhra Pradesh to Bhilwara in the northern state of Rajasthan, the 1,025-mile Mehsana-Bhatinda pipeline from western to northern India and the 466-mile pipeline to Jammu and Kashmir from Bhatinda.

In Thailand, Punj Lloyd is building a 185-mile pipeline for PTT LNG to transport gas from an LNG terminal near Rayong. The project requires 45 horizontal directionally drilled crossings and is set for completion by year-end 2013.

Australia/Papua New Guinea

LNG continues to be the big newsmaker in Australia which accounts for seven sites under construction and eight more in the planning or engineering phase.

Marking the start of one of the country’s latest mega-projects is the $16 billion Santos GLNG LNG plant on Curtis Island. The plant includes the development of coal seam gas (CSG) resources in the Bowen and Surat Basins in southeast Queensland, construction of a 261-mile gas transmission pipeline from the gas fields to Gladstone, and two LNG trains with a combined nameplate capacity of 7.8 mtpa on Curtis Island.

Once completed, GLNG alone will supply 11% of Korea’s domestic gas needs and 9% of Malaysia’s gas consumption. First LNG exports should start in 2015.

In western Australia, Chevron Australia and its joint venture partners ExxonMobil, Shell, Osaka Gas, Tokyo Gas and Chubu Electric Power are working on the multibillion-dollar Gorgon Project. The project will develop the Greater Gorgon area gas fields, located off the northwest coast where five fields have been discovered.

In Papua New Guinea, Esso Highlands Ltd., operator of the PNG LNG project, continues to make progress on meeting the 2014 startup window. Esso awarded the EPC contract to a joint venture of Chiyoda and JGC Corp. for a 6.6 MMt/a LNG plant, with two trains. The contract includes construction of the 435-mile natural gas pipeline from Southern Highlands to Port Moresby in PNG. The pipeline work is projected to be completed when the $10 billion LNG project gets off the ground in 2014.

FSU- Eastern European Countries

Russia and nations in the FSU and Eastern Europe hold promise for future oil and gas activity and several are constructing and planning extensive pipeline networks to Europe and the Asia Pacific region.

Nord Stream AG inaugurated the Nord Stream twin pipeline system on Nov. 11 which runs from Vyborg, Russia to Lubmin near Greifswald, Germany. The two 760-mile offshore pipelines are the most direct connection between the vast gas reserves in Russia and energy markets in the European Union. When fully operational later this year, the pipelines will have capacity to transport a combined total of 55 Bcm of gas a year to the EU for at least 50 years.

Construction of Line 1 of the twin pipeline system began in April 2010 and was completed in June 2011. It began transporting gas in November 2011. Construction of Line 2, which runs parallel to Line 1, began in May 2011. The second line is planned to come on stream later this year. Each line has a transport capacity of 27.5 Bcm/a of natural gas.

Transneft is contractor and operator on the Zapolyarye-Purpe oil pipeline project. The 310-mile Zapolyarye-Purpe pipeline, with capacity to ship up to 45 MMt/a of crude, will transport oil from the Yamal-Nenets Autonomous District and northern Krasnoyarsk territory. Some 750 miles of supply lines will need to be built. Zapolyarye-Purpe will connect fields on the Yamal Peninsula to the Eastern Siberia-Pacific Ocean pipeline (ESPO).

The pipeline will be constructed in three phases with the final phase scheduled for completion in 2016.

Transneft reports that the second stage of the East Siberia-Pacific Ocean (ESPO) pipeline carrying Russian crude to Asian-Pacific markets and the U.S. should be in service by year end, well ahead of schedule. The first part carrying 30 MMt/a of East Siberian crude to Skovorodino near the Chinese border was launched in 2009. Once the second part of the ESPO pipeline from Skovorodino to Kozmino is completed, capacity to the Pacific coast will increase to 30 MMt/y.

Work got under way last year on Kazakh’s KazTransGas and China’s Trans-Asia Gas Pipeline Co. Ltd.’s Beineu-Bozoy-Shymkent Gas Pipeline, which is the second stage of the Kazakhstan-China Gas Pipeline. The 916-mile project will be built in two phases; the first involves laying 723 miles from Bozoy-Shymkent and constructing a compressor station near Bozoy. This phase is set for completion in 2012. Second-phase activity, to be completed from 2014-15, includes a 193-mile section from Beineu–Bozoy and a compressor station in Karaozek. Another 26 branches will be built from the mainline during the first and second phases to supply communities along the route.

BP has proposed an alternative pipeline project to feed Europe with Caspian natural gas. The South East Europe Pipeline would link a major Azerbaijan gas field to a hub in Austria running from western Turkey across Bulgaria and Romania to Hungary’s border, a similar route to that of EU-backed Nabucco pipeline. South East Europe Pipeline would be 810 miles, one-third the length of Nabucco, making it a more economical project.

As operator of the Shah Deniz field – the main Azeri gas natural field – BP may have influence over which pipeline the Shah Deniz consortium will choose.

Two other pipelines – Nabucco and Russian-backed South Stream – are proposed to tap Azeri gas for export to Europe. A final investment decision on the $20 billion Azeri development is expected in 2013.

Gazprom and China National Petroleum Corporation (CNPC) plan to partner to build the 1,616-mile Altai Pipeline to deliver natural gas from western Siberia to northwestern China. The contract period is 30 years and the supply volume, upon reaching design capacity, will be 30 Bcm/yr. First supplies are planned for 2015.

Africa

Limited energy development in Africa is due to political, economic, operational and geopolitical risks. The region accounts for 6,683 miles of planned pipelines and 934 miles under construction.

One area that may hold promise for near-term activity is Nigeria. At the World Petroleum Congress in Qatar, Minister of Petroleum Resources Diezani Alison-Madueke outlined $130 billion in investment plans for oil and gas sectors over the next five years, calling for construction of 1,245 miles of oil and gas pipelines to boost domestic gas supply, a petrochemical plant, new fertilizer and manufacturing plants and three greenfield refineries.

Also in Nigeria, Shell Petroleum Development awarded a contract to Saipem for the Otumara-Saghara-Escravos Gas Pipeline. The 26-mile pipeline, ranging from 2 to 12 inches, will collect 30 Mcf/d of processed associated gas from the western Niger Delta and send it through the Escravos-Lagos system to the domestic market.

Total E&P Angola is developing the CLOV project – an integrated development of a four-field offshore cluster. A total of 34 subsea wells will connect to the CLOV FPSO unit which has processing capacity of 160,000 bopd and storage capacity of 1.78 million barrels.

Serimax is conducting the welding works for the project that involves 500 welds of 10- and 12-inch pipe. The pipe will be installed in 1,000-1,400 meters of water. Project completion is due in 2013.

Total Gabon awarded the Sea Trucks Group a contract to install a 20-mile, 18-inch concrete-coated gas pipeline between the Anguille and Torpille fields off Gabon. The installation work is expected to start this spring.

China and Tanzania signed a $1 billion loan agreement to build a natural gas pipeline in East Africa. The 330-mile pipeline would extend from southern Tanzania to the capital, Dar es Salaam. The 36-inch pipeline will have transport capacity of 784 MMcf/d.

Awaiting a construction start is the 2,565-mile Trans-Saharan Gas Pipeline (TSGP) planned by the Nigerian National Petroleum Company and Sonatrach. Total, Gazprom and the European Union have all displayed an interest in assisting construction. EU officials say the pipeline could supply 20 Bcm/y of gas to Europe by 2016.

Western Europe/EU

While pipeline activity in Western Europe and EU Countries was expected to increase following a decision by the European Commission to provide US$1.9 billion in grants to ensure that some 30 gas project would not be delayed, the growing financial crisis among many EU countries could derail near-term activity.

Those projects scheduled to receive grants include the 500-mile Interconnector Turkey-Greece-Italy (ITGI) project, 130-mile Poseidon Pipeline, 281-mile Skanled Pipeline, 2,050-mile Nabucco Pipeline, 235-mile Odessa-Brody project and the 130-mile Slovakia- Hungary Interconnector.

One area where pipeline work is under way and planned is the North Sea.

Subsea 7 is working under an EPIC contract from Total E&P UK Limited on the Laggan and Tormore deepwater gas field development located west of Shetland in the North Sea. Subsea 7’s principal scope of work comprises the engineering, fabrication and installation of 88 miles of 8-inch and 2-inch piggy-backed service pipelines and the engineering, supply and installation of 1 x 77-mile control umbilical and associated subsea structures and tie-ins.

Phase 1 offshore operations encompassing pipelines and umbilical installations and pre-commissioning activities are scheduled to start shortly. Phase 2 offshore operations, encompassing tie-in and commissioning activities, are scheduled to start in 2013.

Saipem is installing a subsea pipeline in the Ormen Lange northern field development in the Norwegian Sea for A/S Norske Shell. The project is being developed with a subsea template located in 900 meters of water and tied back to Ormen Lange by two 12-inch production pipelines, a 6-inch service line and a control umbilical.

In the Barents Sea, Eni Norge awarded a contract to Technip valued at 200 million Euro for the Goliat field development. Goliat will be the first Norwegian oil-producing field north of the Arctic Circle in the Barents Sea. It is located 59 miles northwest of the city of Hammerfest on the Norwegian coast. Offshore installation work is scheduled to be carried out over three construction seasons from 2011-13.

Middle East

In the Middle East 8,805 miles of pipelines are planned and 2,675 miles are in various stages of completion.

RASGAS (joint venture between Qatar Petroleum and ExxonMobil) plans to develop the multibillion-dollar Barzan natural gas project in the North Field reservoir offshore Qatar in the Arabian Gulf. Work includes a natural gas offshore production system with conventional wellhead platforms, intrafield pipelines, 180 miles of up to 24-inch export pipeline to the onshore Barzan Gas Plant in Ras Laffan Industrial City (RLC). First-phase production is scheduled at 1.5 Bcf/d.

In Saudi Arabia, Saudi Aramco awarded an EPIC contract to Saipem for the Al Wasit Gas development of the Arabiyah and Hasbah offshore fields. This encompasses 12 wellhead platforms, two tie-in platforms and an injection platform, a 36-inch, a 160-mile export trunkline, 125 miles of mono-ethylene glycol (MEG) pipelines, 125 miles of subsea electric and control cables and 25 miles of offshore flowlines. Also included are shore approaches and 75 miles of onshore pipelines.

ConocoPhillips and Abu Dhabi National Oil Company (ADNOC) awarded the Shah Gas project in Abu Dhabi to the Al Jaber Group. The project requires construction of facilities including gas-gathering systems, processing trains and product pipelines.

Adnoc has said it expects first production by late 2013 or early 2014.

In the UAE, Technip, in consortium with NPCC, was awarded an EPC contract by ZADCO for the Satah Full Field Development project, 124 miles northwest of Abu Dhabi. The $500 million contract includes offshore brownfield works to existing wellhead platforms and production manifold platform, installation of infield pipelines, as well as modifications and installation of facilities at the onshore Satah plant at Zirku Island.

Leighton Offshore is working under a $58 million contract from Iraq’s South Oil Company as part of the Crude Oil Export Facility Reconstruction Project (Sea Line Project). This involves developing two offshore platforms, a 47-mile, 48-inch oil pipeline and a Single Point Mooring system. The project will expand export capacity by building a pipeline connecting storage sites to the offshore crude oil export terminal near Basra in southern Iraq.

Foster Wheeler’s Global Engineering and Construction Group was awarded a project management consultancy (PMC) services contract by South Oil Company (SOC) for the Iraq Crude Oil Export Expansion Project. This calls for installation of two onshore and offshore pipelines plus three single-point moorings and a central manifold and metering platform. Scheduled for completion in 2013, the project is expected to boost Basra export capacity from 1.8 MMbp/d to 4.5 MMbp/d by 2014.

South & Central America/Caribbean

Several South, Central American and Caribbean countries are implementing plans for new pipeline infrastructure.

In Brazil, Petrobras is constructing a 530-mile ethanol pipeline to link the main ethanol- producing regions in Minas Gerais and São Paulo to the large consuming centers of São Paulo and Rio de Janeiro. The pipeline will have capacity to transport 21 MMcm/a.

The first section will extend 125 miles from Ribeirão Preto to Paulinia. Phase two involves construction northward through states in the mid-west. The system will be extended to Barueri and Guarulhos in greater São Paulo and Duque de Caxias in Rio Di Janeiro. The pipeline should be brought online in 2014.

Pacific Rubiales Energy Corp. has partnered with EXMAR to develop an LNG export project in northern Colombia. The project involves construction and development of a liquefaction and regasification barge, a small-scale vessel designed to deliver LNG to industrial consumers, and development of a pipeline from the company’s La Creciente gas field to the Caribbean coast.

Front-end engineering and design have begun. The project and pipelines are expected to be operational in 2013.

A recent Rigzone report outlined an MOU calling for a joint venture by Russia’s Rosneft and Petroleo de Venezuela (PDVSA) to develop heavy crude oil reserves in Venezuela as part of the Carabobo-2 project. Crude oil production is expected to peak at above 400,000 bpd.

It the plan goes forward, work will cover the exploration and development cycle as well as construction of surface facilities and pipelines. There are plans to add a special processing facility (upgrader) with a capacity of 200,000 bpd to bring extracted oil up to commercial quality. Commercial oil will be transported for export to the Araya port through a trunk pipeline to be built by PDVSA.

Comments