December 2010 Vol. 237 No. 12

Features

Onshore Pipeline Outlook: Strong Through 2015

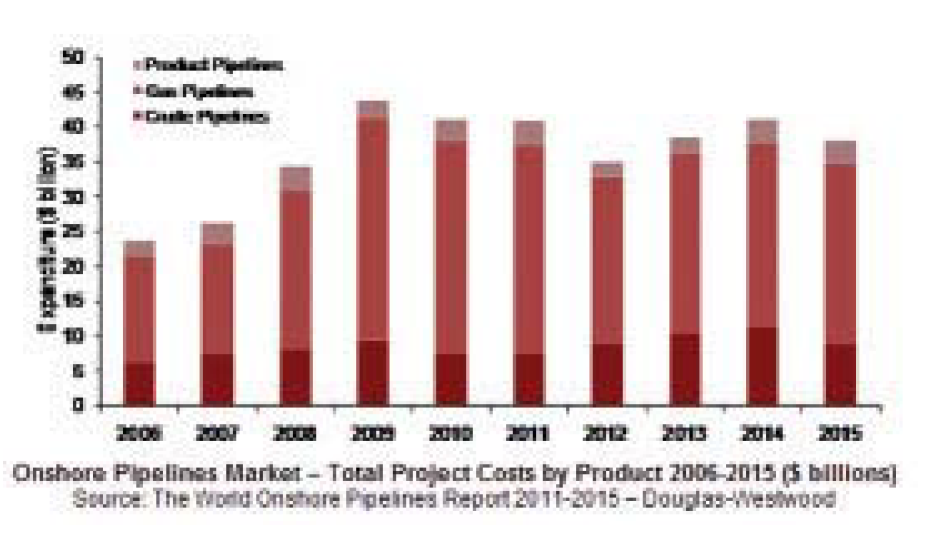

It is forecast that $193 billion will be spent on onshore pipeline projects worldwide through to 2015, according to data in energy business analysts Douglas-Westwood’s third edition of The World Onshore Pipelines Report 2011-2015.

The report notes that in recent years, levels of activity in the onshore pipelines market have been affected by what can be considered, in relative terms, short-term macroeconomic factors.

This has particularly been the case in developed regions such as North America whose economies have been most affected, but less so in developing regions such as Asia, where strong economic growth has been maintained.

In these developed economies, the report says, the global economic downturn had the dual effect of both destroying energy demand as well as reducing the availability of credit.

This combination led to many proposed pipeline projects either being delayed or in some cases cancelled altogether, which is highlighted by the trend of declining annual expenditure – a trend set to produce a significantly reduced annual industry expenditure in 2012.

However, over the forecast period 2011-2015, these short-term factors will ultimately begin to once again give way to more long-term and industry specific drivers.

Beyond 2012, the report notes that continued growth in global oil and gas demand and the associated production increases (fundamental long-term drivers of activity), will require significant investment in pipeline infrastructure.

In North America, increasing investment in the development of unconventional energy sources, such as shale gas and oil sands, is set to create a shift in the location concentrations of production and will require major investment in new pipeline projects to link the new energy sources with existing pipeline networks and new markets.

Meanwhile, in Asia, soaring energy demand is set to continue to support strong levels of investment in domestic pipeline networks, as well as many trans-national and trans-regional projects designed to help meet long-term energy requirements.

In Europe , the desire to create greater energy security through supply diversification and greater regional network integration is set to drive investment in a number of regional and trans-regional projects.

The World Onshore Pipelines Report from Douglas-Westwood forecasts an 11% increase in kilometers of pipelines installed over the period 2011-2015, compared to the historic 2006-2010 period. Nearly 74% of the associated expenditure is expected to be spent in Asia, Eastern Europe and the FSU and North America. More than 68% of this expenditure is expected to be spent on gas pipelines.

According to the report, Asia stands out as the largest forecast market – by both length of pipeline construction and associated expenditure – accounting for $55 billion of forecast capital expenditure.

Douglas-Westwood officials say the forecasting process involved the scrutiny of all announced pipeline prospects on a project-by-project basis. This process resulted in a significant number of announced pipeline projects being “slipped out” of the forecast period. Also, some projects currently expected to go ahead will slip, but likewise some new projects will certainly come to fruition over the forecast period – compensating somewhat for potential project slippage.

In light of the strength of market drivers and the volume of announced projects, Douglas-Westwood expects the onshore pipelines industry to recover strongly and experience substantial and sustained levels of investment over the forecast period.

For more information on The World Onshore Pipelines Report 2011-2015, visit http://www.dw-1.com/shop/shop-infopage.php?longref=547~0

Comments