November 2010 Vol. 237 No. 11

Features

U.S. Oil And Gas Merger/Acquisition Activity Shows Strong Gains

Merger and acquisition (M&A) activity in the U.S. oil and gas sector reached its highest level in more than six quarters during the second quarter 2010, according to PricewaterhouseCoopers LLP (PwC). With improved credit markets and buyer-seller expectations finally aligning, coupled with increased CEO confidence and stabilized commodity prices, the U.S. oil and gas sector saw a total of 142 announced deals in the second quarter – the highest volume for deals seen since the third quarter of 2008, when the total numbers of announced deals was 190, according to PwC.

Total value for the second quarter amounted to $36.9 billion, compared with $13.7 billion in the second quarter of 2009, representing a 169% increase year over year.

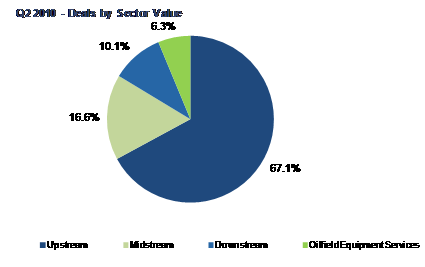

For the first six months of 2010, the oil and gas sector accounted for 262 announced deals – a 27% increase over the number of deals compared to the same period last year. A sequential quarter over quarter comparison shows oil and gas activity continues to be robust with an 18.3% increase over the first quarter, which included 120 announced transactions at a value of $32.5 billion. Upstream asset-focused deals dominated deal activity, comprising 67% of total deal value in the quarter, along with the largest total deal volume at 80%.

“Deal activity in the oil and gas sector rebounded significantly in the second quarter, and we expect the momentum to continue throughout the second half of the year,” said Michael Collier, U.S. leader of the energy M&A practice at PricewaterhouseCoopers.

“As commodity prices and equity markets continue to stabilize, senior managers are showing greater inclination to do transactions today than we’ve seen over the past two years. At the same time, buyers and sellers are more aligned when it comes to valuations, which is helping to drive the market and to ultimately get deals done,” he said.

For the three month period ending June 30, asset sales represented 85% of deal activity compared with 15% from U.S. corporations, in part due to oil and gas companies exiting conventional commitments to focus on and finance positions in unconventional sources of energy.

“Asset sales heavily contributed to the resurgence in activity in the second quarter, which have largely been driven by oil and gas companies’ continuing to adjust their portfolios to maximize the return on their core businesses,” continued PwC’s Collier. “While the oil spill has created some uncertainties for deepwater assets, the U.S. government policy response will be the real driver as CEO’s of both resource and equipment and services companies rethink the risks and rewards of doing business in the deep water.”

Some $13.4 billion in deals related to assets sales that involved non-U.S. entities taking positions in shale gas and unconventional oil and gas assets. Foreign buyers made up more than 25% of the transactions in the quarter, up from 21.6% during the same period last year. Inbound transactions by China-based companies accounted for $900 million in M&A deals, demonstrating China’s ongoing search to feed its appetite for oil and gas as the world’s leading consumers of energy.

There were 11 refinery deals with total value of $3.7 billion, compared with the five deals with a total value of $231.6 million over the same period last year. “Some spectacular returns were achieved during the last cycle for investors with the courage to buy at the bottom of the cycle. While the deal volume in refineries is relatively small, there may be more “bets” on improving crack spreads as investors, some of whom will be private equity-backed, will try to re-do some of the last cycles’ great wins,” added Collier.

“With a significant amount of capital on the sidelines, private equity firms are beginning to find opportunities to do deals in oil and gas, especially focused on midstream and upstream assets,” Collier noted. “As deal activity continues to heat up, U.S. corporations are acknowledging the savvy deal making strategy of private equity firms and are adopting those skill sets to better compete and succeed in the competitive oil and gas industry.”

Editor’s Note: PricewaterhouseCoopers’ oil and gas M&A analysis is a survey of announced U.S. transactions compiled by PricewaterhouseCoopers and Herold’s. For information, visit: http://www.pwc.com or www.braincomm.com. Email contact: pieri@braincomm.com.

Comments